Also lingo. And beards.

Why Cuba is having an economic crisis (Noahpinion)

The Language of Totalitarian Dehumanization (Quillette)

On the Cuba events. Governments and protests, now that’s a strained relationship. Talking about the so-called “Second World” countries, Nikita Khrushchev did not even know what booing is, until he encountered it in his visit to London in 1956.

Few years later, during a massive strike in the Russian city of Novocherkassk, a crowd stormed the central police station. Whether it was a genuine assault, or a naive display of defiance from a people inexperienced in protesting, the government’s fearful puzzlement turned to cold, brutal aggression. Unarmed protesters at the center of the city, mistakenly thinking that those days were over, remained steadfast at the face of warnings to disperse. That is, until security forces opened direct fire against them. The ensuing massacre was covered-up for three decades. Since this was an à la Orwell un-event, no high-ranking officials’ records were stained.

Khrushchev’s aloof ignorance strikes a nerve, contrasted with the people’s heartbreaking one. Both glimpses are captured in the brilliant (though somewhat uneven) Red Plenty, by Francis Spufford.

All things said, Karl Marx Loved Freedom (Jacobin). More beards.

The Greek government, like its French counterpart, is escalating the push for vaccinations. As constitutional scholars argue the limits of state power regarding personal freedom and the public good, historical precedents are brought forth (for the US, c. early 1900s), involving mandatory vaccinations, quarantines and discrimination. The discussion draws from equal protection of the laws jurisprudence and smoothly led me to Yick Wo v. Hopkins (1886):

Yick Wo v. Hopkins established fair implementation of statutes (History Net)

The decision set a milestone and has been cited some 150 times.

The backdrop of the case is rich. As it turns out,

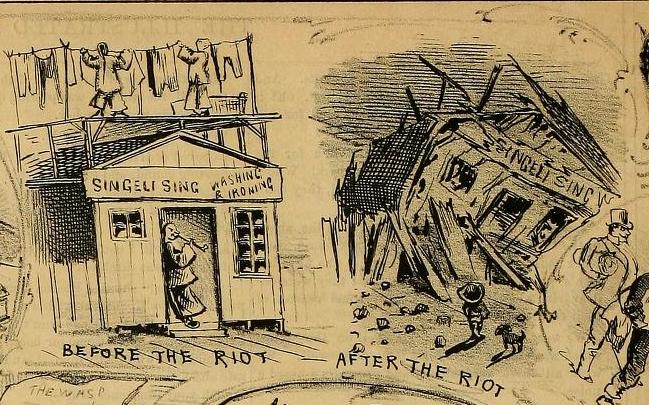

An 1880 ordinance of the city of San Francisco required all laundries in wooden buildings to hold a permit issued by the city’s Board of Supervisors. The board had total discretion over who would be issued a permit. Although workers of Chinese descent operated 89 percent of the city’s laundry businesses, not a single Chinese owner was granted a permit.

Oyez

The regulation was one in a series of many that reflected the anti-immigrant (especially anti-Chinese) sentiment, following the influx due to the Gold Rush (1849).

Yick Wo: How A Racist Laundry Law In Early San Francisco Helped Civil Rights (Hoodline)

A particularly badass line, from the unanimous opinion authored by Justice Stanley Matthews, shows that the Court did not hold back:

Though the law itself be fair on its face and impartial in appearance, yet, if it is applied and administered by public authority with an evil eye and an unequal hand, so as practically to make unjust and illegal discriminations between persons in similar circumstances, material to their rights, the denial of equal justice is still within the prohibition of the Constitution.

_-_Local_Chips_(cropped).jpg){kind=link}