- How black-owned banks redefined risk in America Johnny Fulfer, Economic Historian

- Consistency: What everyone needs to know Irfan Khawaja, Policy of Truth

- Mao’s secret factories in Cold War China Lorenz M. Lüthi, War on the Rocks

- The irresistible rise of of the civilization-state Aris Roussinos, UnHerd

financial markets

13 Books for 2020 – What A Year!

2020 is turning into quite the publishing year.

Perhaps every year is like this and I just haven’t been paying attention before. Now, as I actively scan publisher sites and newsletters for upcoming books, there seems to be an abundance of super-interesting new stuff: how is anybody – even someone like me who does this for a living – supposed to keep up?

#1: The year began at full (or stagnating…?) speed with University of Houston professor Dietrich Vollrath‘s Fully Grown: Why a Stagnant Economy is a Sign of Success, With praise by Tyler Cowen and reviews in The Economist and the Wall Street Journal – and actually a lot of good discussions on Twitter – I’m sad that I haven’t taken time to read it. Later, perhaps, on the off-chance that nothing else on this incredible lists comes in the way.

#2: Next up was Diane Coyle‘s Markets, State, and People. Coyle, the endlessly interesting public intellectual/economist and newly(-ish) appointed Professor of Public Policy at Cambridge, is someone we all should read: she manages to be controversial and still balanced, provocative but still interesting. This book, however, seems to be in line with all the other “Third Way” books of last year: Acemoglu and Robinson’s The Narrow Corridor; Raghuram Rajan’s The Third Pillar; Branko Milanovic’s Capitalism, Alone. Crowded field. As I haven’t even gotten around to her previous book on GDP yet, I imagine I’ll read that one first whenever I carve out some time for Coyle.

The curse of modernity is quickly adding up.

#3: Changing gears somewhat – at least in terms of topics – I have started reading Charles Murray‘s Human Diversity: The Biology of Gender, Race, and Class and it’s exactly as provocative as you might think. Delivered, however, with the seriousness of scientific investigation and a massive chip on his shoulder. Still, exactly the kind of antidote to madness that fuels a lot of my priors. I’ll write up a comment or two whenever I finish this 528-page tome.

#4: In a similar vein is the Dutch writer and historian Rutger Bregman‘s Humankind: a Hopeful History, scheduled to be released in June. As Bregman isn’t somebody that I usually agree with, I’m very excited to read this take of his, which is hopefully a mix of Paul Bloom’s End of Empathy, Ruth DeFries’ The Big Ratchet and Paul Seabright’s The Company of Strangers. Sort of like Yuval Harari’s Sapiens but better (and no, I’m not on Team Harari – despite this excellent long-read in The New Yorker).

#5: Going back a little bit to what I think is chronologically the next book to be released (on Tuesday March 10 in the U.S., but not until April in the U.K.) is Robert Bryce’s A Question of Power: Electricity and the Wealth of Nations. Having recently written a piece on electricity generation and being into the weeds about climate change and emissions, I’m very curious about this take on electricity as a critical source for our prosperity. I hope it reads a little like an improved version of Zubrin’s best chapters in Merchants of Despair.

#6: March is also the month for Angus Deaton and Anne Case‘s Deaths of Despair and the Future of Capitalism (Amazon says it’s already out in the U.K.) Their hugely successful and highly relevant pet project for the last few years, Deaton and Case’s case(!) for how rising morbidity rates indicate a collapse of the fabric of society is a pretty standard one by now: globalization, economic inequality, the hollowing-out of tight-knit communities and the various forces that may have fueled this.

The reviews are already popping up left and right (WSJ, Financial Times) and their session was the most exciting and most talked-about at the ASSA meeting in San Diego. As I understand it, the latest findings is that American life expectancy – that pesky ever-increasing number that fell in recent years, in no small part due to overdoses and opioids – has recovered and is now again on the up-tick. Maybe Deaton and Case’s book will be one for an odd historic event rather than foreshadowing “The Future of Capitalism” (also, what’s up with shoving ‘Future of Capitalism’ into your titles?!).

#7: In a similar topic, Robert Putnam – yes, the Harvard professor famous for Bowling Alone and the idea of social capital – is back with another sweeping analysis of what’s gone wrong with American society. The Upswing: How America Came Together a Century Ago and How We Can Do It Again, coming out in June, is bound to make a lot of waves and receive a lot of attention by social commentators.

#8: Officially published just yesterday is John Kay and former Bank of England Governor Mervyn King‘s Radical Uncertainty: Decision-Making for an Unknowable Future. Admittedly, this is the book I’m least excited about on this list. Reviewing King’s 2016 End of Alchemy – where King discussed his experiences of the financial crisis and the global banking system – for the Financial Times, John Kay discussed exactly that: the title? “The Enduring Certainty of Radical Uncertainty.” Somebody please press the snooze button. Paul Krugman’s 4000 word review of End of Alchemy ought to be enough; I’d be surprised if Kay and King brings something new to the table in thus poorly-titled release (though, of course the fringe already loves it).

The Really Good Stuff

While the above eight titles are surely worth at least some of your time, the next five are worth all of it.

#9: I’ll begin with my two biggest hypes: Matt Ridley‘s How Innovation Works: And Why It Flourishes in Freedom, coming out May 14th in the U.K. and May 19th in the U.S. The author of The Rational Optimist and The Evolution of Everything is back with another 400-page rundown of a deep-seated and hyper-relevant topic: how do societies innovate and progress? What conditions assist it, and which obstacles prevent it?

I expect a lot of spontaneous order-type arguments, debunked Great Man fallacies, and some Mariana Mazzucato take-downs.

#10: The second hype, William Quinn and John Turner‘s Book and Bust: A Global History of Financial Bubbles. Since John first told me about this book over a year-and-a-half ago, I’ve been super excited – I’m a big fan of his work – and I’m looking forward to receiving my review copy in the next couple of weeks. Publication date: August.

#11: For somebody who writes about bubbles and financial markets more than most people think healthy, I’m gonna get a warm-up in MIT professor Thomas Levenson‘s Money for Nothing: The South Sea Bubble & The Invention of Modern Capitalism. What’s with all these books on historical financial bubbles? Yes, you’re right: 2020 marks the three-hundred year anniversary of the South Sea Bubble, that iconic period of John Law in France and the similar government funding scheme in England will surely receive a lot of attention this year.

#12: Some environmental stuff at last: Bjørn Lomborg, the outspoken author and voice of reason in the climate change space announced that his False Alarm: How Climate CHange Panic Costs Us Trillions, Hurts The Poor, and Fails To Fix the Planet will be published in June this year! While possibly the least boring book on this list, the title receives lowest possible marks. What overworked publisher decided that this page-long subtitle was a good idea?!

#13: Also, Alex Epstein of the Centre for Industrial Progress and host of Power Hour (one of my all-time favorite podcasts) has been working on an update to his hugely popular The Moral Case for Fossil Fuels. As far as I understand, we’re to receive an updated and revised version in August – the Moral Case for Fossil Fuels 2.0!

So. The next six months have at least thirteen pretty interesting books coming up. I imagine there are a bunch more for the rest of the year – and a few I have completely overlooked.

Also, after this burst of links, Amazon should probably offer Notes On Liberty an affiliate program.

In sum: you can see my fields of interests overlapping here: (1) financial history and financial markets; (2) environment, climate change, and its solutions; (3) Big Picture society stories, preferably by interesting or quantitatively savvy authors. Not enough on the fourth big interest of mine: (4) money and monetary economics – particularly in historical contexts. Perhaps not, as David Birch’s Before Babylon, Beyond Bitcoin is on my desk, and I’m currently re-reading William Goetzmann’s Money Changes Everything – both first released in 2017.

Also: the absence or underrepresentation of women (or ethnic minorities or any other trait you care a lot about) might disturb you: 2 out of 17 authors women (4 out of 27 authors mentioned) – Needless to say, it must be because I’m sexist.

Post-script: Ha! As I just heard about Stephanie Kelton‘s upcoming book The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy, I’m gonna quickly add it to the list and satisfy both of my qualms above: not enough women (now: 3/18 authors!), and not enough monetary economics. Splendid!

Happy reading, everyone!

Financial History to the Rescue: The Harder Money Wins Out

This article is part of a series on bitcoin (and bitcoiners’) arguments about money and particularly financial history. See also:

(1) ‘On Bitcoiners’ Many Troubles’, Joakim Book, NotesOnLiberty (2019-08-13)

(2): ‘Rothbard’s First Impressions on Free Banking in Scotland Were Correct’, Joakim Book, AIER (2019-08-18)

(4): ‘Bitcoin’s Fixed Money Supply Is a Weakness’, Joakim Book, AIER (2019-08-28)

The great monetary economist and early Nobel Laureate John Hicks used to say that monetary theory “belongs to monetary history, in a way that economic theory does not always belong to economic history.”

Today I’m going to illustrate exactly that with respect to the Bitcoiner’s (mistaken) progressivism in another episode of Financial History to the Rescue.

In the game of monetary competition, the Bitcoin maximalists posit, the “harder” money always wins out. I’ve been uneasy with the statement as it (1) isn’t clear to me what “harder” money (or money’s “hardness”) really means, and (2) probably isn’t historically true. So we end up with something that’s false, or vague – or both! Clearly unsatisfactory. As I pointed out in my overview post to this series, financial and monetary history is almost always more nuanced than what such simple generalizations allow.

Luckily enough, Saifedean Ammous at the Soho Forum debate last week, did inadvertently provide me with a useable definition – and I intend to use it to debunk the idea that money’s history is one of increased hardness. Repeatedly Saif claimed that monetary history, before the advent of central banking, showed us that the harder money always won out: whenever two monetary networks clashed (shells and silver; wampum and gold) the “harder” money won. The obvious implication is that Bitcoin, being the “hardest” money, will similarly win out. Right off the bat, there’s some serious problems here.

First, it’s not altogether clear that such “This time is not different” arguments apply. Yes, economic history teaches us not to discount what seems to be long-standing or universally applicable phenomena – but also to take notice of the institutional setting in which they happen. Outcomes specific to, say, the Classical Gold Standard, rarely generalize into our hyper-modern financial markets with inflation targeting central banks.

Second, over the twentieth century we literally went from the hardest money (gold) to the “softest” money (central bank-created fiat paper money). Sure, you can argue that this was unfair or imposed upon us from above by wars and welfare states, but discounting it as irrelevant strikes me as overly cherry-picking. If the hardest money “lost” before, what makes you think that your new fancy money will win out this time around?

Then Saif returned to the topic of hardness and defined it as a money whose supply is “the hardest to increase.” The hardness of Cowrie shells or Wampum or gold or Whale’s teeth or Rai stones or the other early money that Jevons listed and discussed in 1875, all rely on a difficult, costly and inconvenient process of extraction and/or production. Getting Rai stones from far-away islands, stringing beads together into extended strips of Wampum, or digging up gold from inaccessible patches of the earth were all cumbersome and expensive processes. In Saif’s mind, this contributed to their hardness. Their money stock were simply difficult to expand – in jargon: their money supplies were inelastic.

The early 1600s Dutch Republic struggled with another problem. As the main financial centre of the time, countless hard money (coins) from all over the world were used in Amsterdam. Estimates say over a thousand legally recognized kinds of coins – and presumably even more unrecognized coins. A prime setting for monetary competition: they were all pretty hard (Saif’s definition: difficult and costly to expand) commodity moneys, of various quality, origin, and recognition in trade.

Another feature of 17th century Amsterdam was the international environment of Bills of Exchange (circulating private credit notes). Briefly summarized, merchants across the world traded debts on Amsterdam bankers or traders, and rather than holding and transporting bullion across the world, they transported the debt of the most trustworthy and reliable Dutch financiers. As all such bills required a settlement medium in Amsterdam, trade on thin margins was very sensitive to fluctuations in prices between the commodity moneys in which their bills were denominated – and very sensitive to debasements and re-defined values by various European proto-governments.

In 1609, the City of Amsterdam created the Wisselbank (initially a 100% reserve exchange bank) specifically tasked with standardizing the coinage and to insulate the bill market from currency fluctuations (through providing a ‘neutral’ unit of account for bills settlement). The Bank accepted deposit of whatever coin at the legally recognized rate (unrecognized at metal content) and delivered ”high-quality Dutch trade coins” upon withdrawal. To fund itself, it added a withdrawal fee of 1.5%, but no internal transfer fee, which made holding currency at the Bank very expensive in the short-term, but very cheap in the long-term. Merchants also avoided much of the withdrawal fee by simply trading balances with one another rather than depositing and withdrawing trade coins. In return for this cost-saving, sellers of bank balances would share a portion of the funds saved with the buyer in what’s known as the “Agio”: the price of Bank money in terms of current money outside the Bank’s accounts. This price would fluctuate like any other price on the market and would indicate the stance of liquidity demands.

In a classic example of Alchian’s monetary competition by transaction costs, Dutch merchants and financiers “outsourced” the screening and assaying of unfamiliar coins. They preferred settling their transactions through the (cheaper) medium that was deposits in the Bank.

And it gets worse for the bitcoiner’s story. In 1683, the Bank coupled its deposits with specific receipts for withdrawal; to gain access to coins, one was required both to hold balances and to purchase a receipt issued by the Bank (they also changed the pricing). Roughly speaking, the Bank became a fractional reserved bank (with capped withdrawals) overnight – and contrary to what the hardness argument would imply, the agio on Bank money rose to above par!

Two monetary historians, Stephen Quinn and William Roberds, summarize one of their many writings on the Wisselbank as follows:

“imaginary money on the Bank’s ledgers succeeded because it was more reliable than the real stuff. […] The most liquid asset in the economy was no longer coin, but a sort of ‘virtual banknote’ residing in Bank of Amsterdam accounts.”

Further,

“the evolution of the agio shows that the market valued irredeemable balances as if they were closely tied to backing trade coins” (my emphasis)

The story of the Amsterdam Wisselbank’s monetary experiments and innovations show us that monetary adaption relies on many more dimensions than “hardness.” Sometimes “hard” money is defeated by “soft” money, since the softer money brought other benefits to its users – in this case a cheap and reliable settling medium.

The lesson for bitcoin-vs-fiat-vs-FinTech is pretty clear: hard money doesn’t always “win”; and sometimes “soft” money can better serve the needs of consumers in a free market.

On Translating Earnings From The Past

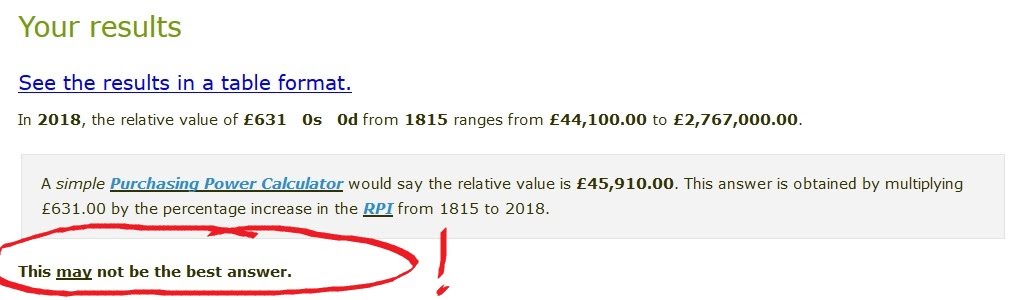

A few days ago, John Avery Jones published a great piece on the Bank of England blog (“Bank Underground”), investigating how much Jane Austen earned from her novels in the early 1800s. By using the Bank’s own archives and tracking down Austen’s purchases of “Navy Fives” (Bank of England annuities, earning 5%), Avery Jones backed out that Austen’s lifetime earnings as a writer was probably something like £631 – assuming, of course, that the funds for this investment came straight from the profits of her novels.

Being a great fan of using literature to illustrate and investigate financial markets of the past, I obviously jumped on this. I also recently looked at the American novelist Edith Wharton’s financial affairs and got very frustrated with the way commentators, museums, and scholars try to express incomes of the past in “today’s terms”, ostensibly vivifying their meaning.

For the Austen case, both Avery Jones and the Financial Times article that followed it, felt the need to “translate” those earnings via a price index, describing them as “equivalent to just over £45,000 at today’s prices”.

Hang on a minute. Only “£45,000”? For the lifetime earnings of one of the most cherished writers in the English language? That sounds bizarrely small. That figure wouldn’t even pay for the bathroom in most London apartments – and barely get you a town-house in Newcastle. The FT specifically makes a comparison with contemporary fiction writers:

“[Austen’s] finances compare badly even with those of impoverished novelists today: research last year by the Authors’ Licensing and Collecting Society found that writers whose main earnings came from adult fiction earned around £37,000 a year on average”

Running £631 through MeasuringWorth’s calculator yields real-price estimates of £45,910 (using 1815 as a starting year) – pretty close. But what I think Avery Jones did was adjusting £631 with the Bank’s CPI index in Millenium of Macroeconomic Data dataset (A.47:D), which returns a modern-day price of £45,047 – but that series ends in 2016 and so should ideally be another 7% or so from 2016 until May 2019.

“This may not be the best answer”

Where did Avery Jones go wrong in his translation? After all, updating prices through standard price indices (CPI/RPI/PCE etc) is standard practice in economics. Here’s where:

The third line on MeasuringWorth’s result page literally tells researchers that the pure price number may not reflect the question one is asking. The preface to the main site includes a nuanced discussion about prices in the past:

“There is no single ‘correct’ measure, and economic historians use one or more different indices depending on the context of the question.”

When I first estimated Mr. Darcy’s income, this was precisely the problem I grappled with; simply translating wealth or incomes from the past to the present using a price index severely understates the meaning we’re trying to convey – i.e., how unfathomably rich this guy was. There is no doubt that Mr. Darcy was among the richest people in England at the time (his annual income some 400 times a normal worker’s salary), a well-respected and wealthy man of elevated rank. However, translating his wealth using a price index doesn’t even put him on the Times’ Rich List over the thousand wealthiest Britons today. Clearly, that won’t do.

Because we are much richer today in real terms, price indices alone do not capture the meaning we’re trying to communicate here. Higher real income – by definition – is a growth in incomes above the rise in prices. We therefore ought to use a more tangible comparison, for instance with contemporary prices of food or mansions or trips abroad; or else, using real income adjustments, such as GDP/capita or average earnings.

MeasuringWorth provides us with three other metrics over and above the misleading price-index adjustment:

Labour Earnings = £487,000

using growth in wages for the average worker, it reports how large your wage would have to be today to afford what Austen could afford on £631 in 1815. Obviously, quality adjustments and technological improvements make these comparisons somewhat silly (how many smartphones, air fares and microwaves could Austen buy?), but the figure at least takes real earnings into account.

Relative Income = £591,300

Like ‘Labour Earnings’, this adjustment builds on the insight above, but uses growth in real GDP/capita rather than wages. It more closely captures the “relative ‘prestige value’” that we’re getting at.

Both these attempt are what I tried to do for Mr. Darcy (Attempt #2 and #3) a few years ago.

Relative Output = £2,767,000

This one is more exciting because it captures the relationship to the overall economy. If I understand MeasuringWorth’s explanation correctly, this is the number that equates the share of British GDP today with what Austen’s wealth – £631 – would have represented in 1815.

Another metric I have been experimenting with is reporting the wealth number that would put somebody in the same position in the wealth distribution of our time. For example, it takes about £2,5m to qualify for the top-1% of British wealth (~$10m in the United States) distribution today. What amount of wealth did somebody need to join the top 1% in, say, 1815? If we could find out where Austen’s wealth of £631 (provided her annuities were her only assets) rank in the distribution of 1815, we can back out a modern-day equivalent. This measure avoids many of the technical problems above for how to properly adjust for a growing economy, and how to capture inventions in a price index – and it gets to what we’re really trying to convey: how wealthy was Austen in her time?

Alas, we really don’t have those numbers. We have to dive deep into the wealth inequality rabbit hole to even get estimates (through imputed earnings, capital stocks or probate records) – and even then the assumptions we need to make are as tricky and inexact as the ones we employ for wage series or prices above.

The bottom line is pretty boring: we don’t have a panacea. There is no “single correct measure”, and the right figure depends on the question you’re asking. A reasonable approach is to provide ranges, such as MeasuringWorth does.

But it’s hard to imagine the Financial Times writing “equivalent of between £45,000 and £2,767,000 at today’s prices”…

Those revenue-raising early central banks

In a piece on a rather different topic, George Selgin, director for the Center for Monetary and Financial Alternatives and editor-in-chief of the monetary blog Alt-M, gave a somewhat offhand comment about the origins of central banks:

For revenue-hungry governments to get central banks to fund their debts is itself nothing new, of course. The first central banks were set up with little else in mind. (emphasis added)

Writing about little else than (central) banks in history, you can imagine my surprise:

Reasoned response: Selgin ought to know better than buying into this simplified argument.

Less reasoned response, paraphrasing one of recent year’s most epic tweets: you come into MY house?!

Alright, let’s make a quick run-through, then. Clearly, some simplification and lack of attention to nuances is permissible under the punchy poetic licenses of the economic blogosphere – especially so when the core of an argument lies elsewhere. But the conviction that early central banks

(a) were created as revenue-raising devices for their governments, or

(b) all central banks provided their governments with direct fiscal benefits,

is a gross simplification of a much broader and much more diverse history of early public banks. Additionally, the misconception entails what Italian banking scholar Curzio Giannini derisively referred to as overly-narrow “fiscal theor[ies] of central banks”. Since too many people believe some version of the argument, let’s showcase the plethora of early central banks and illustrate their diverse experiences.

Initially, the banks-as-fund-raisers argument may seem reasonable; a few proto-central banks definitely were set up with this purpose in mind, with the Bank of England’s series of monopoly charters beginning in 1694 as the prime example. David Kynaston, the great historian of the Bank, eloquently characterized the relation between the government and the Bank as a ‘ritualistic dance’ in light of the periodic renewals of its monopoly charter; the Bank provided the government with funds and in return received some new privilege in addition to lucrative interest payments.

Among the dozen or so other candidates reasonably fitting the description “first central banks”, we see a wide variety of purposes, not all of which were principally – or even at all – concerned with funding their governments.

Banco di San Giorgio (Genoa, 1407), was essentially a precursor of money market funds with investors holding the City state’s debt and receiving taxing rights. Here, as in many of the northern Italian city-state banks of the 14th and 15th century, the banks-as-fund-raisers argument seems applicable (we might mention others here too, like the Catalonian Taula de Canvi, 1401, that is often considered the first public bank). Whether or not these first generation banks may be counted as “central banks” is much less doubtful, but a topic for another day.

Amsterdam Wisselbank (1609), a much-studied institution and a trailblazer in the history of central banking, was primarily set up to facilitate payments, specifically to simplify the chaotic muddle of coins and payment methods that abounded in the Low Countries during the 1500s and 1600s. The Bank’s lending was circumscribed, and the lending that did take place often went to the Dutch East India Company – of course, we might argue that the Dutch East India Company, with its directors appointed by the Dutch provinces, actually constituted an arm of the government and so counting this lending as government financing. Besides, the City only began using the Wisselbank for financing purposes firstly through a loan in the 1650s and then more frequently towards the end of the 17th century. Regardless, those are (decades removed) outcomes – not initial purposes.

Hamburger Bank (1619) was similarly set up with monetary stabilization in mind and adopted many of the features of the Wisselbank. Contrary to the Wisselbank, it had a credit department that right away engaged in lending to private parties on collateral. However, it seems that most of its funds were lent to the Kämmerei (municipality treasury). In economists William Roberds and Francois Velde’s account, the

problems with circulating coinage in early seventeenth-century Hamburg were, if anything, worse than in Amsterdam.

A partial vindication, at best, for the banks-as-fund-raisers argument since the Hamburger Bank was clearly set up with monetary stabilization in mind rather than government financing. In practice, however, it did finance the city.

The Riksbank: (Stockholm, 1668). Picking up from its failed predecessor ‘Stockholms Banco’, what later became known as Sveriges Riksbank (frequently credited with being the first – surviving – central bank) was tasked with facilitating trade and upholding the value of the domestic currency. In practice, this meant influencing the foreign exchanges as they stood in Hamburg or Amsterdam. Initially, the bank was explicitly prohibited from extending funds to the crown (in early 2019 there has emerged a dispute over this point among some Swedish financial historians). What is clear is that for the first fifty years or so of the bank’s existence, the rule seems to have mostly held up; not until the Great Northern Wars in the early 1700s did the Riksbank to any meaningful extent advance funds to the government.

Bank of Scotland (1695) and the Royal Bank of Scotland (1727), were both – a bit like the Riksbank – chartered to advance and improve the functioning of the domestic economy, and they were prohibited from lending to the crown. Despite the well-known political conflicts leading to the chartering of the Royal Bank, the Scottish case of rivaling banks were clearly created to advance the North Sea trade, not to finance the government or manage its debt. The third chartered Scottish bank, the British Linen Company (1745) was formed in order “to carry on the linen manufactory”. As is often the case in banking history, the Scottish case might thus be the clearest counterpoint to an argument. Further, the Scottish banking historian Sydney Checkland pointed out that the Bank of Scotland was “solely dependent on private capital, and […] wholly unconnected with the state.”. Again, the No True Central Bank objection might be raised, but it would send us tumbling into a dark definitional hole that has to wait for another time.

Banco del Giro/Wiener Stadtbank (Vienna, 1703 and 1705) were both established as a result of “the poor state of Austrian public finance” Like in Venice and Genoa, the banks were meant to enhance the liquidity of the government’s debt, actively contributing to reducing the State’s and the City’s interest rates respectively – and then gradually pay back their debt. While both banks did accept private deposits, and like its Hamburg and Dutch predecessors facilitated payments through their ledgers, these operations were clearly not their prime purposes. Money-raising argument vindicated.

This brief overview of some early central banks illustrate the point: banking history contains much wider experiences than a simplified money-raising argument implies. Indeed, even the First Bank of the United States – clearly an aspiring candidate to the title of ‘first’ central banks’ – seems to primarily have had trade-enhancing and economic development purposes in mind. This I say much hesitantly, since early American banking is definitely not my forte and I fully expect Selgin (and others) to correct me here.

Regardless, to claim that early (central) banks were set up with government finance in mind, is clearly an overstatement.

___

The title is a play on my favorite of George Selgin’s many brilliant articles, ‘Those dishonest goldsmiths’.

For the record, George Selgin is well-versed in this literature, and I’m merely using his quote as a stand-in for a common conviction among the not-so-well informed academic crowd.

Two Financial Instruments that made the Modern World

Following my Mr. Darcy piece that outlined the use and convenience of British government debt instruments in the eighteenth (and predominantly the nineteenth) century, I thought to extend the discussion to two particular financial instruments. In addition to the Consols (homogenous, tradeable perpetual government debt) that formed the center of public finance – and whose active secondary market that made them so popular as savings devices – the Bill of Exchange was the prime instrument used by merchants for financing trade and settling debts.

The complementarity of the Consol and the Bill in international finance, roughly from the South Sea Bubble (1720) to the end of Napoleon (1815), was the “secret of success for international finance” (Neal 2015: 101) and arose without an overarching plan, i.e. rather spontaneously. As the Consol is more easily understood for a modern reader, and the Bill is both more ancient and less well understood, I’ll focus the bulk of my attention on the latter.

According to Anderson (1970: 90), the Bill constituted “a decisive turning-point in the development of the English credit system,” but is much older than that. In practice, it was a paper indicating debt and a time for repayment, allowing financing of current trade. Cameron (1967:19) writes that the Bill

was far more ancient than either the banknote or the demand deposit; it had been developed in the Middle Ages. At first the bill was used as a device for avoiding the cost and risks of shipping coin or bullion over great distances, then as a credit instrument which circumvented the Church’s prohibition of usury. When it first came to be used as a means of current payment is a moot question that may never be answered, but that it was so used in eighteenth-century England is beyond doubt.

The Bill was predominantly used in coastal cities in the Mediterranean and around the North-Sea, becoming frequent perhaps in the 1700s. One observer even dates an early instance of its use to 1161, and it was of standard use among traveling traders, merchants and brokers throughout the Middle Ages (Cassis & Cottrell 2015: 12). Occasionally – warranting a discussion of its own – Bills in England became “so widespread that they drove out even banknotes” (Cameron 1967: 19).

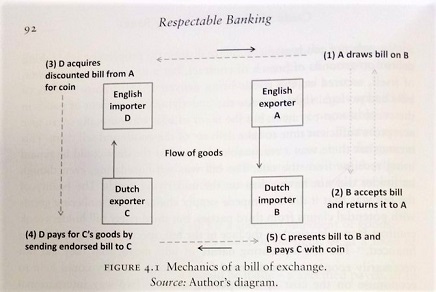

There is an unfitting competition among financial historians as to who can produce the most persuasive, informative or complicated schedule for how Bills worked (I know of at least four similar, yet uncredited, renditions). Here’s Anthony Hotson’s (2017: 92) attempt from last year:

- We start, counter-intuitively, in the top-right corner. Andrew, an English exporter of Apples, draws up a Bill on Bas, a Amsterdam maker of Bankets – a Dutch pastry. Bas, having no coin/gold available to pay Andrew – either because he won’t have the funds until after he has sold his apple-flavored(!) Bankets, or because the risk of loss or cost of transportation is too great – accepts the Bill and returns it to Andrew.

- Having returned it to Andrew, we now have a debt and a financial instrument; Bas has promised to pay Andrew £x for the apples in 90 days, a common duration for a Bill of exchange.

- But like most merchants, Andrew cannot wait 90 days for payment; he has sold and shipped his Apples, but needs funds for himself (feeding his family, or investing in new Apple-harvesting equipment etc). In the heyday of British financial markets, Andrew could simply visit a bank, Bill-broker or the London financial markets himself, and offer to sell the Bill there. Of course, Andrew won’t be able to sell the Bill for £x, since his buyer is effectively providing him with a loan for 90 days. The bank, bill-broker or financial market trader will discount the Bill with the going interest rate (say 6%, for one-quarter of a year, so ~1.5%), paying at most £0.985x for the Bill. Besides, there is a risk-of-default element involved, so the buyer applies a risk premium as well, perhaps buying the Bill at £0.95x.

- In the schedule above Hotson uses the Bill trade to show how merchants trading Bills could net out their respective debts and minimize the need to send payment across the British channel. For (3) and (4), then, we replace the banker with an English importer – Dave – of Dutch goods (perhaps tin-glazed pottery) looking for a way to pay his Amsterdam pottery supplier, Cremer. Instead of shipping gold to Amsterdam, Dave may purchase Andrew’s Bill, and settle his account with Cremer by sending along the Bill drawn on Bas. Once the 90 days are up, Cremer can simply wander over to Bas’ pastry shop and present him with the Bill to receive payment for the goods Cremer already shipped to England.

This venture can – and usually was – made infinitely more complicated; we can add brokers and discounting banks in every transaction between Andrew, Bas, Dave and Cremer, as well as a number of endorsers and re-discounters. In his popular book Exorbitant Privilege, Barry Eichengreen recounts a 12-step, several-pages long account for how a U.S. importer of coffee and his Brazilian supplier both get credit and signed papers from their local (New York + Brazil) banks, how both banks send their endorsed bills to their London correspondent banks, and some investor in the London money markets purchase (and perhaps re-sell) the Bill that eventually settles the transaction between the American coffee importer and the Brazilian farmer.

Although it might sound excessive, complicated and impossible to overlook, the entire process simplified business for everyone involved – and allowed business that otherwise couldn’t have been done. In econo-speak, the Bill of Exchange set within a globalizing financial system, extended the market for merchants and farmers and customers alike, lowered transaction costs and solved information asymmetries so that trade could take place.

Turning to the opposite end of the maturity spectrum, the Consol as a perpetual debt by the government was never intended to be repaid. Having a large secondary market of identical instruments, allowed investors or financial traders everywhere to pass Gorton’s No-Questions-Asked criteria for trade. A larger market for government debt, such as after Britain’s wars in the late-1700s and early 1800s, allowed dealers in financial markets to a) be reasonably certain that they could instantly re-sell the instrument when in need of cash, and b) quickly and effortlessly identify it. These aspects contributed to traders applying a smaller risk premium to the instrument and to be much more willing to hold it.

While the Bills were the opposite of Consols in terms of homogeniety (they all consisted of different originators, traders, and commodities), there developed specialized dealers known as Discount Houses whose task it was to assess, buy, and sell Bills available (Battilosso 2016: 223). Essentially, they became the credit rating institutions of the early modern age.

Together these two instruments, the Bills of Exchange and the Consols, laid the foundations for the modern financial capitalism that develops out of the Amsterdam-London nexus of international finance.

Mr. Darcy’s Ten Thousand a Year

On popular demand, I’m reviving a reoccurring theme of mine: teaching economic history through the lens of popular culture. Today: bonds, yields and 18th century English financial planning.

In what is probably my favourite piece ever written, I tried to estimate exactly how rich Mr. Darcy was – Mr. Darcy, of course, of Jane Austen’s classic novel Pride & Prejudice. I showed that whatever method you use to translate incomes to the present, all characters in Austen’s captivating story are astonishingly rich. But, as we well know today, there are large differences even among the superrich; compare Bernie Sanders (small-time millionaire) with George Lucas and Steven Spielberg (single-digit billionaires) or Jeff Bezos (wealthiest man alive).

Using Pride & Prejudice to illustrate some economic point is hardly unconventional (Piketty did this in his Capital in the Twenty-First Century), so let me similarly discuss 18th and 19th century British financial markets using the characters in this well-known tale.

The starting point is the following musing, courtesy of former Oxford Economist Martin Slater’s (2018: 52) The National Debt; how come “female characters in nineteenth-century novels always seem to have a suspiciously exact income of ‘so many pounds per year'”? Where does this money come from? Why is it so exact? And what’s the reason Piketty uses this particular literary example to illustrate the permanence and steady stream of income that capital somehow just throws off?

Consols and Financial Markets

Financial markets are truly awesome – not just in their impressive scope or potential devastation, but in the many different needs they simultaneously fulfil for many different people. Slater ably guides us through the confusing mishmash that is the 17th and 18th century English public finance, but what emerges by 1757, after Henry Pelham’s consolidation of government debt, is two main – and for our purposes, equivalent – securities: the Consolidated 3% Annuities (and the ‘Reduced annuities’), affectionately named ‘Consols’. These were permanent government bonds with annual interest payments of 3%. This means that they had no maturity date, i.e. the holder of the security could expect the government to keep paying 3% of the face value for all future (a Churchill-issued subsequent Consol was actually repaid and retired just a few years ago, after almost a century in service).

Two cool things happen. First, the “initial value” – the face value – of debt running in perpetuity becomes almost irrelevant, since all that matters for the issuer is the ability to maintain interest rate payments; there is no presumption of future repayment. Second, creditors – that is, holders of the Consols who receive the regular interest payments – may trade that asset on financial markets. Since the plethora of different debt assets were now condensed into a single, credible, identical and easily-identified asset, the market for 3% Consols in London developed into a very large and liquid market. With such ease of access and predictable and stable payoffs, the Consols became the instrument of saving for well-off families in Austen’s time.

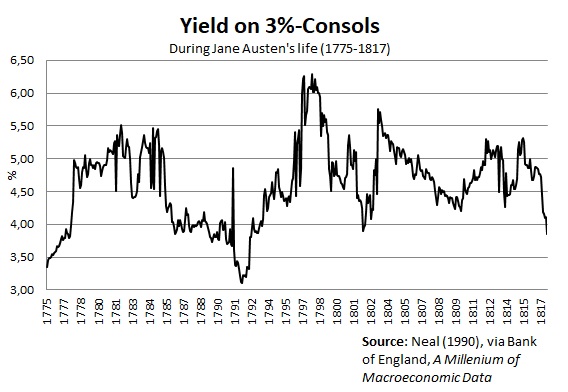

A note on yields

The Consols, essentially a piece of paper with a face value of £100, entitled the owner to a perpetual stream of payments by the government, in this case 3% – or £3. Now, the actual price at which this paper could be sold in London fluctuated extensively depending on the conditions of the financial market and, most prominently in Austen’s lifetime, the Napoleonic wars. As the £3 annual pay was serviced by the British government, and financial strain during the war increased the risk for defaults (through a foreign invasion or British government itself), the price of Consols was chiefly reflecting the military success.

When the market price of a debt falls below its face value, the effective interest rate (the “yield”) that a prospective investor receives increases; paying £50 for a Consol with face value of £100 and a £3 perpetual interest payment, effectively earns the investor 6% interest instead of 3% (3/50 = 0.06). Since the Consols were the most dominant asset on the largest financial market in the world, their price became “the single most important asset price in the world economy” as Klovland (1994: 165) called it. Here’s the yield on Consols during Austen’s life:

It reached a low of 3.11% in 1792 (almost at par), and a high of 6.22% in 1798 (below £50) after the suspension of the gold standard.

The Bennets and the fortunes of handsome young men

The families of Pride & Prejudice made good use of this thriving financial market – not specifically for trading but for financial planning (others, such as British economist David Ricardo, and the banking families of Rothschild and Barings, made some of their fortune trading Consols).

In the novel, Mr. Bennet – the protagonist Lizzy’s father – has an income of £2,000 a year (again, see my 2016 piece for three different attempts at “translating” these sums into today’s money). It is not clear what his income comes from, but it’s a fair guess that it stems, like many other landed gentry of the time, from renting out farm lands belonging to the family home Longbourne. In addition, we know that Mrs. Bennet’s portion to the family home is a £5,000 contribution which is the sole inheritance the (five) Bennet daughters are entitled to.

Now, the way well-off families like the Bennets would make use of Consols was to ensure that non-inheriting children had at least some source of income after the passing of their father. The underlying concern in Pride & Prejudice, causing Mrs. Bennet to worry so about fortunate marriages for her daughters, is that the Bennet estate is entailed away to Mr. Collins – and with it the presumed rental income of £2,000 a year. That would leave the girls homeless, reduced to living off Mrs. Bennet’s inheritance of £5,000.

Austen began writing First Impressions (the initial title for Pride & Prejudice) in October 1796. During the decade leading up to this, the yield on Consols had been firmly within the interval 3.5-4.5%, hovering around 4% for years. It should thus not surprise us that Mrs. Bennet’s fortune of £5,000 presumably consisting of Consols, would have been purchased at around £75, predictably yielding the family an annual return of 4%. Indeed, the characters of Pride & Prejudice seem to be squarely set on 4% being the general norm. For instance, in a desperate attempt to enhance his already-inane proposal to Lizzy, Mr. Collins explicitly says:

“To fortune I am perfectly indifferent, and shall make no demand of that nature on your father, since I am well aware that it could not be complied with; and that one thousand pounds in the 4 per cents, which will not be yours till after your mother’s decease, is all that you may ever be entitled to.”

(Chapter 19, p. 133 in the 2009 HarperCollins edition)

Here we see the great use that Consols offered families like the Bennets. Once the Bennet parents pass away, the £5,000 of Consols could be divided equally among her children; Lizzy’s share would be a thousand pounds, which earns her an annual 4% interest return, or £40 (although maybe several year’s earnings for a regular worker, this was a rather small sum for such rich families – in contemplating Lizzy’s sister Lydia’s imprudent marriage, we learn that Mr. Bennet spent almost £100/year on Lydia’s purchases and pocket money alone). Being liquid financial assets, dividing up the Consols among children was very easy, and their steady income stream ensured that they would have at least some income. Bar Napoleonic conquest, the interest payment on the Consols would reliably show up year after year.

As for the handsome young men, Mr. Bingley’s case is easier than Mr. Darcy’s. We know that Bingley’s income is not agricultural, but investments from a fortune of almost £100,000 inherited from his father, who had not yet acquired an estate. The fortune was “acquired by trade”, where (being from the North) cotton or shipping are prime candidates, but the slave trade is also a possibility. We also know that the ambiguity of his annual income (£4,000 or £5,000) lies well within the return from a fortune of that size invested in Consols. Indeed, for Bingley to hold that kind of fortune, earn that income and still not have an estate of his own, suggests that his financial wealth consists predominantly of Consols – perhaps complemented with some other stock (Bank of England or East India Company stock are plausible candidates). Clearly, new money.

Mr. Darcy, on the other hand, is plainly old money. And a lot of it. There are subtle hints in the novel that Pemberley has been in the Darcy family for generations. What we don’t know is precisely how his £10,000 a year is earned. When visiting Pemberley in Derbyshire with her aunt and uncle, Lizzy is told by the housekeeper that Mr. Darcy is such a generous and fair man: “ask any of his tenants”, she says, which indicates that Mr. Darcy, has a fair number of them – as one would expect from a sizeable estate like Pemberley. Now, what we don’t know is if the entirety of his £10,000 a year is reaped from rental income; it could be that some of his income is financial – or that either his financial or rental income is excluded from this rumoured number. Beyond a mention of his sister, Georgiana’s, fortune of £30,000 – which for convenience would likely be held in Consols – we know very little about the personal finances of Mr. Darcy.

The use and abuse of Consols

The financial market for government debt in the late-18th and early 19th century was not created with financial planning in mind, but by incremental improvements to previous government funding problems. The outcome, however, was a striking success for Britain, whose thriving financial market in no small part accounted for Britannia’s Century until WWI.

Moreover, as contemporary economists from Ricardo and John Stuart Mill to Malthus and Lauderdale observed, the recurring interest payments, funded by taxes, may have had quite large macroeconomic consequences. Taxing ‘productive’ investments and trade in order to fund ‘unproductive’ holders of government debt was, it was argued, harmful to the country – and in a time where government expenditures largely consisted of the military and debt maintenance, the impacts of funding the debt was of prime political interest.

Piketty’s use of Austen’s England (and Balzac’s France) was used for precisely the same distinction. Wealth, in Piketty’s view, perpetuates itself, and effortlessly earns its return (never mind the work, risk and selection issues involved). By continually paying the interest on its debt, the governments of Austen’s Britain financed the leisurly lifestyles of the rich, just as the “natural” return of the modern-day rich contribute and maintain today’s inequality.

The Consol was a revolutionary invention, but it is possible that it was not part of Mr. Darcy’s Ten Thousand a Year.

Nightcap

- It’s not gerrymandering if it benefits Democrats Aaron Bycoffe, FiveThirtyEight

- Just because you’re paranoid doesn’t mean they aren’t out to get you Rod Dreher, the American Conservative

- Planting trees beneath Turkish bombs in Syria Matt Broomfield, New Statesman

- In the long run we are all dead Charles Goodhart, Inference

Down All Your Markets

The US stock market had its worst ever initial trading weeks in 2016. Speculators are alarmed by the fall in the stocks of China. The economy of China has been growing more slowly, if at all. Also, most of the economies of the world are in growth recessions, a reduction in the rate of growth. The US dollar is high relative to other currencies, which reduces exports.

The government of China has yet to learn that interventions into financial markets often backfire. The Chinese chiefs have halted stock transactions when the market average falls to seven percent. They also have not allowed sales by investors who own more than five percent of a company. One problem with financial “circuit breakers” – a halt of trading – is that when stocks start to fall, speculators will panic and sell more quickly before trading halts. Restrictions on selling stocks create uncertainty when buying them. A speculator will fear being unable to sell shares later.

There is enough inherent uncertainty in markets without government adding to it. Uncertainty makes it important to let the market set the prices. Markets are a discovery process in which prices and quantities evolve through the bids of buyers and offers of sellers. When government interferes, we cannot know the price. Since the leaders of China have decided to have a market economy in goods, input factors, and financial assets, they should allow the market to do its job of setting the prices.

When I visited China three times, I saw a forest of cranes in all the cities I went to. Construction has driven the economy of China, along with exports. But, similar to real estate booms elsewhere, this construction was propelled by governmental policy. Throughout the world, cheap credit and fiscal subsidies to real estate have fueled unsustainable speculation.

Now China has much excess building capacity, and the halt in construction reduces related goods such as furniture and raw materials. The slow-down in China and sluggish growth elsewhere has resulted in a collapse of commodity prices.

The chiefs of China seek to move the country’s economy towards more domestic consumption. But they interfere with domestic spending by imposing a value-added tax of 17 percent on most goods other than real estate. The government of China probably chose to impose a VAT because the World Trade Organization allows the VAT to be subtracted from the price of exports, unlike an income tax. But Chinese consumers suffer a higher cost of living.

The Chinese leaders could have instead enacted LVT, land-value taxation, which would not add to the cost of goods. A tax on land value reduces the purchase price but not the land rent, so also not the price of goods. A tax on most of the rent or land value would stop the land speculation that has made a few people rich at the expense of the public.

The government of China still maintains tight control over the banking system. All the markets – real estate, financial, goods – would be more efficient if interest rates too were set by the market supply and demand for loanable funds. Of course the central banks of Europe, Japan, and the USA also are not letting their markets set the money supply and interest rates. But common practice does not imply optimal policy.

I don’t think the big drop in stock market averages imply impending economic doom. For 200 years, the US economy has had a real estate cycle of an average duration of 18 years. The current cycle began with the depression of 2008. The recovery has been slow, but the expansion has continued as employment and output have grown. Real estate construction has contributed to the expansion, and land values have recovered. The economy seldom has a recession while interest rates and commodity prices are low.

The economy of China has some severe long-run problems, but its economy is still developing and catching up. The government seems ready to let the currency trade more freely, and the coming acceptance of the currency (the yuan or renminbi) into the “special drawing rights” of the International Monetary Fund will boost the economy.

In the short run, the US stock market could fall some more, as markets often overreach, but over the next few years, financial markets will be consistent with the economic reality of restored world-wide economic growth, if there are no major destructive attacks. What we should be worried about is the unsustainability of debt and the next real estate speculative boom. The next economic disaster is about a decade into the future, and nobody is yet alarmed about that.

Cognitive Blocks and Libertarianism

Last year Brian Gothberg, who was lecturing at a summer seminar I attended in 2009, left the following comment in response to a post about media coverage and Austrian economics:

I think there’s a perceptual or cognitive block, that simply makes it hard for many people to see government activity in the foreground of the story, as an actor which actively and (often) arbitrarily changes outcomes. It reminds of the recent Brian Greene programs on cosmology on PBS. In one, he compares the treatment of space, through most of scientific history, as simply being the unadorned theater stage, upon which the truly interesting things actually happen. It’s only later that Einstein (using Riemann’s math) described space as having positive, unambiguous characteristics. After Einstein brought space itself into the foreground, you could make statements about particular things that space did do, and other particular things that space did not do.

Another example: at a gathering of friends with children, my wife and I were observing a small boy (3-ish) who kept biting the other children. When it came to tears, parents would come in and intervene, and scold him. Later, we watched the same parents — who were baffled at the boy’s biting — laugh and giggle as the father playfully bit his son. Apparently, nobody had ever brought the father’s behavior into the foreground, for their scrutiny, as a possible influence on the son’s problem. Sometimes, the obvious does stare people in the face. I think that the way we describe the role and actions of government, in the press and schools, goes a long way to explain this cognitive block. Libertarianism is nothing like common sense; not nearly.

I was reminded of this as I read the following 2008 piece by Roger Lowenstein in the New York Times, where he documents the regulatory regime that was built by the state in the years leading up to the Great Recession. Check this out: Continue reading

Around the Web: Nobel Prize Edition

I just got three of them.

- Why we need to separate the central bank from the monetary authority.

- “Market Design”

- Noble Matching.

Maybe one of our in-house economists can share their thoughts on the award this year as well…