- Foucault, Max Weber, and Hayek Eric Schliesser, Digressions & Impressions

- It’s been a bad week in America Andrew J Cohen, Prosocial Libertarians

- Summer 2008 redux? David Glasner, Uneasy Money

- Meanwhile, in Iraq…

central banking

Some Monday Links: Mostly Econ, again

The worldly turn (Aeon)

The chocolate route (Aeon)

For the Woke warriors, culture and economics are two sides of the same coin – just ask Mollie-Mae (CapX)

Optional.: Knowing who Mollie-Mae actually is.

Measuring the Essence of the Good Life (Finance & Development)

Nightcap: Development with Dignity (NOL)

Great Stories and Weak Economics (Regulation)

Digital currencies and the soul of money (BIS)

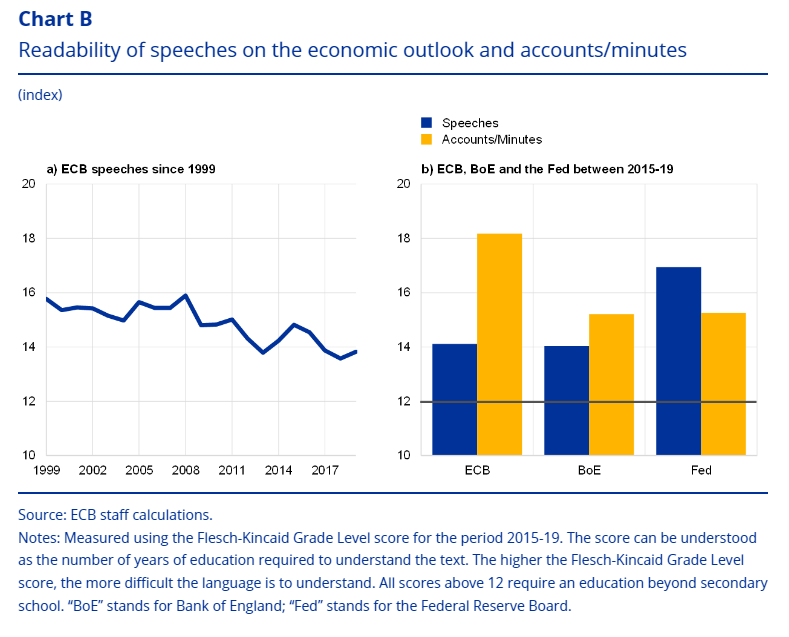

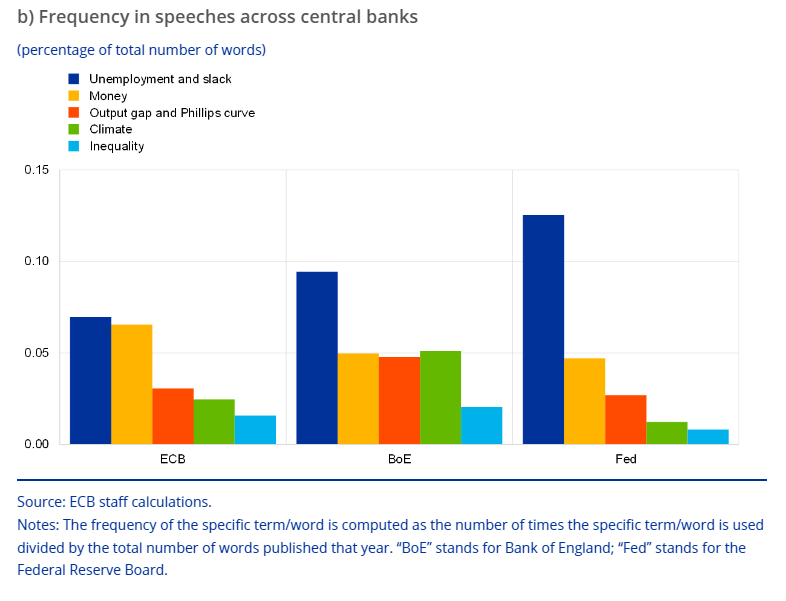

To close this, a couple of neat graphs from the European Central Bank. The first one shows a measure of central bank messages’ clarity , the lower the number, the better. The second graph demonstrates the frequency (a proxy for significance) of some buzzwords. As old Korean masters comment when comparing various strands of their art, the major central banks are “same, same, a little different“.

Nightcap

- How the Afghanistan War really started Robert Wright, Nonzero

- The Fed’s exit strategy (in 2009) Robert Aro, Power & Market

- Austrian Economics for the lower classes Weiss & Nelson, L&L

- On liberalism’s peaceful global order Eric Schliesser, D&I

Monday’s Reserved Judgements (and Satisficing Hopes)

Or, some Monday links on central banks, manners over matters and hard-boiled decisions

That bond salesman from the Jazz Age was right. Reserving judgement, at least sometimes, allows for a fairer outcome. Take for example the Brick film (2005), a neo-noir detective story set in a modern Southern California high school. Here in Greece it made some ripples, then it was forsaken for good. Not sure about its status in the US or elsewhere, but “overlooked”/ “underrated” seem to go with it in web searches. I agree now, but when I first watched it, its brilliance was lost to me ( and no, it was not allegedly “ahead of its time”, as some lame progressive metal bands of late 90s hilariously asserted when they zeroed in sales…).

The film’s peculiarity was obvious from the titles. A couple of gals left the theater like 10’ in. My company and I were baffled for most part, by the gritty atmosphere. And I have not even begun with the dialogue. The language was something from off the map. As late Roger Ebert noted:

These are contemporary characters who say things like, “I got all five senses and I slept last night. That puts me six up on the lot of you.” Or, “Act smarter than you look, and drop it.”

You see, the whole thing was intended to serve tropes, archetypes and mannerisms from the hard-boiled fiction of 1920s-30s. A manly man vs crime and (corrupted) government, and so on and so forth. We went there, un-f-believably how, clueless about all these. We did, however, make a recurring joke from the following lines:

Brendan: You and Em were tight for a bit. Who’s she eating with now?

Kara: Eating with?

Brendan: Eating with. Lunch. Who.

Seen in this light, everything made sense to my gusto. Anyway, seems that reserving judgements not only does better assessments, but also protects the lazy unaware.

Now, I have previously indicated that I have a soft spot for the “technology of collective decisions” that are central banks. I usually reserve my judgements on them, too. This comment summarises recent developments, including a few interesting links:

In which the Rich Get Richer (Economic Principals)

A new paper by Carola Binder examines central bank independence vis-à-vis a technocratic – populist merge in the age of digital media:

Technopopulism and Central Banks (Alt – M)

The author argues that central banks, supposedly the bastions of technocratic approach, tend to “respond” (i.e. be nudged by and directly appeal) to a perceived “will of the people”, as it is expressed on-line or via events like the “FED Listens” series. This bend acts as a claim to legitimacy and accountability, in exchange of trust and extended discretion, leading to a self-reinforcing circle almost beyond the democratic election process. In other words, not quite the “Bastilles” contra “modern Jacobinism” (to remember how Wilhelm Röpke deemed independent central banks in 1960). A way out could be made, concludes the author, by introducing of a rule-based monetary policy.

Central banks, as institutional arrangements developed mostly during the 20th century, share a common mojo and tempo with the FED. They gradually assumed more independence, and since the emergence of modern financial markets, (even more) power. This rise has been accompanied by increasing obligations in transparency and accountability, fulfilled through an ever-expanding volume of communication in terms of hearings, testimonies, minutes, speeches etc. This communication also plays a role in shaping economic actors’ expectations, a major insight that transformed our understanding of macroeconomic outcomes. Andy Haldane talks all these, along with other delicious bits, in an excellent speech from 2017 (his speeches have generally been quite something):

A Little More Conversation A Little Less Action (Bank of England)

Plot twist: The endeavor of more communication has a so-so record in clarity, as documented by the rising number of “education years” needed to follow and understand central banks’ messages. The same trend goes for the pylons of rule of law, the supreme courts, at least in Europe. We certainly have come a long way since that time at the 70s, when a former Greek central bank Governor likened monetary decisions to a Talmudic text, ok, but we are not there yet.

As a parting shot, let us return just over a year back, when the German Federal Constitutional Court delivered a not exactly reserved decision (5 May 2020) about the European Central Bank’s main QE program. The FCC managed to:

- scold the top EU Court for flawed reasoning and overreach in confirming the legality of the program in Dec 2018 (the FCC had stayed proceedings and referred the case to the Court of Justice of the EU, for a preliminary ruling in Jul 2017. Europe’s top courts are not members of the Swift Justice League, apparently).

- indirectly demand justifications from ECB, which is beyond its jurisdiction as an independent organ of EU law, by

- warning the German public bodies that implement ECB acts to observe their constitutional duties, while

- effectively not disrupting the central bank’s policy.

The judicial b-slapping provoked much outcry and theorising, but little more, at least saliently. The matter was settled by some good-willed, face-saving gestures from all institutions involved, while it probably gave a push to the Franco-German axis, to finally proceed in complementing monetary policy measures with the EU equivalent of a generous fiscal package. The rift between the EU and the German (in this case, but others could follow) respective legal orders may never be undone, though. If anyone feels like delving deeper into the EU constellation, here is a fresh long slog:

Constitutional pluralism and loyal opposition (ICON Journal)

I don’t. But then again, maybe I will act smarter than I look.

Monetary Tales from the Farthest Shore

The second bank by the sea

My music playlist has nearly stagnated for years and, depending on your age, maybe yours has too. Evidence suggests that (partly) because of mind shenanigans, our musical palette does not quite expand past the age of 30. I think that something similar goes for gaming. I am still fond of those (pc) games from my late teen – early adult years and stay happily ignorant about the newer ones. Those single player games immersed you through substance over eye-candies. Some in-game scenes remain pure gold after all these years. Like that dialogue, when one of my younger siblings was delving in a fictional setting resembling the Caribbean during the Golden Age of Piracy. (Escape from Monkey Island. I preferred RPGs. Nowadays, only books – like this one.)

At some point, the protagonist, a witty swashbuckler, visited the Second Bank of an island called Lucre. “What happened to the First Bank of Lucre?”, he inquired. “Nothing”, said the bank teller, “It was our public relations department’s idea. They felt that being called the ‘First’ bank didn’t project an image of experience”. At the time I thought it as just a funny anachronism. Later, I recognized a jab to brand marketing practices and the corporate-speak more generally. But it was also the scheme of a “fledgling” first banking institution versus a “trustworthy” second one that almost held a real-world analogy.

Some kind of a theory

There is a rich discussion on the origins of money, its form and the proper control of it, as well as a few historical cases of either state or private currencies thriving – or failing. Hard. In the thick of it, we talk about two positions. From the one hand, the “economics textbook” approach proposes that money emerged in the realm of private economic relations, to minimize transaction costs and facilitate trade. (Francisco d’Anconia would approve.) Here be a decentralized, bottom-up acceptance of the medium of exchange. This view sits well with the classical liberal dichotomy between the civil and state spheres, which can be expanded to envision a very limited role for the state in monetary affairs. From the other hand, the “anthropological – historical” position articulates that trust on money comes mostly from the sovereign’s guarantee, marked by the sign of God and/ or Emperor. This top-down explanation is more receptive to the state control of money, rhyming with the monetary power as a prerogative of the ruler and an expression of sovereignty.

Beginning with some important judicial decisions in the second half of 19th century, the official assertion of state power over money came in the 20th century. Per the Permanent Court of International Justice, in 1929, “it is indeed a generally accepted principle that a state is entitled to regulate its own currency”. You know, the norm of modern national monetary monopolies. There was a time though, when things were more colorful and less unambiguous. From the 13th century onward to the Golden Age of Piracy and beyond, it was only normal for different monies of various issuers to flow from one territory to the other. Reputable currencies required not only a resilient authority backing them, but also a nod by society and custom. This kind-of-synthesis of the two positions outlined above rung especially true in the case of the young Greek state in 1830s – 1840s. (For this section I draw from the comprehensive “History of the Greek State 1830 – 1920”, by George B. Dertilis [the 2017 Crete University Press edition, in Greek. An extended version, under a different title, is forthcoming in English in 2021/22]. Btw, on Mar. 25 we celebrate 200 years from the Declaration of the Greek Revolution versus the Ottoman rule, an [underrated?] event with connotations of nationalism and liberal constitutionalism.)

Over there at the (Balkan) shore

As the new state needed to break free from all the institutions of Ottoman Empire, its hastily assembled first Bank of Issue sought to introduce a new national currency (the Phoenix). The impoverished, ravaged and cut off from international debt markets nascent state reflected bad upon the Bank. The government tried to force public’s trust via legislation. By decree, payments from/ to the state coffers would include a mandatory percentage of the new banknotes (later the percentage was set at 100%). Revenue from state natural resources – present and future – would back the currency. The administrative magic did not do it. The public actively tried to avoid the Phoenix banknotes, in favor of traditional silver/ gold coins. Bank and currency failed to crowd out the foreign monies and ultimately went out of business. A few years later, the overall environment had improved somewhat and a more vigorous state established the second Bank of Issue. Another new national currency, the Drachma, was already circulating in – copper – coins along with the foreign ones.

The second Bank received an exclusive charter of issue and undertook the task to roll-out the Drachma banknotes (silver/ gold coins would follow) and, in doing so, integrate the fragmented Greek countryside to a more cohesive national economy. Up until then, the local markets had operated as loosely hierarchical oligopolies. At the bottom of the chain, each small village or group of villages was dependent on a merchant-money lender who held monopsonistic power over the (tiny scale) agricultural production and, at the same time, monopolistic power in cash and credit. These rural businessmen depended on the respective merchant-money lender of the nearest town for brokerage. Next in line was the merchant-money lender of the nearest city, usually with access to international trade routes. You get the picture. These informal networks contained competition among neighboring lesser merchant-money lenders and promoted trade through a complex web of transactions (involving forward contracts, insurance premiums and bills of exchange, among others). (The official site for the anniversary features a fancy piece about the first attempts to establish a national bank as well. It includes a few names and dates, while noticing the “exploitative” networks and the “primitive” credit system .I find its lack of nuance disturbing somewhat misleading.)

Becoming one with the forces

The Bank opted to tap and complement the existing disjointed market forces, in order to gently nudge them. It channeled its primary tool, lending in banknotes, to the local money markets, firstly, to a limited number of large merchant-money lenders, later to the middle ones. (According to the Bank’s ledgers, these clients usually chose respectable job titles, such as “Banker” or “Broker”. Others, a bit blunter, went by the Greek equivalent of “Usurer”.) This lending – apart from being short-term, relatively safe and profitable – enabled the Bank to gradually assume a leading position, without the need to deep dive at the specifics of each end-user of the market. The soft, indirect entry in the century-old customary networks lowered the cost of money and contributed to the integration of the national economy. The transition was not always smooth, with the occasional episode (people switching from banknotes to metallic coins, the Bank returning the favor by aggressively cutting back lending, the government setting compulsory percentages etc – you know the drill), but still, the stakeholders’ incentives aligned. Society at large recognized Bank and currency, with the system reaching a workable equilibrium

The merchant-money lender of old was finally phased-out by regular bank lending in the next decades. Further underpinned by a cozy relationship with the state (always a valuable client, usually a partner, sometimes even an opponent), the Bank acted as a quasi-central banking institution until 1928, when the charter was transferred to the newly found Bank of Greece. The Drachma continued as official legal tender (albeit with numerous conversions) until the end of 2001.

Elective Affinities in Institutional Design, 1951

[Note: this is a piece by Michalis Trepas, who you might recognize from the now-defunct NOL experiment “Be Our Guest.” Michalis is a newly-minted Notewriter, and this is the first of many more such pieces to come. -BC]

The Treasury and the Federal Reserve System have reached full accord with respect to debt-management and monetary policies to be pursued in furthering their common purpose to assure the successful financing of the Government’s requirements and, at the same time, to minimize monetization of the public debt.

– Joint announcement by the Secretary of the Treasury and the Chairman of the Board of Governors, and of the Federal Open Market Committee, of the Federal Reserve System, issued for release on Mar. 4, 1951

The Allied High Commission appreciates that these responsibilities [for the central bank] could not, without serious inconvenience, be given up so long as no legislation has been enacted establishing a competent Federal authority to assume them.

– Letter from the Allied High Commission to Chancellor Adenauer, Dated Mar. 6, 1951

A Financial Fable by Carl Barks, a short story starring Donald Duck and his duck-relatives, was published in Mar. 1951. It featured concepts like supply/ demand, money shocks, inflation and the ethics of productive labor, from a rather neoclassical perspective. Read today, it seems out of synch with the postwar paradigm of a subordinated monetary policy to the activist state and, more generally, with what came to be known as the Golden Age. As you have already probably noticed, this March also marks the 70th anniversary of two more instances against the currents of the time. It was back then that two main traditions of central bank independence – based on political consensus and judicial (“Chevron”) deference in the case of US, based on written law and judicial review in the case of Eurozone (read: Germany) – were (re)rooted. In the following lines, I offer an outline focused on institutional interplay, instead of then usual dramatis personae.

The first instance is the well-known Treasury – FED Accord. Its importance warrants a mention in nearly every institutional discussion of modern central bank independence. The FED implemented an interest rates peg – kind of capping the yield curve – in 1942, to accommodate public debt management during World War II. The details were complicated, but we can still think of it as a convenient arrangement for the Executive. The policy continued into the early 50s, with the inflationary backdrop of the Korean War leading to tensions between a demanding Executive and an increasingly resistant central bank. Shortly after the dispute became more pronounced, reaching the media, the two institutions achieved a compromise. The austere paragraph cited above ended the interest rates peg and prompted a shift of thinking within – and without – the central bank, on monetary policy and its independence of fiscal needs.

The second one is definitely more obscure, and as such deserves a little more detail. The Bank deutscher Länder (BdL) was established in 1948, in the Allied territory of occupied Germany. It integrated central banking institutions, old and new, in a decentralized fashion á la US FED. Its creation underpinned the – generally successful – double reform of that year (a currency conversion with a simultaneous abolition of price controls), which reignited free market forces (and also initiated the de facto separation of the country). The Allied Banking Commission (ABC) supervised the BdL and retained the sole right to issue direct instructions, a choice more practical than doctrinal or ideological. As the ABC gradually allowed a greater leeway to the central bank, while fending off even indirect German political interventions, the resulting institutional setting provided for a relatively independent BdL.

In late 1950, the Occupational Authority wanted out and an orderly transfer of powers required legislation from the Federal Government. Things deadlocked around the draft of the central bank law, the degrees of centralization and independence being the thorniest issues. The letter cited above, arriving after a few months of inertia, was the catalyst for action. The renewed negotiations concluded with the “Interim Law” of 10 Aug. 1951. The reformed BdL was made independent of instructions from the Federal Government, while at the same time assuming an obligation to support government’s general economic policy – without prejudice to its monetary duties.

This institutional arrangement was akin to what the BdL itself had pushed for, a de jure formalization of its already de facto status. Keep in mind that the central bank enjoyed a head start in terms of reputation and experience versus the Federal Government, after all. But it can also be traced to the position articulated by the free market-oriented majority in the German quasi-governmental bodies back in 1948, a unique blend of explicit independence from/ cooperation with the government. The 1951 law effectively set the blueprint for the final central bank law, the Bundesbank Act of 1957. The underlying liberal creed echoed in the written report of the Chairman of the Committee for Money and Credit of the parliament:

The security of the currency… is the highest precondition for the retention of a market economy, and hence in the final analysis that of a free constitution for society and the state… [T]he note-issuing bank must be independent of these [political bodies] and subject only to the law.

The Financial Fable was the only story featuring Disney’s characters that made it to an important history of comics book, published in 1971. Around that time, the postwar consensus on macroeconomic stabilization policy was reaching its peak. A rethinking was already underway on the tools and goals of monetary policy, taking it away from the still garbled understanding of the period. It took another decade or so for both sides of the Atlantic to recalibrate their respective monetary policies. The accompanying modern central bank independence, with its foundations set in 1951, became a more salient – and popular – aspect a bit later.

Nightcap

- The challenges of lending to Main Street George Selgin, Alt-M

- What Sweden has done right on Coronavirus Joakim Book, AEIR

- The State Has Seized Many New Powers. It Won’t Let Go of Them Easily. Andrei Znamenski, Mises Wire

- When disease comes, rulers grab power Anne Applebaum, Atlantic

Nightcap

- Bernie, Cuba, literary, and ill-gotten gains Irfan Khawaja, Policy of Truth

- The weird global coronavirus data Scott Sumner, EconLog

- Why the Fed shouldn’t “Do Nothing” George Selgin, Alt-M

- Corporatism (“anarchy”) on the Indian subcontinent Priya Satia, LARB

Nightcap

- Goodbye, Neal Peart Suleman Khawaja, Policy of Truth

- Great economics, bad politics (Banerjee & Duflo) Chris Dillow, Stumbling & Mumbling

- The Golden Age of the Federal Reserve is here Scott Sumner, MoneyIllusion

- Randolph Borne and the Progressives Nikhil Pal Singh, New Statesman

Be Our Guest: “The U.S. Economy: A Fading Illusion?”

This essay, by longtime NOL reader and CPA Jack Curtis, is the first essay of 2020’s “Be Our Guest” feature. Here is a snippet:

This widespread financial vulnerability seems a natural result of government policies that minimize interest rates and support monetary inflation as the Federal Reserve and other central banks have continued to do in recent decades. There is little incentive to save money when it offers no significant return and its value is inflated away. Governments that cling to such policies are imposing dependence upon their citizens, forcing them in essence to live hand to mouth, deprived of the ability to provide for their own futures.

Jack paints a pretty gloom picture of the U.S. economy. Does this square with what economists have been telling us about the state of the world? Please, read the whole essay, and if you have been thinking about writing for the public in 2020, give us a holler. We’d be happy to put your thoughts up for the whole world to read.

Nightcap

- Who betrayed Syria’s Kurds? Amberin Zaman, Al-Monitor

- How the Physiocrats confronted France’s empire (Smithian-Misesian-Hayekian federation) Pernille Røge, Age of Revolutions

- Strange respect for central banks Scott Sumner, MoneyIllusion

- This is just the beginning of Brexit Tom McTague, the Atlantic

Nightcap

- Indigenous actors and International Relations Andrew Szarejko, Duck of Minerva

- You’re all a bunch of socialists Bryan Caplan, EconLog

- Doubting disaster capitalism Chris Dillow, Stumbling & Mumbling

- Inside America’s worst financial crisis Amanda Griffiths, Alt-M

Nightcap

- The threat of fanaticism Chris Dillow, Stumbling & Mumbling

- On targeting the price of gold George Selgin, Alt-M

- Reinventing language Catherine Charrett, Disorder of Things

- Geopolitics and Greenland Jon Rahbek-Clemmensen, War on the Rocks

Nightcap

- From Lahore to Lancashire: Untold stories from imperial Britain John Keay, Literary Review

- The younger sons in Jane Austen’s England had to work Richard Francis, Spectator

- How soon we forget Scott Sumner, EconLog

- Gin, sex, malaria, and American anthropology Charles King, Chronicle Review