- The future of God in 1943 Tim Stanley, History Today

- Against the old clichés, Anne Applebaum, New Criterion

- French colonialism lives on in Africa Thomas Fazi, spiked

- A free-market gold standard? George Selgin, Alt-M

gold standard

Nightcap

- How the Arabic language spread Barnaby Rogerson, History Today

- Post-Ottoman ethnic cleansing Christopher Kinley, Origins

- Legal decentralization and the Ottoman Empire NOL

- Fear of a gold planet Larry White, Alt-M

Nightcap

- The case for empathy Elizabeth Segal, Aeon

- Christianity: an internationalist perspective Ross Douthat, New York Times

- Who’ll defend freedom? Chris Dillow, Stumbling & Mumbling

- Judy Shelton speaks up for the gold standard David Glasner, Uneasy Money

Nightcap

- Good riddance to cultural Christianity James Rogers, Law & Liberty

- When failure succeeds Chris Dillow, Stumbling & Mumbling

- Interest rates and the gold standard Larry White, Alt-M

- Trump’s America, Netanyahu’s Israel Adam Shatz, London Review of Books

Joakim Book: Winner of the 2018 Money Metals Exchange & Sound Money Defense League essay contest

Just to keep readers up to date, Joakim just won a scholarship for an essay on sound money and banking. Here is the link to the essay. Here is the link to the announcement. It reads as follows:

For the third straight year, Money Metals Exchange, a national precious metals dealer recently ranked “Best in the USA,” has teamed up with the Sound Money Defense League to offer the first gold-backed scholarship of the modern era. These groups have set aside 100 ounces of physical gold to reward outstanding students who display a thorough understanding of the economics, monetary policy, and sound money.

A gold-backed scholarship?! Freakin’ awesome. Here is Joakim’s latest post at NOL, which was highlighted at the Financial Times‘ “Alphaville” blog (the FT is like the Wall Street Journal for countries that were once part of the British Empire).

One of the things I liked most about Joakim’s latest blog was the fact that he incorporated a post by another Notewriter into his thoughts (in this case Rick’s musings on Mariana Mazzucato and counterfactuals). The folks at “Alphaville” have been good to us over the years, too. They’ve linked, since 2017, to thoughts from Shree, Federico, Vincent (twice!), Mark, and Tridivesh as well as Joakim.

Joakim’s well-deserved award stacks up quite nicely with Lucas’ 2018 Novak Award from the Acton Institute and Nick’s winning entry for the Mont Pelerin Society’s 2018 Hayek essay competition. All in all, it’s been a good year for the Notewriters.

Josh Barro and the Gold Standard

A few days ago, when it was announced that former Cato Institute president John Allison was under consideration for treasury secretary, Josh Barro of Business Insider dismissed the man as a “nutcase”. Why? Because Allison believes that the Federal Deposit Insurance Corporation (FDIC) generates a moral hazard that contributes to financial crises (a statement I agree with).

This slur irked one of the economists at Cato, George Selgin, who took to twitter to challenge Barro. In the exchange, at one point, Barro indicated that the desire of libertarians to return to the gold standard confirms the “nuttiness” of libertarians and the people at Cato.

And here, Barro allows me to make a comment on the gold standard. The sympathy towards the gold standard is not sympathy towards gold per se, but rather sympathy for reducing the capacity of governments to exercise discretion. Basically, each time you hear some academic economist mention the gold standard, what that economist means is rules-based monetary policy.

The gold standard era (1875-1914) was not an image of perfect monetary policy. It is not a lost paradise that we ought to strive to. However, the implicit rules imposed by the system did favor more stability that would have been the case with discretion during that era. In fact, the era of central banking with the Federal Reserve has not been that great relative to the gold standard era (and in the world of central banks, the Fed is pretty good). A lot of the scorn that the gold standard era has received had to do with regulatory policy towards banks (notably regarding restrictions on branch banking which forced more volatility) or with the role of changes in international demand for assets (see here). Thus, in spite of its many flaws, the gold standard was not that bad (but it was not* gold per se that was helpful – it was the shunning of discretion by governments).

To be sure, I do not favor a return to a gold standard era. What I do like, and what I think John Allison likes as well, is the return to rules-based monetary policy. Josh Barro should have been intellectually generous and understand this key distinction. By not making that distinction, of which he must be aware given his background, he debased the debate over monetary policy.

The Gold Standard is Not Without its Costs

News from the department of “life is bigger than art:” A few days ago I posted a fictitious account of a future Wells Fargo Bank operating on a revived gold standard. Turns out the real Wells Fargo, now a regular large commercial bank with its roots in the California gold rush, has a branch in downtown San Francisco at the site where the bank was first opened in 1852. The branch had an exhibit of historic artifacts, including gold nuggets from the gold rush era. I say had, because last night thieves rammed an SUV into the lobby and made off with the nuggets!

All of which underscores the fact that security is among the real costs associated with a gold standard. There is no law of nature that says free banking has to be based on gold, as I pointed out in my post. The market would, if free to do so, sort out costs and benefits and find the sort of system or systems that best satisfies consumers.

I love Wells Fargo; They Hate Me.

While I have this blog window open I’ll add some unrelated comments about Wells Fargo. I am a happy customer and I credit this to the stiff competition among banks at the retail level. I regularly get solicitations from banks offering $100 bonus to open an account, with strings attached, of course but I stick with Wells Fargo. At the macro level our current banking system is gravely flawed but it works well for us retail customers.

I get free checking, a handy web site, and ATMs all over the place. When my credit card was hacked recently, they replaced it promptly and took my claims about false charges at face value. My average credit card balance last year was nearly $4,000 and I paid zero interest. That’s because I pay it off at the last possible date, which is 25 days after billing. I pay an $18 annual fee but got $300 in cash rebates last year. I never pay late fees or penalties of any kind.

I do not have a savings account with Wells Fargo because those accounts are a joke. Their most popular savings account yields (drum roll) 0.01%. Not one percent, but one hundredth of one percent. For every thousand dollars I might keep in a savings account, I would get ten cents in annual interest, taxable. I do, however, hold shares of Wells Fargo preferred stock which pay 6.8% current yield (for you experts, a somewhat lower yield to call). The shares appreciated about 70% since I bought them at the bottom of the Great Recession.

So I am a money loser for Wells Fargo. They earn merchant fees from my credit card use and that’s about it. They count on their average customer’s ignorance and lack of financial discipline to generate fee income and to carry high-interest balances on their credit cards. Dear reader, if that describes you, don’t despair. You can get out in front of the wave and let the banks work for you, not the other way around. It just takes a little knowledge and some discipline. Most important: if you can’t pay cash for a purchase (or use a credit card paid off before interest kicks in), you can’t afford it! That includes cars. Save up your money and buy a junker. Mortgages are OK for home purchases because of tax breaks, but even there, start with a healthy down payment.

Here endeth today’s sermon. Go in peace and freedom!

A Tale of Free Banking

Herewith we visit an imaginary future where free banking prevails. Government regulation of banks is a thing of the past. Banks have the freedom and the responsibility that they lacked under government regulation. In particular, private banks are free to print money, either literally, in the form of paper banknotes for the shrinking number of customers who want them, but in electronic form for most.

Print money? Horrors, you say! Fraud! Runaway inflation!

Not so fast. Come with me on a fantasy visit to the local branch of my bank, a future incarnation of Wells Fargo to be specific.

The first thing we notice is a display case showing a number of gold coins and a placard that says, “available here for 1,000 Wells Fargo Dollars each, now and forever.” I have in my wallet a number of Wells Fargo banknotes in various denominations. I could walk up to a teller and plunk down 1,000 of them and the smiling young lady would hand over one of these coins. More likely I would whip out my smartphone and hold it up to the near-field reader, validate my thumbprint, and complete the transaction without paper.

I have a few of these beautiful gold coins socked away at home but I don’t want any more today nor do I want to carry them around. Electronic money is ever so much safer and more convenient. Still, I am reassured by the knowledge that I could get the gold any time I wanted it. That is the basis for my confidence in this bank, not the FDIC sticker we used to see in the bank’s window.

Confidence? What about inflation? Wells Fargo can create as many of these dollars as they want, out of thin air. Without government regulation, who will stop them from creating and spending as many dollars as they want?

The market will stop them, that’s who.

In my scenario, Consumer Reports and a number of lesser known organizations track Wells Fargo and other banks. These organizations post daily figures online showing the number of Wells Fargo dollars (WF$) outstanding and the amount of gold holdings that the bank keeps in reserve to back these dollars. Premium subscribers, I imagine, can get an email alert any time a bank’s reserves fall below some specified levels. Large depositors will notify Wells Fargo of their intention to begin withdrawing deposits and/or demanding physical gold. Small depositors piggyback on the vigilance efforts of big depositors. They know it is not necessary for them to pester the bank when the big guys are doing it for everybody.

Wells Fargo practices fractional reserve banking. They cannot redeem all their banknote liabilities and demand deposit liabilities at the stated rate of one ounce of gold per thousand WF$. This situation is clearly outlined in the contract that depositors sign and is printed on their banknotes.

Let’s assume Wells Fargo backs just 40% of its banknotes and deposits with physical gold. How is this figure arrived at? By trial and error. Managers believe that if they let the reserve ratio slip much below 40% they will start getting flak from the monitoring websites and their big depositors. If they let it rise much above that figure their stockholders will begin complaining about missed profit opportunities.

Under fractional reserve banking, bank runs are possible. A bank run is a situation where a few depositors lose confidence in a bank and demand redemption of their deposits in gold or in notes of another bank. Seeing this, other depositors line up to get their money out, and if left unchecked, the bank is wiped out along with the depositors who were last in line. Bank runs are not a pretty sight.

Wells Fargo has a number of strategies for heading off a bank run. They have an agreement with the private clearing house of which they are a member that allows the bank to draw on a line of credit under certain circumstances. There is a clause, clearly indicated in the agreement with their depositors, allowing them to delay gold redemption for up to 60 days under special circumstances. They can reduce the supply of WF$ by calling in loans as permitted by loan agreements. Most important, though, is Wells Fargo’s reputation. Not once in their long history has Wells Fargo been subject to a bank run. Management is keenly aware of the value of their reputation and will move heaven and earth to preserve it.

To sum up, Wells Fargo’s ability to create unbacked money is limited by the public’s willingness to hold that money. The bank can respond to changes in the demand to hold WF$ whether those changes are seasonal in nature or secular. They have strategies in place to head off runs should one appear imminent or actually begin.

What about competing banks, you may ask. Does Bank of America issue its own money? If so, there must be chaos with several different brands of money in the market. Are there floating exchange rates? Is a BofA$ worth WF$1.05 one day and WF$0.95 the next? What else but government regulation could put an end to such chaos?

The market, that’s what else.

Competing suppliers of all sorts of products have an incentive to adhere to standards even as they compete vigorously. If we were in a classroom right now I would point to the fluorescent lights overhead. The tubes are all four feet long and 1.5 inches in diameter, with standard connectors. They run on 110 volt 60 Hz AC current. Suppliers all adhere to this standard while competing vigorously with one another. If they don’t adhere to the standards people won’t buy their light bulbs.

So it is that competing banks in my fantasy world have all converged on a gold standard. They all adhere to the standard one ounce of gold per thousand dollars. (I trust it’s obvious that I just made up this number. Any number would do.)

Why gold? Gold has physical properties that have endeared it to people over the ages—durability, divisibility, scarcity to name a few. But other standards might have evolved such as a basket of commodities—gold, silver, copper, whatever.

You may raise another objection. All this gold sitting in vaults detracts from the supply available for jewelry, electronics, etc. That’s a real cost to these industries and their customers.

Yes, it is. It’s called the “resource cost” of commodity-backed money. To get a handle on this cost we must recognize that gold sitting in vaults is not really idle, but is actively providing a service. It is ensuring a stable monetary system immune from political meddling. How valuable is that? The market will balance the benefits of stability against the resource costs of a gold standard.

Furthermore we can expect resource costs to decline slowly as confidence in the banking system increases and people are comfortable with declining reserve ratios. Wells Fargo may find that a 30% reserve ratio rather 40% will be enough to maintain confidence. Other things equal, this development would boost profits temporarily, but those profits would soon be competed away, to the benefit of depositors and the economy as a whole.

Let’s go back to bank runs. Aren’t they something horrible, to be avoided at all costs?

Actually an occasional bank run is something to be celebrated. Not for those involved, of course, but to remind depositors and bank managers alike that they need to be careful. The same is true of the recent Radio Shack bankruptcy. Bad news for stockholders, suppliers and employees but an opportunity for competitors to learn from this bankruptcy.

Under my free banking scenario, depositors must take some responsibility for their actions. That doesn’t mean they have to become professional examiners. They just have to take some care to check with Consumer Reports or other rating organizations before signing on with a bank.

Have I sketched out a perfect situation? There’s no such thing as perfection in human affairs but I submit that this situation would be vastly superior to what we have now, where the Federal Reserve’s policy of printing money to finance government deficits will end badly. Furthermore, relatively free banking has existed in the past and worked well. To learn more, start with Larry White’s “Free Banking in Britain.”

Tamny on Fractional-Reserve Banking: Right Conclusion, Faulty Analysis

John Tamny has posted a long and thought-provoking piece entitled “The Closing of the Austrian School’s Economic Mind.” He begins with a cogent critique of the anti-fractional-reserve stance of certain Austrian economists at the Mises Institute. Unfortunately, he follows that with a discussion of fractional reserves, the money multiplier, and other issues in which he goes badly astray.

As Tamny says, it is only some Austrians who have a problem with fractional-reserve banking. I consider myself an Austrian but I do not share the view of fractional reserves of the Mises Institute contingent, whom I prefer to call hard-money advocates.

The alleged problem, as the hard money people have it, is that under fractional reserves it appears that two people have a claim on the same dollar. This, they say, is fraud. But it is not fraud if the arrangement is disclosed to all parties. There are problems with our present-day fractional-reserve system, which I discuss below, but fraud is not one of them. (Incidentally, Tamny scores a point when he wonders about the hard money people calling in the state to crush the alleged fraud, but I believe most of them are anarchists and would have private protection agencies do the job. Just how this might work is beyond me.)

Tamny recognizes that fractional-reserve banking is the norm in all modern societies but he goes a little too far when he says fractional-reserve banking is a tautology. Modern banks do offer warehousing of money to those few who want it, via safe-deposit boxes. Anybody can rent one and stuff it full of currency or near-money assets like gold coins, and of course pay an annual fee. This is a minor sideline for banks, but it exists, so there is no tautology.

Also, contrary to Tamny, it is possible for a well-run business to fail for lack of money. This can happen if the supply of money in an economy falls short of the demand to hold it. (We must not mistake the demand to hold money with the demand to acquire money for spending. We all want to hold a certain level of cash, enough to cover emergencies or unexpected bargains but not so much as to pass up good opportunities for spending or investing it.) Money supply can get out of balance with money demand when there is a monopoly supplier, as there is in all modern economies, which has no market forces to tell it how much money to issue. There would be such forces in a free banking system, which is a topic for another time.

I promised to mention problems with fractional-reserve banking. The first is that government control of the banking system has short-circuited market forces that would signal to bank managers the amount of reserves they ought to keep on hand. If managers keep too little in reserves, they risk a liquidity crisis, or short of that, fear of a crisis on the part of depositors or would-be depositors. If they keep too much, they pass up profit opportunities and dis-serve their shareholders. The safety of a fractional-reserve bank depends critically on its reputation for prudence in lending. Without government interference in the forms of both controls (among them reserve requirements, capital requirements, and asset restrictions) and support (two that come to mind are Federal deposit insurance and the privilege of borrowing from the Federal Reserve), managers would very likely be more prudent about lending, and even more, about maintaining their reputation for prudent lending. Depositors would come to understand banks as something more like a mutual fund than a piggy bank.

This first point is not a strike against fractional reserves, but the government’s failure to let a free-market fractional-reserve system work honestly and efficiently.

The second problem is the flip side of the first. Federal Deposit Insurance relieves depositors of any incentive to question the soundness of their bank’s lending process. Depositors have no reason to look beyond the FDIC sticker in the window. Such is not the case with mutual funds which bear some resemblance to fractional-reserve banks. Most fund investors look carefully at ratings before investing. FDIC insurance does not eliminate risk, it socializes it, wreaking all sorts of distortions in the process.

I agree with Rothbard that occasional bank failures, leaving depositors and shareholders as well as other bank creditors empty-handed, should be welcomed because they put the fear of God into managers and depositors alike.

An advantage of a fractional reserve system over a 100% gold-backed system is that the latter would suck almost all the world’s supply of gold into underground vaults leaving very little for industrial or ornamental uses. Fractional reserves free up a lot of that gold for these uses, more so over time as the reserve levels needed to maintain confidence in the system fall as the system works well and confidence increases.

Tamny next takes up the money multiplier, and in so doing goes wildly off the rails. He cites the textbook example:

- Someone deposits $1,000 cash in bank A

- Bank A lends out $900 and keeps $100 cash as reserves

- The recipient of the $900 deposits it in bank B which loans out $810 and keeps $90 cash as reserves

- The $810 is deposited in bank C, and on it goes.

Textbooks use this example to show how money is created by fractional-reserve banks via a multiplier which approaches 1/r where r is the fraction of deposits maintained as reserves by each bank, 1/0.1=10 in the example. The new money is categorized as M1, which includes currency and travelers’ checks in addition to demand deposits (checking account balances).

So is M1 really money? Most definitely, because it fits the definition perfectly: a generally accepted medium of exchange. Is there anyone reading this piece who does not keep much more of his money in a checking account than in cash? How often do we pay cash these days? We use our debit cards, paper checks, or on-line transfers instead of currency. Or we use credit cards which we pay off by on-line transfer or check. All this is M1 money, all created by private banks under the aegis of fractional reserve banking. Notwithstanding the problems cited above, it all works rather well.

Tamny will have none of it. He goes through the same textbook exercise, imagining a group of friends in a room instead of a sequence of banks. He is wrong to say that no money is created in the process. To be sure, the amount of currency in circulation has not increased but he fails to notice that M1 money has increased. That’s because each loan recipient has, in addition to some currency, a bank balance that he correctly believes he can spend without ever converting it into currency: M1 money. Tamny could give each borrower in his thought experiment an old-fashioned bank book as evidence of the new money. We have here the nub of Tamny’s problem: his failure to recognize that M1 money (or rather the demand deposits that dominate that category) is real spendable money.

Tamny says money doesn’t grow on trees, but he’s wrong. The Fed creates base money out of thin air, as I’m sure Tamny agrees, but most money creation is done by private banks via the multiplier. And in truth, a fractional reserve system does create real wealth in the long run relative to a 100% reserve system because it increases the efficiency of the money and banking system, freeing up resources for alternate productive uses.

Is the fractional-reserve system inflationary? Yes, when currency flows into banks and is multiplied, it is. The reverse process is deflationary. But if overall bank reserve levels hold steady no price inflation is triggered, other things being equal.

Tamny’s use of NetJets as an analogy to fractional-reserve banking is flawed. The same jet plane cannot be in two different places at the same time. But two dollars of checking account money, each having its origin in the same dollar of currency deposited, can both be spent. Yes, money does grow on fractional-reserve trees. No, real wealth does not.

Tamny asks, if banks can multiply money, why can’t the same be done by “enterprising entrepreneurs eager to quickly turn $1,000 into $10,000 without doing anything?” They can actually, but they must do a lot of work first, like raising capital, setting up an office and web site, rounding up depositors and borrowers. To see details, go to www.startabank.com. The barriers to entry caused by licensing and such are actually rather modest.

Incidentally, the failure to recognize demand deposits as money goes back at least to the Currency School in 1840’s England. This school of thought held that bank notes should be backed 100% by gold but failed to understand that checks payable on demand were also money and required backing.

“Credit is not money,” says Tamny. What is it, then? “Credit is real resources.” But this is a wide departure from the accepted meaning of the term and one that leads to all sorts of confusion. The common definition of credit is a willingness or commitment of lenders to provide loans to certain parties under certain conditions. Businesses often carry lines of credit with banks. Individuals have credit limits on their credit card accounts. No, credit is not money, but it comes close. We feel reassured by credit commitments which we can tap into when needed. Credit is a way to buy stuff, not the stuff itself. I should add that later in the same paragraph Tamny calls credit access to real resources (my emphasis). This is closer to the mark but is not the defining characteristic of credit. Stuff can be bought on credit or with currency or barter. Again, credit is the willingness or commitments of lenders to loan money. But later in the piece Tamny flips back to credit as “resources in the real economy.”

At one point he says true inflation is “devaluation of the dollar.” No, devaluation refers to a drop in exchange rates for a particular currency relative to other currencies. Devaluation is often but not always accompanied by inflation. I’ll give him a pass on this and assume he means true inflation is a drop in the dollar’s purchasing power.

Elsewhere he denies any role for Fed-induced “easy credit” in the housing bubble. It may not have been the dominant factor, and it may have been overpowered by countervailing factors in the examples he cites, but can there be any doubt that lower interest rates stimulate the quantity of housing demanded, other things being equal? Don’t mortgage payments consist almost entirely of interest in the early years? Exercise for the reader: how much more house can you afford given $3,000 per month to spend on a 30-year mortgage if the rate drops from 5% to 4%? Answer: a lot more.

Another Tamny claim is that a growing economy always needs more money. This seems right, since growth generally means more of everything. But as clearing and payment system efficiencies increase, as we turn more to debit cards, credit cards, PayPal, and whatever comes next, our desire to hold money declines. This countervailing tendency could cancel out most or all of the effects of growth on money demand.

Tamny calls government oversight of money “horrid” and wishes for abolition of the Fed. Amen to both, but how can he be sure that, as he claims, credit would soar as a result? It probably would in the long run as sound money prompted increased confidence, but in the short run there could be liquidation of mal-investments and a general hesitation to save and invest pending clarification about where things were headed under the new setup.

John Tamny is correct: the anti-fractional-reserve crusade of the hard-money people is misguided. That case has been made repeatedly, deftly, and at length by Larry White and George Selgin, two of the best contemporary monetary economists. Sad to say, Tamny’s analysis, riddled as it is with errors and confusions, falls far short of their work.

Free Banking Beats Central Banking

In “More Bits on Whether We Need a Fed,” a November 21 MarginalRevolution blogpost, George Mason University economics professor Tyler Cowen questions “why free banking would offer an advantage over post WWII central banking (combined with FDIC and paper money).” He adds, “That’s long been the weak spot of the anti-Fed case.”

Free banking is better than central banking because only in a free market can the optimal prices and quantities of goods be determined. Those goods include the money supply, and prices include the rate of interest.

There is no scientific way to know in advance the right price of goods. With ever-changing population, technology, and preferences, markets are turbulent, and there is no way to accurately predict fluctuating human desires and costs.

The quantity of money in the economy is no different from other goods. The optimal amount can only be discovered by the dynamics of supply and demand in a market. The impact of money on prices depends not just on the amount of money, but also on its velocity, that is, how fast the money turns over. The Fed cannot control the velocity since it cannot control the demand for money, that is, the amount people want to hold. Also, even if the Fed could determine the best amount of money for today, the impact on the economy takes several months to take effect, and so the central bankers would need to be able to accurately predict the state of the economy months into the future. Continue reading

Gold and Money, II

Last [blog post], we examined some propositions about gold as money, drawing from theory and history. [In] this [blog post] we ask whether and how gold might once again serve a monetary function.

Money of any sort, commodity-based or not, derives its value in large part from what economists call a “network effect.” Like a fax machine, whose value depends largely on how many other people have fax machines, we value money because other people value it. We feel confident our money will buy us what we need tomorrow. A strong network effect means that something drastic has to happen before people will give up their familiar form of money.

Something drastic was happening when U.S. Rep. Ron Paul’s Gold Commission was set up in 1979. By the time the commission’s report was issued in 1980, inflation had reached alarming levels: The consumer price index was at 14 percent and rising. The prime rate was over 20 percent, and in 1980 silver exploded to $50 an ounce and gold surpassed $800 (about $2,300 in today’s dollars). Bestselling books urged people to buy gold, silver, diamonds, firearms, and rural hideouts.

We now know that inflation was peaking and that the silver price spike was a fluke caused by a failed attempt to corner the silver market. But none of this was apparent at the time, so it was reasonable to wonder whether our monetary system would survive. What did happen, of course, was that the new Fed chairman, Paul Volcker, stepped on the monetary brakes hard enough to break the back of inflation. Two back-to-back recessions resulted but were followed by a long period of recovery in which both inflation and interest rates dropped steadily. The Gold Commission was largely forgotten, though the U.S. Mint did get into the business of producing gold coins in a big way. Continue reading

Gold and Money

Nothing seems to arouse passions—pro and con—quite like suggestions that gold should once again play a role in our money. “Only gold is money,” says one side. “It’s a barbarous relic,” says the other. Let’s turn down the heat a bit and look into some propositions about gold. That should lead us to some reasonable ideas about whether or how gold might return.

Propositions About Gold

Gold has intrinsic value. Actually, nothing has intrinsic value. The value of any good or service resides in the minds of individuals contemplating the benefits they might derive from it. What gold does have is some rather remarkable physical properties that make it very likely that people will continue to value it highly: luster, corrosion resistance, divisibility, malleability, high thermal and electrical conductivity, and a high degree of scarcity. All the gold ever mined would only fill one large swimming pool, and most of that gold is still recoverable.

Only gold is money. Although gold was once used as money, that is no longer the case. Money is whatever is generally accepted as a medium of exchange in a particular historical setting. Right now, government-issued fiat money, unbacked by any commodity, is the only kind of money we find anywhere in the world, with some possible obscure exceptions.

Perhaps people who say this mean that gold is the only form of money that can ensure stability. That’s what future Federal Reserve Chairman Alan Greenspan thought in 1967, when he wrote “Gold and Economic Freedom” for Ayn Rand’s newsletter. “In the absence of the gold standard, there is no way to protect savings from confiscation through inflation,” he said. When later asked by U.S. Rep. Ron Paul whether he stood by that article, Greenspan said he did. But he weaseled out by saying a return to gold was unnecessary because central banks had learned to produce the same results gold would produce. Continue reading

“Gold and Money”

That’s the title of this piece in the Freeman by our very own Dr. Gibson. In it, he suggests:

Let’s turn down the heat a bit and look into some propositions about gold. That should lead us to some reasonable ideas about whether or how gold might return.

Indeed. I’m tempted to copy and paste the whole thing, but just check it out.

PS I’ve been a very busy man lately, but I’ve got a bunch of almost-finished writings in the works. Stay tuned!

Lost in the Hulaballoo

…was Ron Paul’s hearing on fractional reserve banking. Between the health insurance ruling and AG Holder’s scandal this excellent use of congressional air time has gone largely unnoticed. Congressman Paul brought three well-known economists to testify and I have linked to all three of their testimonies below (I haven’t read all of them yet).

If you manage to finish them soon, feel free to post what you got from them in the comments section.

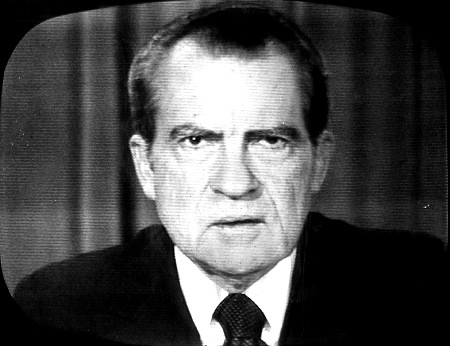

August 15, 1971

People who were alive in 1941 can tell you right where they were on Pearl Harbor day. I can tell you exactly where I was when I heard that President Kennedy had been shot. We all remember 9/11. Another day that I sticks in my memory just as clearly is one that is now remembered by few: Sunday, August 15, 1971.

There was no internet in those days and no cable news channels, so I was mercifully spared the news until the following morning at 8:15 when I opened my motel room door in Huntington Beach and saw the L.A. Times on the doorstep with a headline that said something like “Nixon Imposes Price Controls.”

I was shocked and disgusted for two reasons: though I was employed as an aerospace engineer, I was beginning to learn about free markets, having attended a FEE seminar the year before at which Mises and Hazlitt – now saints of Austrian economics – lectured. And I had voted for Nixon in 1968, naively believing the Republicans were the party of free markets. The following year I signed up with the new Libertarian Party and never looked back on the Republicans until 2008 when Ron Paul ran.

Here is a video recording of Nixon announcing a 90-day “freeze” on prices and wages. Note the Orwellian references to the evils of price controls even as he imposes them.

So what was the big emergency that prompted such a drastic response? Unemployment was running about 6%; price inflation at about 5%. Nixon’s problem was that an election was coming up in the following year. He remembered bitterly his narrow loss to Kennedy in the 1960 election which he attributed to a mild recession of that year. Now he was determined to goose the economy and get himself re-elected. Like FDR, Nixon loved dramatic strokes and never mind the consequences. Earlier that year the man who had made his reputation as an implacable anti-communist had made a sudden and dramatic overture to communist China. So on that sleepy Sunday Nixon delivered another bold stroke, in an end run around the Democratic opposition. Perhaps it worked: he won 49 states in the 1972 election with considerable help from his bumbling opponent, George McGovern.

His action was quite popular. The stock market surged that Monday morning and polls showed a 75% approval rate. But Milton Friedman was right when he predicted “utter failure and the emergence into the open of suppressed inflation.” Another freeze was imposed in 1973 but this time the damage to the economy became evident. As explained in the excellent video series “The Commanding Heights,” “ranchers stopped shipping their cattle to the market, farmers drowned their chickens, and consumers emptied the shelves of supermarkets.” Inflation reached a peak of about 14% before the decade was out and before the powers that be accepted the fact that excessive money creation is the main cause of price inflation. George Schulz, Nixon’s economic advisor and a vigorous opponent of price controls consoled himself with the thought that Nixon had demonstrated dramatically how not to fight inflation.

Nixon wasn’t finished. During that same Sunday broadcast he slapped a 10% tariff on imported goods, accompanied by some blather about fairness. More significantly, he ended the Bretton Woods international monetary system. That arrangement, conceived in 1944, had the U.S. dollar convertible into gold at $35 per ounce, but only for foreign central banks. Not only could private banks and private citizens not convert their dollars, it was even illegal to own gold (with exceptions for dentists, jewelers, etc.). I made a point of violating that particular law on principle before the prohibition was lifted in 1974.

In all fairness, the Bretton Woods system was doomed long before that August. The gold exchange standard had persisted only because of a gentlemen’s agreement that European central bankers would refrain from exercising their redemption rights to any significant degree. So many new dollars had been created to finance Lyndon Johnson’s war in Vietnam and his “Great Society” at home, and so many of those dollars were parked overseas as a result of trade imbalances, that the U.S. government could not come close to honoring its Bretton Woods obligation in full. The French under de Gaulle and his gold-bug advisor Jacques Rueff had become increasingly strident about the situation, but in early August the British ambassador showed up with $3 billion to be redeemed, and that may have been the straw that broke the camels back.

So on that same Sunday Nixon slammed the gold window shut (video here) pushing us out of the frying pan of Bretton Woods, under which numerous wrenching devaluations had wracked international trade, into the fire of floating exchange rates, the system we have now. The devaluations are gone but the wild swings in currency values, something that was not foreseen by Milton Friedman who was an early advocate of currency markets, are almost as bad. Now, wonder of wonders, there is resurgent talk of some sort of gold standard.

Reagan tempted me with with some pretty inspiring rhetoric in his 1980 campaign about getting the government off our backs. Not enough to vote for him, but I was glad he got elected and with the help of Fed chairman Paul Volcker he did break the back of inflation, but he never got spending under control and he didn’t deserve as much credit as he got for the fall of communism, which had been rotten at its core for decades. But Bush I was terrible and in hindsight Clinton wasn’t all bad, yet I confess I was relieved when Bush II beat Gore in 2000. I needn’t remind anyone what a disaster GWB was with his wars, his unfunded medicare expansion and his bailouts (OK, thanks for the tax cut).

I’m voting for Gary Johnson who won’t win, and I really don’t care who wins. Gridlock is the least bad outcome, even if that means the despicable Obama stays in office facing a Republican congress.