A few days ago, John Avery Jones published a great piece on the Bank of England blog (“Bank Underground”), investigating how much Jane Austen earned from her novels in the early 1800s. By using the Bank’s own archives and tracking down Austen’s purchases of “Navy Fives” (Bank of England annuities, earning 5%), Avery Jones backed out that Austen’s lifetime earnings as a writer was probably something like £631 – assuming, of course, that the funds for this investment came straight from the profits of her novels.

Being a great fan of using literature to illustrate and investigate financial markets of the past, I obviously jumped on this. I also recently looked at the American novelist Edith Wharton’s financial affairs and got very frustrated with the way commentators, museums, and scholars try to express incomes of the past in “today’s terms”, ostensibly vivifying their meaning.

For the Austen case, both Avery Jones and the Financial Times article that followed it, felt the need to “translate” those earnings via a price index, describing them as “equivalent to just over £45,000 at today’s prices”.

Hang on a minute. Only “£45,000”? For the lifetime earnings of one of the most cherished writers in the English language? That sounds bizarrely small. That figure wouldn’t even pay for the bathroom in most London apartments – and barely get you a town-house in Newcastle. The FT specifically makes a comparison with contemporary fiction writers:

“[Austen’s] finances compare badly even with those of impoverished novelists today: research last year by the Authors’ Licensing and Collecting Society found that writers whose main earnings came from adult fiction earned around £37,000 a year on average”

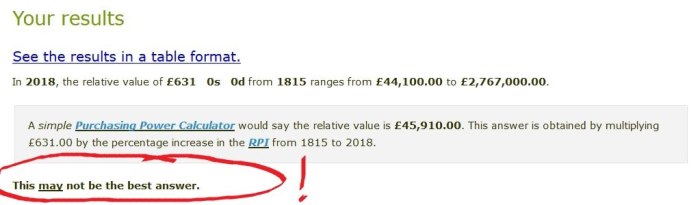

Running £631 through MeasuringWorth’s calculator yields real-price estimates of £45,910 (using 1815 as a starting year) – pretty close. But what I think Avery Jones did was adjusting £631 with the Bank’s CPI index in Millenium of Macroeconomic Data dataset (A.47:D), which returns a modern-day price of £45,047 – but that series ends in 2016 and so should ideally be another 7% or so from 2016 until May 2019.

“This may not be the best answer”

Where did Avery Jones go wrong in his translation? After all, updating prices through standard price indices (CPI/RPI/PCE etc) is standard practice in economics. Here’s where:

The third line on MeasuringWorth’s result page literally tells researchers that the pure price number may not reflect the question one is asking. The preface to the main site includes a nuanced discussion about prices in the past:

“There is no single ‘correct’ measure, and economic historians use one or more different indices depending on the context of the question.”

When I first estimated Mr. Darcy’s income, this was precisely the problem I grappled with; simply translating wealth or incomes from the past to the present using a price index severely understates the meaning we’re trying to convey – i.e., how unfathomably rich this guy was. There is no doubt that Mr. Darcy was among the richest people in England at the time (his annual income some 400 times a normal worker’s salary), a well-respected and wealthy man of elevated rank. However, translating his wealth using a price index doesn’t even put him on the Times’ Rich List over the thousand wealthiest Britons today. Clearly, that won’t do.

Because we are much richer today in real terms, price indices alone do not capture the meaning we’re trying to communicate here. Higher real income – by definition – is a growth in incomes above the rise in prices. We therefore ought to use a more tangible comparison, for instance with contemporary prices of food or mansions or trips abroad; or else, using real income adjustments, such as GDP/capita or average earnings.

MeasuringWorth provides us with three other metrics over and above the misleading price-index adjustment:

Labour Earnings = £487,000

using growth in wages for the average worker, it reports how large your wage would have to be today to afford what Austen could afford on £631 in 1815. Obviously, quality adjustments and technological improvements make these comparisons somewhat silly (how many smartphones, air fares and microwaves could Austen buy?), but the figure at least takes real earnings into account.

Relative Income = £591,300

Like ‘Labour Earnings’, this adjustment builds on the insight above, but uses growth in real GDP/capita rather than wages. It more closely captures the “relative ‘prestige value’” that we’re getting at.

Both these attempt are what I tried to do for Mr. Darcy (Attempt #2 and #3) a few years ago.

Relative Output = £2,767,000

This one is more exciting because it captures the relationship to the overall economy. If I understand MeasuringWorth’s explanation correctly, this is the number that equates the share of British GDP today with what Austen’s wealth – £631 – would have represented in 1815.

Another metric I have been experimenting with is reporting the wealth number that would put somebody in the same position in the wealth distribution of our time. For example, it takes about £2,5m to qualify for the top-1% of British wealth (~$10m in the United States) distribution today. What amount of wealth did somebody need to join the top 1% in, say, 1815? If we could find out where Austen’s wealth of £631 (provided her annuities were her only assets) rank in the distribution of 1815, we can back out a modern-day equivalent. This measure avoids many of the technical problems above for how to properly adjust for a growing economy, and how to capture inventions in a price index – and it gets to what we’re really trying to convey: how wealthy was Austen in her time?

Alas, we really don’t have those numbers. We have to dive deep into the wealth inequality rabbit hole to even get estimates (through imputed earnings, capital stocks or probate records) – and even then the assumptions we need to make are as tricky and inexact as the ones we employ for wage series or prices above.

The bottom line is pretty boring: we don’t have a panacea. There is no “single correct measure”, and the right figure depends on the question you’re asking. A reasonable approach is to provide ranges, such as MeasuringWorth does.

But it’s hard to imagine the Financial Times writing “equivalent of between £45,000 and £2,767,000 at today’s prices”…