- How to flip a yield curve George Selgin, Alt-M

- How ergodicity reimagines economics Mark Buchanan, Aeon

- How to think better about debt Lou Brown, Crooked Timber

- Why even have kids in today’s world? Bryan Caplan, EconLog

debt

Nightcap

- American debt (to immigrants) Gaiutra Bahadur, New Republic

- Why immigrants are superior Jacques Delacroix, NOL

- Misadventures of an anthropologist in Indonesia Tim Hannigan, Asian Review of Books

- Why books don’t work Andy Matuschak

Two Financial Instruments that made the Modern World

Following my Mr. Darcy piece that outlined the use and convenience of British government debt instruments in the eighteenth (and predominantly the nineteenth) century, I thought to extend the discussion to two particular financial instruments. In addition to the Consols (homogenous, tradeable perpetual government debt) that formed the center of public finance – and whose active secondary market that made them so popular as savings devices – the Bill of Exchange was the prime instrument used by merchants for financing trade and settling debts.

The complementarity of the Consol and the Bill in international finance, roughly from the South Sea Bubble (1720) to the end of Napoleon (1815), was the “secret of success for international finance” (Neal 2015: 101) and arose without an overarching plan, i.e. rather spontaneously. As the Consol is more easily understood for a modern reader, and the Bill is both more ancient and less well understood, I’ll focus the bulk of my attention on the latter.

According to Anderson (1970: 90), the Bill constituted “a decisive turning-point in the development of the English credit system,” but is much older than that. In practice, it was a paper indicating debt and a time for repayment, allowing financing of current trade. Cameron (1967:19) writes that the Bill

was far more ancient than either the banknote or the demand deposit; it had been developed in the Middle Ages. At first the bill was used as a device for avoiding the cost and risks of shipping coin or bullion over great distances, then as a credit instrument which circumvented the Church’s prohibition of usury. When it first came to be used as a means of current payment is a moot question that may never be answered, but that it was so used in eighteenth-century England is beyond doubt.

The Bill was predominantly used in coastal cities in the Mediterranean and around the North-Sea, becoming frequent perhaps in the 1700s. One observer even dates an early instance of its use to 1161, and it was of standard use among traveling traders, merchants and brokers throughout the Middle Ages (Cassis & Cottrell 2015: 12). Occasionally – warranting a discussion of its own – Bills in England became “so widespread that they drove out even banknotes” (Cameron 1967: 19).

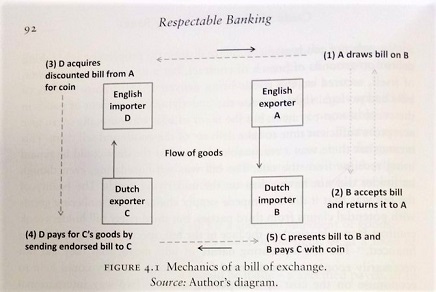

There is an unfitting competition among financial historians as to who can produce the most persuasive, informative or complicated schedule for how Bills worked (I know of at least four similar, yet uncredited, renditions). Here’s Anthony Hotson’s (2017: 92) attempt from last year:

- We start, counter-intuitively, in the top-right corner. Andrew, an English exporter of Apples, draws up a Bill on Bas, a Amsterdam maker of Bankets – a Dutch pastry. Bas, having no coin/gold available to pay Andrew – either because he won’t have the funds until after he has sold his apple-flavored(!) Bankets, or because the risk of loss or cost of transportation is too great – accepts the Bill and returns it to Andrew.

- Having returned it to Andrew, we now have a debt and a financial instrument; Bas has promised to pay Andrew £x for the apples in 90 days, a common duration for a Bill of exchange.

- But like most merchants, Andrew cannot wait 90 days for payment; he has sold and shipped his Apples, but needs funds for himself (feeding his family, or investing in new Apple-harvesting equipment etc). In the heyday of British financial markets, Andrew could simply visit a bank, Bill-broker or the London financial markets himself, and offer to sell the Bill there. Of course, Andrew won’t be able to sell the Bill for £x, since his buyer is effectively providing him with a loan for 90 days. The bank, bill-broker or financial market trader will discount the Bill with the going interest rate (say 6%, for one-quarter of a year, so ~1.5%), paying at most £0.985x for the Bill. Besides, there is a risk-of-default element involved, so the buyer applies a risk premium as well, perhaps buying the Bill at £0.95x.

- In the schedule above Hotson uses the Bill trade to show how merchants trading Bills could net out their respective debts and minimize the need to send payment across the British channel. For (3) and (4), then, we replace the banker with an English importer – Dave – of Dutch goods (perhaps tin-glazed pottery) looking for a way to pay his Amsterdam pottery supplier, Cremer. Instead of shipping gold to Amsterdam, Dave may purchase Andrew’s Bill, and settle his account with Cremer by sending along the Bill drawn on Bas. Once the 90 days are up, Cremer can simply wander over to Bas’ pastry shop and present him with the Bill to receive payment for the goods Cremer already shipped to England.

This venture can – and usually was – made infinitely more complicated; we can add brokers and discounting banks in every transaction between Andrew, Bas, Dave and Cremer, as well as a number of endorsers and re-discounters. In his popular book Exorbitant Privilege, Barry Eichengreen recounts a 12-step, several-pages long account for how a U.S. importer of coffee and his Brazilian supplier both get credit and signed papers from their local (New York + Brazil) banks, how both banks send their endorsed bills to their London correspondent banks, and some investor in the London money markets purchase (and perhaps re-sell) the Bill that eventually settles the transaction between the American coffee importer and the Brazilian farmer.

Although it might sound excessive, complicated and impossible to overlook, the entire process simplified business for everyone involved – and allowed business that otherwise couldn’t have been done. In econo-speak, the Bill of Exchange set within a globalizing financial system, extended the market for merchants and farmers and customers alike, lowered transaction costs and solved information asymmetries so that trade could take place.

Turning to the opposite end of the maturity spectrum, the Consol as a perpetual debt by the government was never intended to be repaid. Having a large secondary market of identical instruments, allowed investors or financial traders everywhere to pass Gorton’s No-Questions-Asked criteria for trade. A larger market for government debt, such as after Britain’s wars in the late-1700s and early 1800s, allowed dealers in financial markets to a) be reasonably certain that they could instantly re-sell the instrument when in need of cash, and b) quickly and effortlessly identify it. These aspects contributed to traders applying a smaller risk premium to the instrument and to be much more willing to hold it.

While the Bills were the opposite of Consols in terms of homogeniety (they all consisted of different originators, traders, and commodities), there developed specialized dealers known as Discount Houses whose task it was to assess, buy, and sell Bills available (Battilosso 2016: 223). Essentially, they became the credit rating institutions of the early modern age.

Together these two instruments, the Bills of Exchange and the Consols, laid the foundations for the modern financial capitalism that develops out of the Amsterdam-London nexus of international finance.

Poverty Under Democratic Socialism — Part I: the French Case

I saw a televised investigation by the pretty good French TV show, “Envoyé spécial” about current French poverty. It brought the viewer into the lives of six people. They included a retired married couple. The four others were of various ages. They lived in different parts of mainland France. All sounded French born to me. (I have a good ear for accents; trust me.) All were well spoken. The participants had been chosen to illustrate a sort of middle-class poverty, maybe. Or, perhaps to illustrate the commonness of poverty in one of the first countries to industrialize.

All the interviewees looked good. They seemed healthy. None was emaciated; none was grossly obese, as the ill-fed everywhere often are. All were well dressed, by my admittedly low standards. (I live in the People’s Democratic Republic of Santa Cruz, CA where looking dapper is counter-revolutionary.) None of those featured was in rags or wearing clothes inappropriate for the season.

The reporter took the viewer into these people’s homes. There was no indoor tour but you could see that the outside of the houses was in good repair. Most of the interviewing took place in kitchens. Every kitchen seemed equipped like mine, more than adequately. There was a range and a refrigerator in each. Every house had at least one television set.(I couldn’t determine of what quality.) No one said he or she was cold in the winter though two complained about their heating bills.

The show was geared to sob stories and it got them. Each participant expressed his or her frustration about lacking “money,” precisely, specifically. It seems to me that all but two talked about money for “extras.” I am guessing, that “extras” mean all that is not absolutely necessary to live in fairly dignified comfort. One single woman in her forties mentioned that she had not had a cup of coffee in a café for a year or more. (Keep her in mind.)

Another woman talked about the difficulty of keeping her tank filled. She remarked that a car was indispensable where she lived, to go to her occasional work and to doctors’ appointments. Her small car looked fine in the video. The woman drove it easily, seemingly without anxiety or effort.

A woman of about forty, divorced, took care of her two teenage daughters at home two weeks out of each month. She explained how she went without meat for all of the two weeks that her daughters were away. She did this so she could afford to serve them meat every day that they were with her. I could not repress the spontaneous and cynical reaction that most doctors would probably approve of her diet.

Yet, another woman, single and in her thirties, displayed her monthly budget on her kitchen table. She demonstrated easily that once she had paid all her bills, she had a pathetically small amount of money left. (I think it was about $120 for one month.) She had a boyfriend, a sort of good-looking live-in help whose earnings, if any, were not mentioned.

The retired couple sticks to my mind. The man was a retired blue-collar worker. They were both alert and in good shape. Their living room was comfy. They also talked about their bills – including for heating – absorbing all of their income. The wife remarked that they had not taken a vacation in several years. She meant that she and her husband had not been able to get away on vacation, somewhere else, away from their house and from their town. They lived close to a part of France where some rich Americans dream of retiring some day, and where many Brits actually live.

I ended up a little perplexed. On the one hand, I could empathize with those people’s obvious distress. On the other hand, I got yanked back to reality toward the end when the retired lady blamed the government for the tightness of her household budget. Then I realized that others had tacitly done the same. The consensus – which the reporter did not try expressly to produce – would have been something like this: The government should do something for me (no matter who is responsible for the dire straights I am in now).

Notably, not one of the people in the report had a health care complaint, not even the senior retired couple.

So, of course, I have to ask: Why are all those people who live far from abject poverty, by conventional standards, why do all those people convey unhappiness?

The first answer is obvious to me only because I was reared in France, where I retain substantial ties: Many small French towns are dreadfully boring, always have been. That’s true, at least, if you don’t fish and hunt, or have a passion for gardening, and if you don’t attend church. (But the French are not going to church anymore; nothing has taken the social place of church.)

And then, there is the issue of what the French collectively can really afford. This question in turn is related to productivity and, separately, to taxation. I consider each in turn.

French productivity

According to the most conventional measure – value produced per hour worked – French productivity is very high, close to the German, and not far from American productivity: Something like 93% of American productivity for the French vs 95% for the Germans. (Switzerland’s is only 86%.) However, to discuss how much money is available for all French people together, we need another measure: the value of French production divided by the number of French people. Annual Gross Domestic Product per capita is close enough for my purpose. (The version I use is corrected to incorporate the fact that the buying power of a dollar is not the same in all countries: “GDP/capita, Purchasing Power Parity”).

For 2017, the French GDP/capita was $43,600, while the German was $50,200. (The American was $59,500.) Keep in mind the $6,600 difference between the French and the German GDP/capita (data).

If French workers are almost as productive as the Germans when they work, what can account for the low French GDP/capita? The answer is that the French don’t work much. Begin with the 35/hr legal work week. (1) (A study published recently in the daily Le Figaro asserts that 1/3 of the 1.1 million public servants work even less than 35 hours per week.) Consider also the universal maximum retirement age of 62 (vs 67 in Germany), a spring quarter pleasantly spiked with three-day weekends for all, a legal annual vacation of at least thirty days applied universally, a common additional (short) winter (snow) vacation. I have read (I can’t confirm the source) that the fully employed members of the French labor force work an average of 600 hours per year, one of the lowest counts in the world. Also log legal paid maternity leave. Finish with an official unemployment rate hovering around 9 to 10% for more than thirty years. All this, might account for the $6,600 per year that the Germans have and the French don’t.

There is more that is seldom mentioned. The fastest way for a country to raise the official, numerical productivity of its workers is to put out of work many of its low-productive workers. (That’s because the official figure is an arithmetic mean, an average.) This can be achieved entirely through regulations forbidding, for example, food trucks, informal seamstress services, and old-fashioned hair salons in private living rooms, and, in general, by making life less than easy for small businesses based on traditional techniques. This can be achieved entirely – and even inadvertently – from a well-meaning wish to regulate for the collective good. The more of this you do, the higher your productivity per capita appears to be and also, the higher your unemployment, and the less income is available to go around. I think the official high French productivity oddly distorts the image of real French income. I suspect it fools many French people, including public officials: They think they are wealthier than they are.

La vie est belle!

The French have nearly free health care – which works approximately as well as Medicare in the USA, well enough, anyway. (French life expectancy is higher than American expectancy.) Education is tuition-free at all levels. There are free school lunches for practically anyone who asks. University cafeterias are subsidized by the government (and pretty good by, say, English restaurant standards!) Many college students receive a stipend. Free drop-off daycare centers are common in big and in medium-size cities. Unemployment benefits can easily last for two years, three for older workers. They amount to something like 55% of the last wages earned, up to 75% for some.

That’s not all. The fact that France won the World Cup in soccer in 2018 suggests that the practice of that sport is widespread and well supported. It’s mostly government subsidized. Other sports are also well subsidized. French freeways are second to none. They are mostly turnpikes but the next network of roads down is excellent, and even the next below that. This is all kind of munificent, by American standards. The French are taken care of, almost no matter what. The central government handles nearly all of this distribution of services directly and some, indirectly through grants that local entities have to beg for.

Someone has to pay for all this generosity. After sixty or seventy years, many, perhaps most French people, still believe that the rich, the very rich, have enough money that can be pried from their clutching hands to pay for the good things they have, plus the better things they wish for. (No hard numbers here, but I would bet that ¾ of French adults believe this.) In fact, multi-fingered, ubiquitous, invasive taxation of the many who are not very rich pays for all of it.

French taxation

The French value added tax (VAT) is 20% on nearly all transactions. When a grower sells $100 of apples to a jelly producer, the bill comes to $120. When the jelly-maker in turn sells his product to a grocery wholesaler, his $200 bill goes up to $240, etc. Retail prices are correspondingly high. The French are not able to cheat all the time on the VAT although many try. (Penalties are costly on the one hand, but there exists a complicated, frustrating official scheme to get back part of the VAT you do pay, on the other hand.) I speculate that the VAT is so high because the French state does not have the political will nor the capacity to collect an effective, normal income tax, a progressive income tax. Overall, the French fiscal system is not progressive; it may be unintentionally regressive. To compensate, until the Macron administration, there was a significant tax on wealth. (That’s double taxation, of course.) It’s widely believed that rich French people are escaping to Belgium, Switzerland, and even to Russia (like the actor Gérard Dupardieu).

The excise taxes are especially high, including the tax on gasoline. In 2018, the mean price of gasoline in France was about 60% higher than the mean price in California, where gas is the most taxed in the Union. An increase to gasoline taxes, supposedly in the name of saving the environment, is what triggered the “yellow vests” rebellion in the fall of 2018. Gasoline taxes are particularly regressive in a country like France where many next-to-poor people need a car because they are relegated to small towns, far from both essential services and work. (2)

All in all, the French central government takes in about 55% of the GDP. This may be the highest percentage in the world; it’s very high by any standard. It dries up much money that would otherwise be available to free enterprise. Less obviously but perhaps more significantly, it curtails severely what people individually, especially, low income citizens, may spend freely, of their own initiative.

What’s wrong?

So, with their abundant and competent social services, with their free schooling, with their prodigal unemployment benefits, with their superb roads, with their government-supported prowess in soccer, what do the French people in the documentary really complain about? Two things, I think.

Remember the woman who couldn’t afford to take her coffee in a café? Well, the French have never been very good at clubs, associations, etc. They are also somewhat reserved about inviting others to their homes. The café is where you avail yourself of the small luxury of avoiding cooking chores with an inexpensive but tasty sandwich. It’s pretty much the only place where you can go on the spur of the moment. It’s where you may bump into friends and, into almost-friends who may eventually become friends. It’s the place where you may actually make new friends. It’s the best perch from which to glare at enemies. It’s where that woman may have a chance to overhear slightly ribald comments that will make her smile. (Not yet forbidden in France!) The café is also just about the only locale where different age groups bump into one another. The café is where you will absorb passively some of that human warmth that television has tried for fifty years but failed to dispense.

This is not a frivolous nor a trivial concern. In smaller French towns, a person who does not spend time in cafés is deprived of an implicit but yet significant part of her humanity. The cup of coffee the woman cannot afford in a café may well be the concrete, humble, quotidian expression of liberty for many in other developed countries as well. (After all, Starbucks did not succeed merely by selling overpriced beverages.) The woman in the video cannot go to cafés because the social services she enjoys and supports – on a mandatory basis – leave no financial room for free choice, even about tiny luxuries. She suffers from the consequences of a broad societal pick that no one forced on her. In general, not much was imposed on her from above that she might have readily resisted. It was all done by fairly small, cumulative democratic decisions. In the end, there is just not enough looseness in the socio-economic space she inhabits to induce happiness.

She is an existential victim of what can loosely be called “democratic socialism.” It’s “democratic” because France has all the attributes of a representative republic where the rule of law prevails. It’s “socialistic” in the vague sense in which the term is used in America today. Unfortunately, there is no French Bureau of Missing and Lost Little Joys to assess and remedy her discontent. Democratic socialism is taking care of the woman but it leaves her no elbow room, space for recreation, in the original meaning of the word: “re-creation.”

The second thing participants in the documentary complain about is a sense of abandonment by government. Few of them are old enough to remember the bad old days before the French welfare state was fully established. They have expected to be taken care of all their adult lives. If anything is not satisfactory in their lives, they wait for the government to deal with it, even it takes some street protests. Seldom are other solutions, solutions based on private initiative, even considered. But the fault for their helplessness lies with more than their own passive attitudes. An overwhelming sense of fairness and an exaggerated demand for safety combine with the government’s unceasing quest for revenue to make starting a small business, for example, difficult and expensive. France is a country where you first fill forms for permission to operate, and then pay business taxes before you have even earned any business income.

The French have democratically built for themselves a soft cradle that’s feeling more and more like a lead coffin. It’s not obvious enough of them understand this to reverse the trend, or that they could if they wished to. There is also some vague worry about their ability to maintain the cradle for their children and for their children’s children.

(1) I am aware of the fact that there exists a strong inverse correlation between length of week worked and GDP/capita: In general, the richer the country, the shorter the work week. Again, this is based on a kind of average. It allows for exceptions. It seems to me the French awarded themselves a short work week before they were rich enough to afford it.

(2) You may wonder why I don’t mention the French debt ratio (amount of public debt/GDP). All the amenities I describe must cost a lot of money and the temptation to finance them partly through debt must be great. In fact, the French debt ratio is lower than the American: 96% to 109% in 2018 according to the International Monetary Fund. This is a little surprising but all debtors are not equal. A country with near full employment and plenty of talent is better able to pay off its debts than one with high long term unemployment and a labor force decreasingly accustomed to laboring. The latter is, of course, a predictable result of inter-generational unemployment and underemployment. Nowadays, it’s common to cross paths in France with people over thirty who have never experienced paid work. International investors think like me about the inequality of debtors. Investors flock to the US but they are reserved about France.

[Editor’s note: You can find the entire, longform essay here if you don’t want to wait for Parts II and III.]

The French Have It Better?

As I keep saying, facts matter. Facts matter more than ideological consistency if you want to know. That’s why I keep comparing us with the other society I know well, France. I am up-to-date on it, a task facilitated by the fact that I read a major French newspaper online every day, by the fact that I watch the French-language Francophone television chain, TV5, nearly every day, and by occasional recourse to my brother who lives in France. My brother is especially useful as a source because he is well-informed by French standards, articulate, and an unreconstructed left-of-center statist. I suspect he has never in his life heard a clear exposition of how markets are supposed to work. He is a typical Frenchman in that respect.

I almost forgot: I must admit that I watch a French soap opera five days a week at lunchtime. And finally, I spy on my twenty-something French nieces and nephews through Facebook. I never say anything to them so they have forgotten I am their so-called “friend.” I almost forgot again: Until recently, I went to France often. Every time I was there, I made it my duty to read local newspapers and newsweeklies and to listen to the radio and to watch the news on television. I said “duty” because it was not always fun.

So, those are my credentials. I hope you find them as impressive as I do.

And, incidentally, for those who know me personally, mostly around Santa Cruz, the rumor that I am a guy from New Jersey who fakes a French accent to make himself interesting to the ladies, that rumor has no foundation. In fact, the accent is real. French is my first language; the accent never went away and it’s getting worse as my hearing deteriorate. I like to write in part because I don’t have much of an accent in writing. Got it?

I found out recently that the French national debt to GDP ratio is about 85. That is, French citizens, as citizens, owe 85 cents for every dollar they earn in a year. The debt is a cumulative total, of course, And “national debt” refers to what’s owed by the national government of a country. The private debt of the citizens of the same country is an unrelated matter. Another way to say the same thing is that, should you reduce the national debt of your country down to zero, it wouldn’t help you directly with your personal credit card balance. (It might help you indirectly to some extent because you wouldn’t be in a position anymore to compete with the federal government for credit. This competition raises interest rates.)

The national debt also does not include the debts of states and local governments. In this country, the aggregate of these non-federal government debts is also high because of our decentralized structure. Let me say it another way: The national debt, associated entirely with the federal government, is a relatively small fraction of the total debt US citizens owe by virtue of the cost of their overall system of government. It’s relatively small as compared to the same quantity for France, for example. The French national debt includes most sub-debts that would be counted as state debt and local debt in this country. Accordingly, the French national debt is overestimated as compared to ours. If French accounting were like ours the French national debt would be considerably less than 85% of GDP.

Well, you ask: What’s ours, our national debt as a percentage of GDP? Fair enough:

It’s about 100% of GDP, 15 points higher than the French percentage. We are closer to Greece than France is in that respect.

This pisses me off to no end. The divergence between the directions taken by French society and American society occurred during my adulthood. I witnessed that divergence in concrete terms through my French relatives and directly, through my visits to France, and the occasional longish sojourn there, and so forth. So, let me summarize what I saw in France during the past thirty years.

The French eat better than Americans. They always did but their food could have become worse under “socialism.” Even the children who stay at school over lunch eat good meals for a nominal sum. School lunches in the average French town taste better than the fare of a better-than-average American restaurant, in my book.

The French have longer vacations than Americans. That’s all of them, all Americans, including civil servants and bricklayers’ union members. Five weeks is the norm in France. You read that right: 5!

In many French municipalities – I am tempted to say “most” but I have not done the research – children go skiing at public expense one week each year or more. There are also many subsidized “initiation to the sea” summer camps.

It’s also true that Americans have bigger houses and bigger cars than do French people. Personally (and I am a kind of small expert on the topic) I think French universities are not nearly as good as their American counterparts. I mean that the best French universities don’t come close to the best American universities and that the worst American universities maintain standards absent in the worst French universities. Elementary and secondary French schools seem to me to be about equivalent to American schools. They also turn out large numbers of functional illiterates. But, there is more.

The French have universal health care that is mostly free. It hurts me a lot to say this but I saw it at work several times, including under trying circumstances, and the French national health care system performed fine every time. (There is an essay on this topic on this blog, I think.) I know this is only anecdotal evidence but the raw numbers don’t contradict my impression. In point of fact, French males live two years longer than American men. I realize this superior longevity could be due to any number of factors (except genetic factors, both populations are very mixed). However, it is not compatible with a truly horrendous “socialized medicine” system. And, yes, I too would like to credit Frenchmen’s longevity to regular drinking of red wine but it’s not reasonable. If it were, a health cult of red wine would have been launched by the wine industry in this country a long time ago.

The French collectively spend about half as much as we do on health care.

I can hear my virginal libertarian friends howling: The French can afford all those tax-based luxuries because they are less likely than Americans to become involved in military ventures. (And I would add, they cut out earlier, as they are now doing in Afghanistan.) But the numbers have to jibe: In the past thirty years, the US never spent more than 5% of GDP on the military. In most years, it was under 4% . Both figures include incompressibles such as veterans’ benefits that aren’t really spent to wage war, now or in the future. Those costs, about ¼ of the military budget in the average year, would be more or less made up elsewhere if they did not exist. So, it seems to me that higher military budgets cannot begin to account for the fifteen percentage points the French have over us in their national debt relative to GDP.

I am a small government conservative who would call himself a libertarian if I did not see the word as associated with pacifism. Yet, I cannot look away from these simple facts. I wish I had an answer to the quandary they pose but I don’t. Any ideas?

How the United States can woo Africa away from China

On December 13, 2018, US National Security Advisor John Bolton, while speaking at the Heritage Foundation, highlighted the key aims and objectives of ‘Prosper Africa,’ which shall probably be announced at a later date. The emphasis of this policy, according to Bolton, would be on countering China’s exploitative economics unleashed by the Belt and Road Initiative, which leads to accumulation of massive debts and has been dubbed as ‘Debt Trap Diplomacy’. A report published by the Centre for Global Development (CGD) (2018) examined this phenomenon while looking at instances from Asia as well as Africa.

During the course of his speech, Bolton launched a scathing attack on China for its approach towards Africa. Said the American NSA:

bribes, opaque agreements and the strategic use of debt to hold states in Africa captive to Beijing’s wishes and demands.

Bolton, apart from attacking China, accused Russia of trying to buy votes at the United Nations through the sale of arms and energy.

Bolton also alluded to the need for US financial assistance to Africa being more efficient, so as to ensure effective utilization of American tax payer money.

The BUILD

It would be pertinent to point out that the Trump administration, while realizing increasing Chinese influence in Africa, set up the US IDFC (International Development Finance Corporation), which will facilitate US financing for infrastructural projects in emerging market economies (with an emphasis on Africa). IDFC has been allocated a substantial budget — $60 billion. In October 2018, Trump had signed the BUILD (Better Utilization of Investments Leading to Development) because he, along with many members of the administration, felt that the OPIC (Overseas Private Investment Corporation) was not working effectively and had failed to further US economic and strategic interests. Here it would be pertinent to mention that a number of US policy makers, as well as members of the strategic community, had been arguing for a fresh US policy towards Africa.

Two key features of IDFC which distinguish it from OPIC are, firstly, deals and loans can be provided in the local currency so as to defend investors from currency exchange risk. Second, investments in infrastructure projects in emerging markets can be made in debt and equity.

There is absolutely no doubt that some African countries have very high debts. Members of the Trump administration, including Former Secretary of State Rex Tillerson, had also raised the red flag with regard to the pitfalls of China’s unsustainable economic policies and the ‘Debt Trap’.

According to Jubilee Debt Campaign, the total debt of Africa is well over $400 billion. Nearly 20 percent of external debt is owed to China. Three countries which face a serious threat of debt distress are Zambia, Republic of Congo, and Djibouti. The CGD report had also flagged the precarious economic situation of certain African countries such as Djibouti and Ethiopia.

US policy makers need to keep in mind a few points:

Firstly, Beijing has also made efforts to send out a message that BRI is not exploitative in nature, and that China was willing to address the concerns of African countries. Chinese President Xi Jinping, while delivering his key note address at the China-Africa Summit in September 2018, laid emphasis on the need for projects being beneficial for both sides, and expressed his country’s openness to course correction where necessary. While committing $60 billion assistance for Africa, the Chinese President laid emphasis on the need for a ‘win-win’ for both sides.

African countries themselves have not taken kindly to US references to debt caused as a result of China. While Bolton stated that Zambia’s debt is to the tune of $6 billion, an aide to the Zambian President contradicted the US NSA, stating that Zambia’s debt was a little over $3 billion.

At the China Zhejiang-Ethiopia Trade and Investment Symposium held in November 2018, Ethiopian State Minister of Foreign Affairs Aklilu Hailemichae made the point that Chinese investments in Ethiopia have helped in creating jobs and that the relationship between China and Ethiopia has been based on ‘mutual respect’. The Minister also expressed the view that Ethiopia would also benefit from the Belt and Road Initiative.

During the course of the Forum of China-Africa cooperation in September 2018, South African President Cyril Ramaphosa had also disagreed with the assertion that China was indulging in predatory economics and this was leading to a ‘New Colonialism,’ as had been argued Malaysian Prime Minister Mahathir Mohammad during his visit to China in August 2018.

Washington DC needs to understand the fact that Beijing will always have an advantage given the fact that there are no strings attached to it’s financial assistance. To overcome this, it needs to have a cohesive strategy, and play to its strengths. Significantly, the US was ahead of China in terms of FDI in Africa in 2017 (US was invested in 130 projects as of 2017, while China was invested in 54 projects). Apart from this, Africa has also benefited from the AGOA program (Africa Growth and Opportunity Act), which grants 40 African countries duty free access to over 6000 products.

Yet, under Trump, the US adopts a transactionalist approach even towards serious foreign policy issues (the latest example being the decision to withdraw US troops from Syria) and there is no continuity and consistency.

US can explore joint partnership with allies

In such a situation, it would be tough to counter China, unless it joins hands with Japan, which has also managed to make impressive inroads into Africa, in terms of investments, and has also been providing financial assistance, though it is more cautious than China and has been closely watching the region’s increasing debts. Japan and India are already seeking to work jointly for promoting growth and connectivity in Africa through the Africa-Asia Growth Corridor. The US is working with Japan and India for promoting a free and open Indo-Pacific, and can work with both countries for bolstering the ‘Prosper Africa’ project.

Perhaps, Trump should pay heed to Defence Secretary Jim Mattis’ (who will be quitting in February 2019) advice where he has spoken about the relevance of US alliances for promoting its own strategic interests.

There are of course those who argue that US should find common ground with China for the development of Africa, and not adopt a ‘zero-sum’ approach. In the past both sides have sought to work jointly.

Conclusion

African countries will ultimately see their own interests, mere criticism of China’s economic policies, and the BRI project, and indirectly questioning the judgment of African countries, does not make for strategic thinking on the part of the US. The key is to provide a feasible alternative to China, along with other US allies, or to find common ground with Beijing. Expecting nuance and a long term vision from the Trump Administration, however, is a tall order.

Hegemony is hard to do: China, globalization, and “debt traps”

As a result of an increasingly insular United States, with US President Donald Trump’s imposition of tariffs, China has been trying to find common cause with a number of countries, including US allies such as Japan, India and South Korea, on the issue of globalization.

While unequivocally batting in favor of an open economic world order, Chinese President Xi Jinping has also used forums like Boao to speak about the relevance of the Belt and Road Initiative (BRI) (also known as the One Belt and One Road Initiative, or OBOR). At the Boao Forum (April 2018), the Chinese President sought to dispel apprehensions with regard to suspected Chinese aspirations for hegemony:

China has no geopolitical calculations, seeks no exclusionary blocs and imposes no business deals on others.

There is absolutely no doubt that the BRI is a very ambitious project, and while it is likely to face numerous obstacles, it is a bit naïve to be dismissive of the project.

Debt Trap and China’s denial

Yet China, in promoting the BRI, is in denial with regard to one of the major problems of the project: the increasing concerns of participant countries about their increasing external debts resulting from China’s financial assistance. This phenomena has been dubbed as a ‘debt trap’. Chinese denialism is evident from an article in the English-language Chinese daily Global Times titled ‘Smaller economies can use Belt and Road Initiative as leverage to attract investment’. The article is dismissive of the argument that BRI has resulted in a debt trap:

It is a misunderstanding to worry that China’s B&R initiative may elevate debt risks in nations involved in massive infrastructure projects. Countries are queuing up to cooperate with China on its B&R initiative, but many Western observers claim the initiative will create a problem of debt sustainability in countries and regions along the routes, especially those with small economies.

The article begins by citing the example of Djibouti in Africa, and how infrastructure projects are generating jobs and also helping in local state-capacity building. It then cites other examples, like that of Myanmar, to put forward the point that accusations against Beijing of promoting exploitative economic relationships with participant countries in the BRI is far from the truth.

The article in Global Times conveniently quotes Myanmar’s union minister and security adviser, Thaung Tun, where he dubbed the Kyaukpu project a win-win deal, but it conveniently overlooked the interview of Planning and Finance Minister, Soe Win, who was skeptical with regard to the project. Said Soe Win in an interview with Nikkei:

[…] lessons that we learned from our neighboring countries, that overinvestment is not good sometimes.

Soe Win also drew attention to the need for projects to be feasible, and for the need to keep an eye on external debt (Myanmar’s external debt is nearly $10 billion, and 40 percent of this is due to China).

The case of Sri Lanka, where the strategically important Hambantota Port has been provided on lease to China (for 99 years) in order to repay debts, is too well known.

The new government in Malaysia, headed by Mahathir Mohammed, has put a halt on three projects estimated at over $22 billion. This includes the $20 billion East Coast Railway Link (ECRL), which seeks to connect the South China Sea (off the east coast of peninsular Malaysia) with the strategically important shipping routes of the Straits of Malacca to the West. A Chinese company, China Communications Construction Co Ltd, had been contracted to build 530km stretch of the ECRL. On July 5, 2018 it stated that it had suspended work temporarily on the project, on the request of Malaysia Rail Link Sdn Bhd.

The other two projects are a petroleum pipeline spread 600km along the west coast of peninsular Malaysia, and a 662km gas pipeline in Sabah, the Malaysian province on the island of Borneo.

During a visit to Japan, Mahathir had categorically said that he would like to have good relations with, but not be indebted to, China, and would look at other alternatives. The Malaysian PM shall also be visiting China in August 2018 to discuss these projects.

Conclusion

While Beijing has full right to promote its strategic interests, and also highlight the scale and relevance of the BRI, it needs to be more honest with regard to the issue of the ‘debt trap’ (especially if it claims to understand the sensitivities of other countries, and does not want to appear to be patronizing). While smaller countries may be economically dependent upon China, the latter should dismiss the growing resentment against some of its projects at its own peril. Countries like Japan have already sensed the growing ire against the Chinese, and have begun to step in, even in countries like Cambodia (considered close to China). A number of analysts are quick to state that there is no alternative to Chinese investment, but the worries in smaller countries with regard to Chinese debts proves the point that this is not the case. China needs to be more honest, at least, in recognizing some of its shortcomings in its dealings with other countries.

Nightcap

- Singapore, capitalism, and market socialism Scott Sumner, EconLog

- China’s Creditor Imperialism Brahma Chellaney, Project Syndicate

- Chairman Xi, Chinese Idol Ian Johnson, New York Review of Books

- Trump may be rude, but that doesn’t make him a tyrant Ted Galen Carpenter, the Skeptics

Which is bigger Ponzi scheme?

A comment on my recent post made me realize that I’ve been wrong about Social Security this whole time. It isn’t quite a giant Ponzi scheme, but if we’re being flexible with our definition of Ponzi scheme it may still be the biggest.

Many people are happy to pay into Social Security thinking they’ll get a reasonable return on their “investment”. To the extent that that’s true, and that return is financed by other people paying in (rather than on actual investments) it’s a Ponzi scheme. But others don’t pay in voluntarily. To the extent that that’s true, it’s like theft but with the robber systematically dropping some of the money. Quasi-Ponzi scheme might be a better term. Social Security paid out $615B in 2008. Let’s guess $650B for 2012. If that was all happy money, it’s one big Ponzi scheme.

But the U.S. government has another project that more closely resembles a Ponzi scheme: Treasury bonds. Here people voluntarily fork over money for a return that is financed in part by later “investors” buying Treasury bonds. Of a $3.5T budget with a $1T deficit, 6% went to paying interest last year (that’s $223B). So 29% of the budget was deficit, and we might conclude that approximately $65B of interest (0.29*$223B) is “Ponzi-financed”.

So now the question is how much of Social Security is “happy money”? Anything more than 10% makes it the bigger Ponzi-scheme. But even if Social Security is heavily financed with “happy money” it is still taken at gun point while purchasers of bonds are there voluntarily. If the government were looking to save $223B and only Social Security benefits and interest payments were on the table, the more ethical choice is to default (if not repudiate). As I recall, I’m ripping off this point from Jeff Hummel.

National Economic Systems: An Introduction for Intelligent Beginners – 3

My Debt, your Debt and Future Poverty.

I told you in previous installments of this series of essays that we, in the USA, are not facing one economic crisis but two.

The fist crisis is a recession. It’s a common event in the long run of market economies. Recessions are defined by serious people (according to me) as two consecutive quarters or more of economic shrinkage. Recessions go away whether any government does anything about them or not. One school of thought (Keynesian), to which the Obama administration belongs, maintains that large government spending – stimulation- can lessen or shorten a recession. I argued that the Obama stimulus package of several months ago cannot possibly stimulate, even if you believe in the stimulation scenario.

The second crisis, by far the most serious, is the abnormally high debt the federal government has incurred since President Obama came to office. It disturbs me because the people, you and I, will have to pay interest on the debt for a long time, and eventually re-pay the principal. Else, the government will have to repay its debt in bad currency, in devalued or in eroded currency. If this happens, we will simply all be poorer, in real terms, If your dollar is worth half in ten years of what it is worth now, you will simply have to pay two dollars for what you buy today for one dollar. There is no reason to assume your income will automatically follow. This is a common fallacy (perhaps the topic for another essay): It takes about forty Indian rupees to buy a US dollar today and the same mountain bike that costs 400 US dollars in this country costs 600 US dollars in India. A good income in India would be 12,000 dollars per year. (That’s about twelve times the national average.) Continue reading

Around the Web: Consortium Edition

Co-editor Fred Foldvary points out that slavery is alive and well today.

Historian Michael Adamson compares the debacle in Iraq to South Vietnam rather than Germany or Japan.

Ninos Malek explains how property rights are the key to environmental conservation efforts.

Jeffrey Rogers Hummel takes on anthropologist David Graeber.