This question is the one that me and Phil Magness have been asking for some time and we have now assembled our thoughts and measures in the first of a series of papers. In this paper, we take issue with the quality of the measurements that will be extracted from tax records during the interwar years (1918 to 1941).

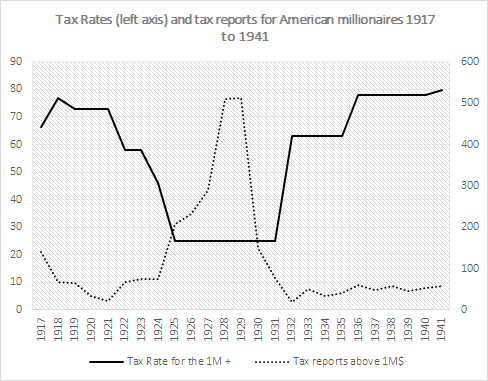

More precisely, we point out that tax rates at the federal level fluctuated wildly and were at relatively high levels. Since most of our inequality measures are drawn from the federal tax data contained in the Statistics of Income, this is problematic. Indeed, high tax rates might deter honest reporting while rapidly changing rates will affect reporting behavior (causing artificial variations in the measure of market income). As such, both the level and the trend of inequality might be off. That is our concern in very simple words.

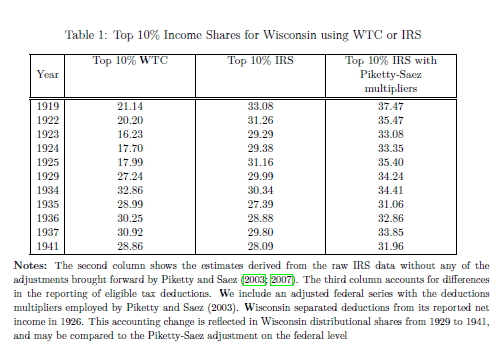

To assess whether or not we are worrying for nothing, we went around to find different sources to assess the robustness of the inequality estimates based on the federal tax data. We found what we were looking for in Wisconsin whose tax rates were much lower (never above 7%) and less variable than those at the federal levels. As such, we found the perfect dataset to see if there are measurement problems in the data itself (through a varying selection bias).

From the Wisconsin data, we find that there are good reasons to be skeptical of the existing inequality measured based on federal tax data. The comparison of the IRS data for Wisconsin with the data from the state income tax shows a different pattern of evolution and a different level (especially when deductions are accounted for). First of all, the level is always inferior with the WTC data (Wisconsin Tax Commission). Secondly, the trend differs for the 1930s.

I am not sure what it means in terms of the true level of inequality for the period. However, it suggests that we ought to be careful towards the estimations advanced if two data sources of a similar nature (tax data) with arguably minor conceptual differences (low and stable tax rates) tell dramatically different stories. Maybe its time to try to further improve the pre-1945 series on inequality.

{kind=link}