- Why have we been recycling plastic? Gonzalez & Sullivan, Planet Money

- The literary scene in the Great Depression Ben Terrall, CounterPunch

- Stealing from the Saracens Edwin Heathcote, Financial Times

- The long road to reaction Thomas Meaney, New Statesman

Great Depression

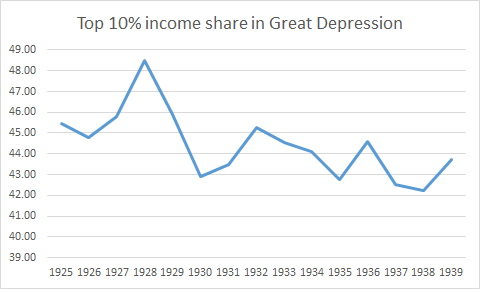

Did Inequality Fall During the Great Depression ?

The graph above is taken from Piketty and Saez in their seminal 2003 article in the Quarterly Journal of Economics. It shows that inequality fell during the Great Depression. This is a contention that I have always been very skeptical of for many reasons and which has been – since 2012 – the reason why I view the IRS-data derived measure of inequality through a very skeptical lens (disclaimer: I think that it gives us an idea of inequality but I am not sure how accurate it is).

Here is why.

During the Great Depression, unemployment was never below 15% (see Romer here for a comparison prior to 1930 and this image derived from Timothy Hatton’s work). In some years, it was close to 25%. When such a large share of the population is earning near zero in terms of income, it is hard to imagine that inequality did not increase. Secondly, real wages were up during the Depression. Workers who still had a job were not worse off, they were better off. This means that you had a large share of the population who saw income reductions close to 100% and the remaining share saw actual increases in real wages. This would push up inequality no questions asked. This could be offset by a fall in the incomes from profits of the top income shares, but you would need a pretty big drop (which is what Piketty and Saez argue for).

There is some research that have tried to focus only on the Great Depression. The first was one rarely cited NBER paper by Horst Mendershausen from 1946 who found modest increases in inequality from 1929 to 1933. The data was largely centered on urban data, but this flaw works in favor of my skepticism as farm incomes (i.e. rural incomes) fell more during the depression than average incomes. There is also evidence, more recent, regarding other countries during the Great Depression. For example, Hungary saw an increase in inequality during the era from 1928 to 1941 with most of the increase in the early 1930s. A similar development was observed in Canada as well (slight increase based on the Veall dataset).

Had Piketty and Saez showed an increase in inequality during the Depression, I would have been more willing to accept their series with fewer questions and doubts. However, they do not discuss these points in great details and as such, we should be skeptical.

Famine and Finance: Credit and the Great Famine of Ireland

I have recently finished reading Famine and Finance by Tyler Beck Goodspeed. While short, it should have a prominent place on the shelves of economic historians interested (obviously) in Irish history and (less obviously) in Malthusian theory.

I have recently finished reading Famine and Finance by Tyler Beck Goodspeed. While short, it should have a prominent place on the shelves of economic historians interested (obviously) in Irish history and (less obviously) in Malthusian theory.

Famine and Finance is a study of the response of Irish farmers to the potato blight. As it is known to many, many individuals simply left Ireland. However, where micro-credit was available, Goodspeed finds that farmers adapted by shifting to different types of activities – notably livestock. These areas experienced a smaller decline in population. Basically, where the institution of micro-credit was present, the demographic shock was much less severe. If only for this nuance, the book makes a sizeable contribution to the historiography of Ireland. The methods used are also elegantly simple and provide an interesting road map for anyone interested in studying the responses of local population to environmental shocks.

However, the deeper point comes from it tells us about institutions. In Goodspeed’s story, the amplitude of the collapse of the Irish population in the 19th century depends on the presence of the institution of micro-credit. Basically, the institution determined the amplitude of the shock. Since Ireland’s potato blight is often presented as the textbook case of Malthusian pressures, Goodspeed’s results are particularly interesting. In his chatper titled”Was Malthus Right?”, he shows that when controls for the institution of micro-credit is present, the typical Malthusian variables fail to explain population changes. In other words (i.e. my words) , Malthusian pressures (the change in population) are in fact institutional failures.

This is a point I have often made elsewhere (see here, here and here and a blog post here). And because Goodspeed backs this point of mine, he has earned himself a place on my shelf of “go-to” books.

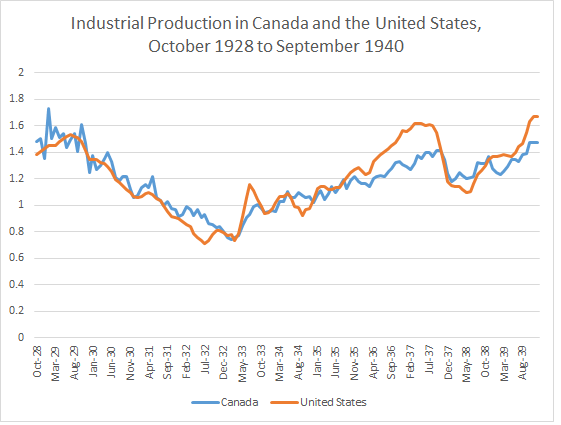

How Canada Tracked the US during the Great Depression

Over the last few years, while I continued my research on other fronts, I started spending small amounts of time on a daily basis to read about the Great Depression and more precisely, how Canada lived through the depression.

Since the old adage is that Canada gets pneumonia when the US gets the flu, I thought that it was a worthy endeavor (although Pedro Amaral and James McGee have been working on that front) to try to see what insights we can derive from looking at Canada’s experience during the Great Depression (especially since it had a very different banking system).

In the process, I managed to collect in a datasheet, the Industrial Production Index of Canada (consisting largely of heavy industry with some light industries and utilities, making it a relatively well-rounded index). This is what it looks like.

Other than seeing Canada’s experienced mirrored in the US experience (except for the 1935-1937 window), I am not sure what to make of it. However, I thought it worthwhile to share that information publicly.

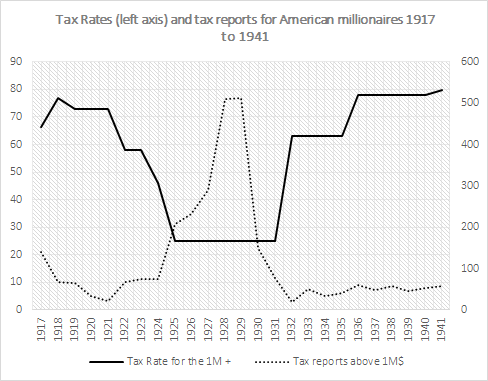

Did 89% of American Millionaires Disappear During the Great Depression?

Over the years, I became increasingly skeptical of using tax data to measure inequality. I do not believe that there is no value in computing inequality with those sources (especially after the 1960s, the quality is much better in the case of the US). I simply believe that there is a great need for prudence in not overstretching the results. This is not the first time I make this point (see my paper with Phil Schlosser and John Moore here) and I think it is especially crucial for anything prior to 1943 (the introduction of tax withholding).

One of my main point is that the work of Gene Smiley which ended up published in the Journal of Economic History has generally been ignored. Smiley had highlighted many failings in the way the tax data was computed for measuring inequality. His most important point was that tax avoidance foiled the measurements of top incomes and how well they could transposed on the overall national accounts.

More precisely, Smiley argued that the tax shelters of the 1920s and 1930s would have affected reporting behavior. As long as corporations could issue stock dividends rather than cash dividends, delaying the payment of dividends until shareholders were in lower tax brackets, there would be avoidance. Furthermore, state and municipal securities were exempted from taxation which meant that taxpayers could shelter income and end up in lower brackets. All this combined to wide fluctuations in marginal tax rates conspires to reduce the quality of the tax data in computing inequality. Rather than substantial increases in inequality, Smiley found that his corrected estimates (which kept tax rates constant) suggested no increase in inequality during the 1920s and a minimal decrease when you exclude capital gains.

Alongside John Moore, Phil Schlosser and Phil Magness, I am in the process of attempting to extend the Smiley corrections to include everything up to 1941 (Smiley had ended in 1929). As a result, I had to assemble the tax data and the tax rates and I was surprised to see that, even without regressions, we can see the problem of relying on the tax data for the interwar period.

The number of millionaires in the tax reports is displayed below. As one can see, it is very low from 1917 to 1924 – a period of high tax rates. However, as tax rates fell in the 1920s, the number of millionaires quintupled. And then, when the Depression started in synchronicity with the increases in top marginal tax rates, it went back down. It went down by 89% from 1929 to 1941. Now, I am quite willing to entertain that many millionaires were wiped out during the Great Depression. I am not willing to entertain the idea that 9 out of every 10 millionaires disappeared. What I am willing to entertain is that the tax data is clearly and heavily problematic for the pre-withholding era.* This is evidence in favor of caution and prudence in interpreting inequality measures derived from tax data.

* I am of those who believe that inequality was lower than reported elsewhere in the 1920s, higher than reported in the 1930s and 1940s. Combined together, these would mean that inequality would tend to follow a L-curve or a J-curve from the 1920s up to the present rather than the U-curve often reported. I will post more on this as my paper with Moore, Schlosser and Magness progresses.

Stock markets and economic growth: from Smoot-Hawley to Donald Trump

In a recent article for the Freeman, Steve Horwitz (who has the great misfortune of being my co-author) argued that stock markets tell us very little about trends in economic growth. Stock markets tell us a lot about profits, but profits of firms on the stock market may be higher because of cronyism. Basically, that is Steve’s argument. He applies this argument in order to respond to those who say that a soaring stock market is the proof that Donald Trump is “good” for the economy.

I know Steve’s article was published roughly a month ago, so I am a little late. But I tend to believe it is never too late to talk about economic history. And basically, its worth pointing out that there are economic history examples to show Steve’s point. In fact, its the best example: Smoot-Hawley.

Bernard Beaudreau from Laval University has advanced, for some years, an underconsumptionist view of the Great Depression (I consider it a “dead theory”). While I am highly unconvinced by this theory (in both its original and current “post-keynesian” reformulation), Beaudreau tries hard to resurrect the theory (see here and here) and merits to be discussed. In the process, Beaudreau attempted to reestimated the effects of of Smoot-Hawley on the stock market with an events study. Unconvinced about the rest of his research, this is a clear instance of sorting the wheat from the chaff. In this case, the wheat is his work (see here for his article in Essays in Economic and Business History) on Smoot-Hawley.

Basically, Beaudreau found that good news regarding the probability of the adoption of the tariff bill actually pushed the stock market to appreciate. Thus, Smoot-Hawley -which had so many negative macroeconomic ramifications* – actually boosted the stock market. Firms that gained from the rising tariffs actually saw greater profits for themselves and thus the firms on the stock market would have been excited at the prospect of restricting their competitors. If that is true, could it be that Donald Trump is the modern equivalent (for the stock market) of Smoot-Hawley.

*NDLR: I believe that Allan Meltzer was right in saying that the Smoot-Hawley might have had monetary ramifications that contributed to the money supply collapse. It was a real shock that precipitated the collapse of weak banks which then caused a nominal shock and then the sh*t hit the proverbial fan.

Alguns mitos, equívocos e objeções comuns ao capitalismo parte 2

Continuando um post antigo, seguem mais alguns mitos, equívocos e objeções comuns ao capitalismo.

Três mitos a respeito da Grande Depressão e do New Deal

Mito #1: Herbert Hoover praticava o laissez-faire, e foi sua falta de ação que levou ao colapso econômico.

Na verdade Herbert Hoover era tremendamente intervencionista na economia. Sua intervenção cooperou para o início da depressão e sua continuada intervenção evitou que a economia se recuperasse logo.

Mito #2: o New Deal trouxe fim à Grande Depressão.

Longe de ser uma série de medidas coerentes contra a depressão, o New Deal foi uma tentativa de Frank Delano Roosevelt de demonstrar que estava fazendo alguma coisa. As medidas do New Deal apenas agravaram e prolongaram a crise. Países que adotaram uma postura menos intervencionista se recuperaram da crise mais rápido do que os EUA.

Mito #3: A Segunda Guerra Mundial deu fim à Grande Depressão.

Talvez este seja o pior mito de todos: a produção industrial no contexto da Segunda Guerra gerou empregos, aumentou o PIB, e com isso acabou com a Depressão. Conforme Friedrich Hayek afirmou, “da última vez que chequei, guerras apenas destroem”. Este mito é uma aplicação da falácia da janela quebrada, observada por Frédéric Bastiat. Guerras não produzem riqueza. Na verdade elas a destroem. O exame cuidadoso dos dados históricos demonstra que a economia dos EUA só se recuperou realmente quando a Segunda Guerra Mundial já havia acabado.

Mais alguns mitos, equívocos e objeções comuns ao capitalismo:

1. Capitalismo é racista e sexista

Considerando o capitalismo economia de livre mercado, onde indivíduos são livres para escolher, nada poderia estar mais longe da verdade. O capitalismo assim definido é cego para raça ou gênero. O que importa é a troca de valores. Para ficar em apenas um exemplo, as lideranças políticas do sul dos EUA pressionavam os donos de empresas de ônibus a segregar os passageiros com base na cor da pele. Os próprios empresários de ônibus queriam ganhar dinheiro com transporte de pessoas, independente da cor da pele. Apenas uma observação: recusar serviço com base em cor de pele, gênero, orientação sexual ou qualquer outro motivo é uma prerrogativa do indivíduo dentro do capitalismo. Leve seu dinheiro para uma instituição que o receba. A instituição que recusa serviço está perdendo dinheiro, e neste sentido já recebeu a punição dentro do capitalismo.

2. Capitalismo tende a bolhas e pânico

Esta é uma observação presente tanto em Marx quanto em Keynes. Conforme observado nos mitos sobre a Grande Depressão e o New Deal, exatamente o oposto é verdade. Conforme a Escola Austríaca em geral e Friedrich Hayek de forma especial observaram, é a intervenção do governo, particularmente no setor bancário e financeiro, que produz bolhas e pânico. A tentativa do governo de estimular a economia através de juros baixos e outros artifícios apenas cria ciclos de crescimento e queda. Milton Friedman e a Escola de Chicago fizeram observações semelhantes. Deixada livre a economia é de certa forma imprevisível, mas através do sistema de preços podemos nos guiar sobre quando e no que é melhor gastar.

3. Capitalismo não investe em coisas importantes

É difícil saber o que seria um investimento importante. Somente indivíduos podem avaliar o que é importante para eles mesmos. O raciocínio aqui é que há investimentos de longo prazo, que custam muito dinheiro e não produzem resultado imediato. Capitalistas não investiriam em voos espaciais ou na cura de doenças, por exemplo. Mais uma vez observa-se a falácia da janela quebrada: investir em uma coisa significa não investir na próxima melhor opção. Exemplos recentes mostram que empresas atuando no livre mercado podem fazer mais, melhor e com menos desperdício do que governos, inclusive quando o assunto é exploração espacial.

4. Capitalismo leva a produção de coisas duvidosas

Mais uma vez este é um argumento de orientação subjetiva. Aquilo que é duvidoso para um individuo pode ser bom para outro. Há aqui a velha máxima de que “o capitalismo produz necessidades artificiais”. Conforme Voltaire respondeu a Rousseau mais de 200 anos atrás, este argumento não se sustenta. O que é uma “necessidade artificial”? Tesouras são necessidades artificiais? E sabão? E pasta de dente? Porque seres humanos viveram por séculos sem estas coisas. Conforme já foi observado por Joseph Schumpeter, a grande virtude do capitalismo é justamente trazer conforto a baixo preço não para reis e rainhas, mas para as pessoas mais simples em uma sociedade. Ainda que alguns possam considerar certos produtos de consumo duvidosos. Apenas não comprem.

Referências:

3 Myths of Capitalism (YouTube)

Top 3 Myths about the Great Depression and the New Deal (YouTube)

Common Objections to Capitalism (YouTube)

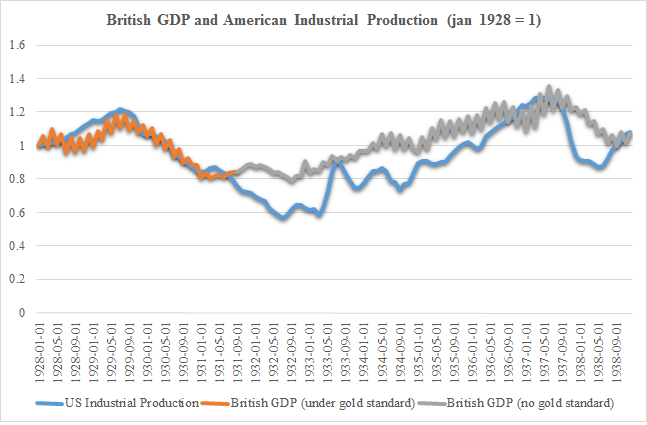

Why Britain, in the Great Depression, is the best example in favor of NGDP targeting

A few weeks ago, I finished reading Scott Sumner’s The Midas Paradox. As an economic historian, I must say that this is by far the best book on the Great Depression since the Monetary History of the United States. Moreover, it is the first book that I’ve read that argues simply that the Great Depression was the result of a sea of poor (and sometimes good) policy decisions. However, coming out of the book, there was one thing that came to mind: Sumner is underselling his (very strong) case.

In essence, the argument of Sumner looks considerably like that of Milton Friedman and Anna Schwartz: The Federal Reserve allowed the money supply to contract dramatically up to 1932, turning what would have been a mild recession into a depression. However, Sumner adds a twist to this. He mentions that after the depth of the monetary contraction had been reached, there was a reflation allowing an important recovery during 1933. This is standard AS-AD macro of a (very late) expansionary policy to allow demand to return to equilibrium. Normally, that would have been sufficient to allow the rebound. Basically, this is the best case for NGDP targeting: never let nominal expenditures fall below a certain path because of a fall in demand. The problem, according to Sumner, is that the recovery was thwarted by poor supply-side policies (like the National Industrial Recovery Act, the Agricultural Adjustment Act etc.). The positive effects of the policy were overshadowed by poor policy. And thus, the depression continued.

To be fair, Sumner is not the first to emphasize the “real” variables side of the Great Depression. I am especially fond of the work of Richard Vedder and Lowell Galloway, Out of Work, which is a very strong candidate for being the first econometric assessment of the effects of poor supply-side policies during the Great Depression. I was also disappointed (but not too much since Sumner did not need to make this case) to see that no mention was made of the Smoot-Hawley tariff as a channel for monetary transmission (as Allan Meltzer argued back in 1976) of the contraction. Nonetheless, Sumner is the first to bring this case so cogently as a story of the Great Depression. Thus, these small issues do not affect the overall potency of his argument.

The problem, as I mentioned earlier, is that Sumner is underselling his case! I base this belief on the experience of England at the same time. Unlike the United States, the British decided to apply their piss-poor supply-side policies during the 1920s – well before the depression. The seminal paper (see this one too) on this is by Stephen Broadberry (note: I am very biased in favor of Broadberry given that he is my doctoral supervisor) who argued that the supply shocks of the 1920s caused substantial drops in hours worked and although the rise of unemployment benefits played a minor role, the vast majority of the causes were due to the legal encouragement of cartel formation. As a result, there were no supply-side shocks during the depression to create noise. However, England did have a demand-side expansionary policy in 1931. Even if it was by accident more than by design, England left the gold standard in September 1931. This led to the equivalent of an easy monetary policy and the British economy stopped digging and expanded afterwards. The Great Depression was not a pleasant experience for the British, but it was not even close to the dreadful situation in the United States. As a result, we can see whether or not it was possible to exit the Great Depression by virtue of a monetary policy. I’ve combined the FRED dataset on monthly industrial production and the monthly GDP estimates for inter-war Britain produced by Mitchell, Solomou and Weale (see here) to see what happened in England after it left the gold standard. As one can see, the economy of Britain rebounded much more magnificently than that of the United States in spite of supply-side constraints.

Sumner should expand on this point! To be fair, he does talk about it briefly. Not enough! A longer discussion of the British case provides him with the “extra mile” to cover the distance against competing theories. The absence of supply shocks in Britain during the Depression confirm his story that the woes of the United States during the 1930s are due to initially poor monetary policy and then poor supply-side policies. In my eyes, this is a strong confirmation of the importance of the NGDP level target argument!

With such a point made, it is easy to imagine a reasonable counterfactual scenario of what economic growth would have been after monetary easing in 1933 in the absence of supply-side shocks. Had the United States kept very unregulated labor and product markets, it is quite reasonable to believe (given the surge seen in 1933 in the Industrial Production data) that the United States would have returned to 1929 levels. In the absence of such a prolonged economic crisis, it is hard to imagine how different the 1930s and 1940s would have been but it is hard to argue that things would have been worse.

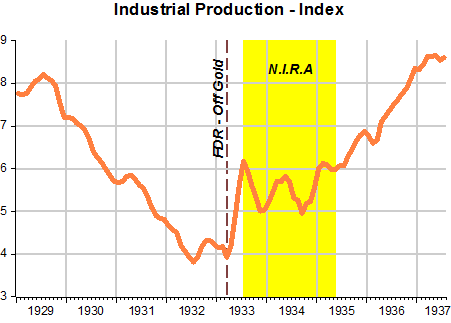

UPDATE: From the blog Historinhas, Marcus Nunes sent me the graph below confirming the importance of the NIRA shock on eliminating all the benefit from easy money after 1933.

Was Murphy Foolish to Take Caplan’s Bet?

A few days ago, Bryan Caplan posted on his bet with Robert Murphy regarding inflation. Murphy predicted 10% inflation. He lost … big time. However, was he crazy to make that bet? In other words, what could explain Caplan’s victory?

Murphy was not alone in predicting this, I distinctly remember a podcast between Russ Roberts and Joshua Angrist on this where Roberts tells Angrist he expected high inflation back in 2008. Their claims were not indefensible. Central banks were engaging in quantitative easing and there was an important increase of the state money supply. There was a case to be made that inflation could surge.

It did not. Why?

In a tweet, Caplan tells me that monetary transmission channels are much more complex than they used to be and that the TIPS market knew this. Although I agree with both these points, it does not really explain why it did not materialize. I am going to propose two possibilities of which I am not fully convinced myself but whose possibility I cannot dismiss out of hand.

Imagine an AS-AD graph. If Murphy had been right, we should have seen aggregate demand stimulated to a point well above that of long-run equilibrium. Yet, its hard to see how quantitative easing did not somehow stimulate aggregate demand. Now, if aggregate demand was falling and that quantitative easing merely prevented it from falling, this is what would prove Murphy wrong. However, all of this assumes no movement of supply curves.

While AD falls and before monetary policy kicks in, imagine that policies are adopted that reduce the potential for growth and productivity improvement. In a way, this would be the argument brought forward by people like Casey Mulligan in work on labor supply and the “redistribution recession” and Edward Prescott and Ellen McGrattan who argue that, once you account for intangible capital, the real business cycle model is still in play (there was a TFP shock somehow). This case would mean that as AD fell, AS fell with it. I would find it hard to imagine that AS shifted left faster than AD. However, a relatively smaller fall of AS would lead to a strong recession without much deflation (which is what we have seen in this recession). Personally, I think there is some evidence for that. After all, we keep reducing the estimate for potential GDP everywhere while the policy uncertainty index proposed by Baker, Bloom and Davids shows a level change around 2008. Furthermore, there has been a wave – in my opinion of very harmful regulations – which would have created a maze of administrative costs to deal with (and whose burden is heavy according to Dawson and Seater in the Journal of Economic Growth). That could be one possibility that would explain why Murphy lost.

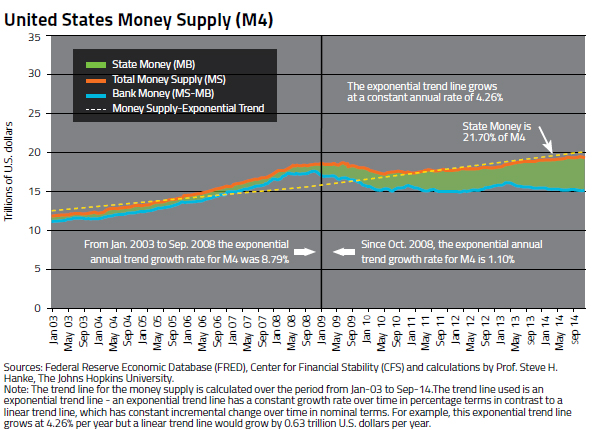

There is a second possibility worth considering (and one which I find more appealing): the role of financial regulations. Now, I may have been trained mostly by Real Business Cycle guys, but I do have a strong monetarist bent. I have always been convinced by the arguments of Steve Hanke and Tim Congdon (I especially link Congdon) and others that what you should care about is not M1 or M2, but “broad money”. As Hanke keeps pointing out, only a share of everything that we could qualify broadly as “money” is actually “state money”. The rest is “private money”. If a wave of financial regulations discourages banks to lend or incite them to keep greater reserves, this would be the equivalent of a drop of the money multiplier. If those regulations are enacted at the same time as monetary authorities are trying to offset a fall in aggregate demand, then the result depends on the relative impact of the regulations. The data for “broad money” (Hanke defines it as M4) shows convincingly that this is a potent contender. In that case, Murphy’s only error would have been to assume that the Federal Reserve’s policy took place with everything else being equal (which was not the case since everything seemed to be moving in confusing directions).

In the end, I think all of these explanations have value (a real shock, a banking regulation shock, an aggregate demand shock). In 25 years when economic historians such as myself will study the “Great Recession”, they will be forced to do like they do with Great Depression: tell a multifaceted story of intermingled causes and counter-effects for which no single statistical test can be designed. When cases like these emerge, it’s hard to tell what is happening and those who are willing to bet are daredevils.

P.S. I have seen the blog posts by Scott Sumner and Marcus Nunes regarding my NGO /NGDP claims. They make very valid points and I want to take decent time to address them, especially since I am using the blogging conversation as a tool to shape a working paper.

The Problem with Modern Monetary Theory

“Modern Monetary Theory,” a doctrine about fiat money, has captured the attention of some reformers and progressives. This doctrine – a set of propositions contrary to logic and evidence – purports to explain why the US and other economies are ailing, but is beset by contradictions with the historic facts and within the doctrine.

For example, The New Inquiry on 11 April 2014 featured an article by Rebecca Rojer on “The World According to Modern Monetary Theory.” The author regards it as a revelation of MMT that the “rules of money are not immutable laws of nature.” Since the science of economics explains the effects of incentives and decisions, evidently these money “rules” are the outcomes of private and governmental decisions, and since the effects are not immutable laws, people can arbitrarily create whatever outcomes they wish. That would indeed be wonderful, to just print money are thereby eliminate unemployment, depressions, and poverty, all without creating price inflation, because the rules of money creation are not immutable, so we can have whatever outcome we wish!

Science is based on logic and evidence rather than “revelations.” It is possible that there have been revelations, but these create religion rather than science, since if an experience or experiment cannot be duplicated, the revelations are not sufficient for scientific warrants. Various religions have had different revelations, and the members do not believe the revelations of the others.

The author provides an example of the MMT doctrine. Suppose there is an island that has minerals. The owner of the mines hires workers and pays them with fiat money, like the paper and bank-account money we have today, i.e. money created out of nothing. But the owner also imposes a tax on the wages of the miners. So evidently this mine owner is a government, and we are not dealing with private enterprise, but a coercive socialist state. The miners work enough to both pay the wage tax and be able to survive.

But a premise of this MMT island example is that prior to the mining, the people were able to hunt and farm without working too hard. So why would anyone work in the mines? The historical explanation is the “enclosures” movement, in which land that was held by small-scale farmers or by villages was forcibly taken by the aristocracy or by the state or by foreign invaders. This is not a money story, but a land-grab story. Another way to get forced labor, other than chattel slavery, is to require the payment of taxes in money, which forces subsistence farmers to work on plantations at least long enough to pay the taxes. That is more a tax story than a money story, since if the government insists on being paid in coconuts, and a farmer does not grow coconuts, he must work on the coconut plantation, get paid in coconuts, and then pay the tax. Therefore the forced labor is based on the government’s restrictions on alternative employment opportunities.

MMT is correct in stating that one way that the government gets people to accept its fiat money is what economists call the “fiscal theory of money,” that the government reinforces its money as a medium of exchange by requiring the use of that money for paying taxes. However, if the government currency is being hyper-inflated, taxpayers would keep their savings in, say, gold, or a stable foreign currency, and then convert it to the fiat money only when a tax payment is due. The fiscal effect only works if the government is not creating too much inflation.

Therefore MMT is incorrect as stating, as a “core building block,” that forcing people to pay taxes with fiat money “gives it its value.” That was not the case, for example, in Zimbabwe, which suffered hyperinflation. One “immutable” economic law of money is that the creation of money, beyond what is needed for transactions, results in price inflation, and the payment of taxes becomes tied to that inflation, via the nominal rise of prices and wages, rather than preventing inflation.

A related fallacy of MMT is that “sovereigns” in general create money by “spending it into existence.” That can indeed happen, as for example in the Zimbabwe hyperinflation, but in the US and most countries today, government spending comes from taxes and borrowing, not money creation. The central bank, such as the Federal Reserve, does not create money by spending it for goods, but rather by buying bonds and then increasing the banks’ reserves or funds to pay for the bonds.

Since the “core” proposition of MMT, that price inflation can be controlled by government’s taxing and spending, is incorrect, the whole superstructure of the MMT doctrine built on it collapses. Actually, MMT does accept the proposition that monetary inflation creates price inflation, but that true proposition contradicts the core MMT premise that tax-paying gives money its value.

A worse MMT fallacy is that the taxes paid to the government destroys money. MMT tells us that governments create money when they spend, and then the money disappears when taxes are paid. But a tax no more destroys money than the dollars used to buy bread. The seller of bread now has the money, and the government now has the dollars paid in taxes, and they then spend that money.

There have been various theories and doctrines on money and banking in the history of economic thought, and in my judgment, the explanations that best fit the facts are a combination of the monetarist and the Austrian schools of thought. The monetarist core is the equation MV=PT, which explains that the quantity of money (M) multiplied by its annual velocity or turnover (V) equals the price level (P) multiplied by the amount of transactions (T) measured in money. Thus high price inflation, a rise in P, is usually caused by monetary inflation, an on-going increase in M.

The Austrian school explains how excessive monetary inflation not only cause price inflation, but distorts relative prices, such as when house purchase prices rise faster than rentals. Austrian theory shows how governmental central planning fails because the knowledge to do so well is always lacking, and that applies to money as well. Hence the Austrians propose free-market money and banking, so that the market sets interest rates and the money supply.

Indeed the Fed failed to prevent the Great Depression of the 1930s and the Great Recession of 2008, and its policies generated high inflation during the 1970s and the cheap credit that has fueled land-value bubbles. MMT cannot do any better, because, as the Austrian theory explains, the optimal money supply is not only not known, but not knowable. The pure free market provides the optimal money supply just as it provides the optimal amount of bread and the optimal amount of shoes.

Weekly Wakeup 01-24-2014

Making this a quick copy paste job today. It has been a busy week.

To make a long story short, read this.

Myth: The Great Depression was caused by government inaction in the face of a failing economy.

Reality: The Hoover administration was the most active interventionist of a non-war economy in American history.

To quote the man himself:

“[W]e might have done nothing. That would have been utter ruin. Instead, we met the situation with proposals to private business and to Congress of the most gigantic program of economic defense and counterattack ever evolved in the history of the Republic. We put it into action.

No government in Washington has hitherto considered that it held so broad a responsibility for leadership in such times. . . . For the first time in the history of depression, dividends, profits, and the cost of living have been reduced before wages have suffered.”

And to quote the Murray Rothbard about Hoover’s actions:

At St. Paul, at the end of his campaign, Hoover summarized the measures he had taken to combat the depression: higher tariffs, which had protected agriculture and prevented much unemployment, expansion of credit by the Federal Reserve, which Hoover somehow identified with ‘protection of the gold standard’; the Home Loan Bank system, providing long-term capital to building-and-loan associations and savings banks, and enabling them to expand credit and suspend foreclosures; agricultural credit banks which loaned to farmers; Reconstruction Finance Corporation (RFC) loans to banks, states, agriculture, and public works; spreading of work to prevent unemployment; the extension of construction and public works; strengthening Federal Land Banks; and, especially, inducing employers to maintain wage rates. Wage rates ‘were maintained until the cost of living had decreased and the profits had practically vanished. They are now the highest real wages in the world.’ But was there any causal link between this fact and the highest unemployment rate in American history? This question Hoover ignored.

Hoover had, indeed, “placed humanity before money, through the sacrifice of profits and dividends before wages,” but people found it difficult to subsist or prosper on “humanity.” Hoover noted that he had made work for the unemployed, prevented foreclosures, saved banks, and “fought to retard falling prices.” It is true that “for the first time” Hoover had prevented an “immediate attack upon wages as a basis of maintaining profits,” but the result of wiping out profits and maintaining artificial wage rates was chronic, unprecedented depression. On the RFC, Hoover proclaimed, as he did for the rest of his program, “Nothing has ever been devised in our history which has done more for those whom Mr. Coolidge has aptly called the ‘common run of men and women.'” Yet, after three years of this benevolent care, the common man was worse off than ever.

Hoover staunchly upheld a protective tariff during his campaign, and declared that his administration had successfully kept American farm prices above world prices, aided by tariffs on agricultural products. He did not seem to see that this price-raising reduced foreign demand for American farm products. He hailed work-sharing without seeing that it perpetuated unemployment, and spoke proudly of the artificial expansion by business of construction “beyond present needs” at his request in 1929-30, without seeing the resulting malinvestment and business losses.

While claiming to defend the gold standard, Hoover greatly shook public confidence in the dollar and helped foster the ensuing monetary crisis by revealing in his opening campaign speech that the government had almost decided to go off the gold standard in the crisis of November, 1931—an assertion heatedly denied by conservative Democratic Senator Carter Glass.

The spirit of the Hoover policy was perhaps best summed up in a public statement made in May, before the campaign began, when he sounded a note that was to become all too familiar to Americans in later years—the military metaphor:

The battle to set our economic machine in motion in this emergency takes new forms and requires new tactics from time to time. We used such emergency powers to win the war; we can use them to fight the depression (321-323).

Some Mistakes Have Been Made

I just finished up the readings for a class on the history of the modern Middle East. The main book issued is one conveniently written by the professor of the course (James Gelvin) and is aptly titled The Modern Middle East: A History. Below is an excerpt that I think sums up the problems facing the Middle East today:

American policy towards the Middle East [after World War 2] was instrumental in promoting both development and the civic order development was to sustain […] To promote development, the United States adopted a multifaceted approach derived, in good measure, from its own Depression-era wartime experiences.

Ooops.

Here is Murray Rothbard’s America’s Great Depression. Now, I know libertarians are infamous for condescending suggestions to “go read a book”, but I don’t think we can really help it sometimes. Hoover’s interventionist policies and Roosevelt’s New Deal were disastrous for the American economy. Most, if not all, of the Middle East’s problems today can be traced to the institutions currently in place, and these institutions in their turn were created and codified based upon models that had entirely failed the West.

For the record, the developmentalist approach led directly to, you guessed it, economic nationalism and political despotism. You can find a convenient ranking of the world’s states based off of GDP (PPP) per capita here. According to the IMF, the US ($48,387) is ranked 6th in the world (the US also repealed or rebuked many of the Depression-era policies of the Hoover and Roosevelt administrations; the few that remain are among the most pressing problems American society faces today). The world average is $11,489. Egypt is ranked 104th, Iraq is 128th, Iran is 69th (coming in slightly above the world average at $13,053), and Syria is 118th.

National Economic Systems: an Introduction for Intelligent Beginners

Part One: Stimulation.

This essay does not require any specialized or advanced knowledge of economics. It does require an open mind and moderate alertness.

It’s must be difficult for the average working stiff with a job or school attendance, or both, a mortgage, and a family, to make sense of the daily economic news. It’s not because you are ill-informed, it’s because the media gives economic news in bits and pieces without tying them together, and usually without context. I suspect few of the big media commentators understand the context or try to link the fragments, anyway. Those who do understand tend to assume that everyone is aboard the same train they are riding. They don’t have much to say to those who are still at the station.

Major exceptions are the Financial Times, which has a strong pro-Obama bias, and the Wall Street Journal, which does not. Even with those, you have to read them every other day to get the big picture. So here, is the straight dope. (If you are concerned about my qualifications, a valid point, you will find a link to a fairly up-to-date version of my vita on the front of this blog.)

We are not facing one economic crisis but two. One is more or less routine, the other is almost unprecedented. The mildly re-assuring noises the media are currently making are about the first crisis, the almost-routine crisis only.

The first crisis is a conventional recession. Recessions are historically a normal part of capitalism. Healthy capitalist economies are on a growth path most of the time. There are several measures of economic growth and contraction. The easiest to understand is Gross Domestic Product, “GDP.” There are criticisms of this measure but we don’t care right now, for our narrow purpose.

GDPs grow at varying rate at different times and in different countries. A US GDP growth of 3.5 % per year makes nearly everyone happy. Countries that are at an early stage of development, such as India, and have a long way to go, often experience annual growth of 6% or 7%. China’s GDP growth has often topped 10% .Western European countries have been pleased with annual rates of growth of 2% for many years. There is a lesson here; don’t lose track of it.

National economies don’t always expand, sometimes, they contract. That’s a lot like the income of someone on an hourly wage instead of a straight salary. The prodigious economic growth of western countries under capitalism in the past 150 years is made up of series of expansions followed by contractions. We had overall growth because the contractions were both less in magnitude and shorter in duration than the periods of expansion.

The word “recession” means either two consecutive quarters of contraction of the national economy or it means any damn thing you want. Serious people only use the term in connection with the definition above. That’s what I do because I try to be a serious person.

Recessions are tricky because you only know about them after the fact, when the national statistics come out. Anyone who says, “We are in a recession” is either speculating or making propaganda. Economic commentators try to read the existence of a recession, and the waning of a recession, by studying other economic events. Those are events believed to be associated with recessions and to which numbers are attached that are collected frequently.

Here are two main ones: Unemployment figures and stock market indexes. There are others you can learn about if you become interested. When national unemployment goes down and the main stock market indexes go up for a while, commentators tend to announce the end of a recession. I think that liberal commentators give those a lot of weight under Democrat administrations, and conservative commentators under Republican administrations.

The reading of these signals is not an exact science, by a long shot. I just believe those readings are better than nothing if you take care to follow several. That’s a big “if,” of course.

Incidentally, there are very good scholarly, academic studies regarding the connections between various indicators and economic growth/contraction. I suspect few commentators keep abreast of those. I wouldn’t be surprised if it were none. I would be pleasantly surprised if some did.

Now, on to the current situation. When President Obama took office, it’s pretty clear the US was in a recession, or entering one. The President had nothing to do with it. There was much discussion everywhere about whether his buddies in Congress caused it. Fact is that there have been recessions with Republican as well as with Democratic administrations, and with Congressional domination of one or of the other major party.

The political elites of most countries, including many American Republicans believe in something called “Keynesian economics.” You don’t need to read Keynes to know as much as they do. Here is the gist: In modern developed societies, the government is such a large economic actor that it can influence decisively the path of the national economy. Thus, Keynesians believe that government has the power to stop or to improve on recessions. Governments may do this by engaging in spending, public spending, spending tax money, or borrowed money. (Keep I mind that, with the interesting exception of a few oil rich countries, governments have no money except what they can take in taxes and what they can borrow.)

Real conservatives, and libertarians who are not especially conservative, think that Keynesian economics is a dangerous hoax. They argue that government spending aggravated and deepened past recessions including the one associated with the Great Depression of the nineteen thirties. Fortunately, we don’t have to consider here who is right. (Full disclosure: I am one of them.)

A point that’s not in dispute is that government spending usually entails bigger government debt. More on this later.

Keynesian public spending is forthrightly intended to stem the spread of unemployment. The reasoning is simple: When people lose their job, or fear losing their job, they, and often, their neighbors, spend less. This lowered spending in turn slows down the national economy. This induces more unemployment: If I stop buying my daily latte because I am unemployed, or I fear I might soon be, and if others do the same, the barrista at my local coffee shop will lose her job. And so forth.

The fewer people earn a living, the smaller the national economy. If I merely forgo buying a car for the time being, the indirect effects on the national economy are even worse.

Hence, good Keynesian government spending should have very quick effects. It should stem the spread of unemployment rapidly and durably. It used to be the case that government had the ability to spend money quickly through public works. Hitler, for example, reduced quickly very high German unemployment by hiring the unemployed, and many underemployed, essentially to dig holes: Go to work in the morning; get a government check in the evening; spend the next day.

This approach has become difficult to employ for a variety of reasons, including permitting processes related to safety and to environmentalist zeal. Thus, if my city of Santa Cruz decides to build another breakwater for its harbor today, it’s unlikely anyone will get a paycheck for handling a tool for eighteen months, or more. Most past recessions lasted less than eighteen months.

As I write, only 10% or 15 % of the stimulus package money decreed by the President has been spent. Either, that’s not enough to stem the spread of unemployment, or, it’s not really a spending spree intended to stimulate. If the latter, what’s the purpose?

There is a beginning of an answer if you look at parts of the package that have a well-known name attached. One such is financing for a train from Disneyland to Las Vegas. It was put in by Harry Reid, the Senate Democratic Leader. There is no way the bulk of the corresponding money will be spent until five or even six years from now, except for studies employing a handful of specialists. Those specialists are not suffering from high unemployment, by the way. This part of the package does nothing to put to work Tom, Dick and Harry. The money won’t be spent for a long time because such a project needs a lot of planning, including for permitting to satisfy environmentalists.

What is the real purpose of this part of the stimulus package, then? At least, it makes Harry Reid look good with his voters. At worst, Harry Reed is using his muscle in Congress to satisfy special interests. I don’t know if the latter is true. I have not researched it. It’s plausible.

My conclusion: Even if you subscribe to Keynesian views on how to jump-start a national economy in recession, the measures taken by the administration six months ago do not work and cannot work.

Those who say, “Give it time” don’t know what they are talking about. The essence of government spending for stimulus purposes is speed. If you don’t stop and reverse unemployment quickly, the recessionary spiral worsens. If you did nothing at all, it would stop on its own, in good time, anyway.

Why do I care about the stimulus package’s lack of effectiveness?

Two reasons. First its part of a mass of unprecedented government spending. I mean unprecedented in the absence of a major war, like WWII. It increases public, government indebtedness to a worrying extent. Public debt has consequences, in the long run and in the not- so-long-run. More on this in the next episode of this posting.

The second reason, I care is that I detect a social and political project markedly different from the one announced by the administration in the current oversize government spending. I have not become a conspiracy theorist. I am relying on public information, including the President’s own past statements, those of his close advisers and, above all, my knowledge of what went on in Western Europe between about 1980 and 2000. I will address this alternative project in a subsequent posting also.

You have been good but there will be a quiz!

Current events update:

The Wall Street Journal has a good discussion of the Maine public health plan in today’s issue. It’s on p. A12, in the editorial section. It’s a fiasco. We care because it has important features in common with what we know of Obamacare.

Cool people tend to dismiss Rush Limbaugh, even conservatives. Limbaugh is bombastic and he exaggerates. That’s vulgar. However, he must have an army of good researchers because he comes up within a short time with hard evidence of allegations against his political adversaries. One of the wildest allegations from the right is that Obamacare entails “death boards.” Well, what do you know: Today, on-air, he reads excerpts from a Veterans Administration practitioner guidebook that sounds for all the world to me like a “death book.”

The convicted mass murderer of 270 people in the air over Lockerbie, Scotland receives a hero’s welcome in his home-country of Libya. He had been freed on compassionate grounds by the gutless Scottish Minister of Justice. (Yes, there is such a thing.) I saw it on television. This is not hearsay.

I think the enthusiasm greeting him in Libya should be written in the accounts book. It should enter into any calculus, side-by-side with collateral damage, next time this country has reason to consider bombing anything in Libya. It should not be long.

It’s unreasonable to treat in exactly the same way those who hate us and those who harbor sheer evil in their hearts, and our old friends. The stupid Scots should get a pass. The evil Libyans shouldn’t. There is no ethical system in the world that requires that this country do otherwise, not even Christianity. You are supposed to forgive your enemies after they have stopped harming you, not while they are cutting your throat, not even when they are impotently clamoring their wish to do it.

By the way, I am told by those who should know that Arabs respect this kind of thinking.

Austrian Economics and the Left

Matt Yglesias has a post up over at Slate.com on Ron Paul and Austrian Economics. I won’t get into the details of what he got right and wrong about his largely honest attempt to explain the Austrian School to Leftists (the word “crank” was only used once! A new high for the Left). Instead, what I’d like to do is hone in on this whopper:

Many of the original Austrians found their business cycle ideas discredited by the Great Depression, in which the bust was clearly not self-correcting […]

Has Yglesias conveniently forgotten about Hoover’s attempts to prop up wages and his signing of the protectionist Smoot-Hawley tariff?

Why don’t Hoover’s policies get more attention by economists and journalists trying to understand and explain the Great Depression, or am I missing something?

{kind=link}