I did not think that my post on NGO versus NGDP would gather attention, but it did (so, I am happy). Nick Rowe of Carleton University and the (always relevant) blog Worthwhile Canadian Initiative responded to my post with the following post (I was very happy to see a comment by Matt Rognlie in there).

Like Mr. Rowe, I prefer to speak about trade cycles as well. I do not know how the shift from “transactions” to “output” occurred, but I do know that as semantic as some may see it, it is crucial. While a transaction is about selling a unit of output, the way we measure output does not mean that we focus on all transactions. I became aware of this when reading Leland Yeager (just after reading about the adventures on Lucas’ Islands). However, Nick (if I may use first names) expresses this a thousand times better than I did in my initial post. When there is a shift of the demand for money, this will affect all transactions, not only those on final goods. Thus, my first point: gross domestic product is not necessarily the best for monetary transaction.

In fact, as an economist who decided to spend his life doing economic history, I do not like gross domestic product for measuring living standards as well (I’ll do a post on this when I get my ideas on secular stagnation better organized). Its just the “least terrible tool”. However, is it the “least terrible” for monetary policy guidance?

My answer is “no” and thus my proposition to shift to gross output or a measure of “total spending”. Now, for the purposes of discussion, let’s see what the “ideal” statistic for “total spending” would be. To illustrate this, let’s take the case of a change in the supply of money (I would prefer using a case with the demand for money, but for blogging purposes, its easier to go with supply)

Now unless there is a helicopter drop*, changes in the money supply generate changes in relative prices and thus the pattern (and level) of production changes too. Where this occurs depends on the entry point of the increased stock of money. The entry point could be in sectors producing intermediary goods or it could closer to the final point of sale. The closer it is to the point of sale, the better NGDP becomes as a measure of total spending. The further it is, the more NGDP wavers in its efficiency at any given time. This is because, in the long-run, NGDP should follow the same trend at any measure of total spending but it would not do so in the very short-run. If monetary policy (or sometimes regulatory changes affecting bank behavior “cough Dodd-Frank cough”) causes an increase in the production of intermediary goods, the movements the perfect measure of total spending would be temporarily divorced from the movements of NGDP. As a result, we need something that captures all transaction. And in a way, we do have such a statistic: input-output tables. Developed by the vastly underrated (and still misunderstood in my opinion) Wassily Leontief, input-output tables are the basis of any measurement of national income you will see out there. Basically, they are matrixes of all “trades” (inputs and outputs) between industries. What this means is that input-output tables are tables of all transactions. That would be the ideal measure of total spending. Sadly, these tables are not produced regularly (in Canada, I believe there are produced every five years). Their utility would be amazing: not only would we capture all spending (which is the goal of a NGDP target), but we could capture the transmission mechanism of monetary policy and see how certain monetary decisions could be affecting relative prices.** If input-output tables could be produced on a quarterly-basis, it would be the amazing (but mind-bogglingly complex for statistical agencies).

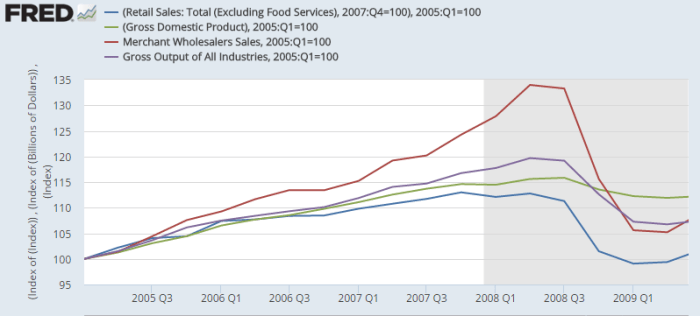

The closest thing, at present, to this ideal measure is gross output. It is the only quarterly statistic of gross output (one way to calculate total spending) that exists out there. The closest things are annual datasets. Yet, even gross output is incomplete as a measure of total spending. It does not include wholesale distributors (well, only a part of their activities through value-added). This post from the Cobden Centre in England details an example of this. Mark Skousen in the Journal of Private Enterprise published a piece detailing other statistics that could serve as proxies for “total spending”. One of those is Gross Domestic Expenditures and it is the closest thing to the ideal we would get. Basically, he adds wholesale and retail sales together. He also looks at business receipts from the IRS to see if it conforms (the intuition being that all sales should imitate receipts claimed by businesses). His measure of domestic expenditure is somewhat incomplete for my eyes and further research would be needed. But there is something to be said for Skousen’s point: total nominal spending did drop massively during the recession (see the fall of wholesale, gross output and retail) while NGDP barely moved while, before the recession, total nominal spending did increase much faster than NGDP.

In all cases, I think that it is fair to divide my claim into three parts: a) business cycles are about the deviation from trends in total volume of trades/transactions, thus the core variable of interest is nominal expenditures b) NGDP is not a measure of total nominal spending whose targeting the market monetarist crowd aims to follow; c) since we care about total nominal spending, what we should have is an IO table … every month and d) the imperfect statistics for total spending show that the case made that central banks fueled spending above trend and then failed to compensate in 2008-2009 seems plausible.

Overall, I think that the case for A, B and C are strong, but D is weak…

Interesting posts. Are there any good papers/references on input-output tables?

In terms of monetary policy, the only paper I’ve seen that I found is by a Quebec colleague of mine at HEC Montreal : http://economie.esg.uqam.ca/upload/files/seminaires/Sector3.pdf

Thanks Vincent!

So you, like me, are heavily influenced by Yeager too!

I agree with a lot of what you say. I am going to focus on one thing where we disagree. I hadn’t though before about input-output tables in this context. I’m still unsure about them. But one thing I will say is that they leave a lot of things out. Take the housing market for example. The flow of expenditures on new houses is probably small relative to the flow of expenditures trading existing (old) houses. And monetary disequilibrium can disrupt trading in old houses as much as new houses. Which means that some people will be owning when they should be renting, and vice versa. And people will be living in the wrong houses because they can’t trade houses easily. Used cars too. And real and financial assets. Once we start thinking about the Trade Cycle, and consider all trade, any measure of “output” and expenditures on “output” becomes just one part of a much bigger picture.

Now fluctuations in NGDP could never be more than an imperfect proxy for monetary disequilibrium, because even if monetary policy was perfect we would still see some fluctuations caused by other things. And it’s the same with any measure of nominal transactions. They fall at night, and every weekend, for example, and presumably not for monetary reasons. I think it has to be an empirical question, where we look at various measures and try to see which one stays relatively stable except when it really does look like monetary disequilibrium. We are looking for a guard dog that always barks and only barks, when there is in fact a burglar in the house. Inflation failed. NGDP would be better. Can we find something better still? I don’t know.

With regards to used goods (element 1): I am not sure how much of a problem this is with regards to the “ideal” input-output tables. Transferring assets is about transferring inputs (not perfectly, I will concede). However, gross output as a proxy for our ideal measure is not the best.

With regards to used goods (element 2): Although I think Skousen oversells his case sometimes, his proposal for gross domestic expenditures could be even better than GO. His GDE is basically GO+wholesalers sales+retail sales. There are indices of volumes of used goods sales (I am sure there is one for houses). These could be added to the Skousen proposal. The true test of efficiency would be, in spite of short-run volatility that would be greater than for NGDP, the long-run trends of both GDE and NGDP would be similar. Then we’d have to compare how much the short-run movements of NGDE explain short-run variations of RGDP.

“I do not know how the shift from “transactions” to “output” occurred, but I do know that as semantic as some may see it, it is crucial.”

Here is Milton Friedman:

“Despite the large amount of empirical work done on the transactions equations, notably by Irving Fisher and Carl Snyder ( Fisher 1911 pp 280-318, Fisher 1919, Snyder 1934), the ambiguity of the concept of “transactions” and the “general price level”, particularly those arising from the mixture of current and capital transactions—were never satisfactorily resolved. The more recent development of national income accounting has stressed income transactions rather than gross transactions and has explicitly and satisfactorily dealt with the conceptual and statistical problems of distinguishing between changes in prices and changes in quantities. As a result, the quantity theory has more recently tended to be expressed in terms of income rather than of transactions.”

JP: so once again, the categories of national income accounting determine how we think, rather than vice versa. The Order of Things in The Celestial Emporium of Benevolent Knowledge strikes again.

In reply to both JP and Nick: This is something I have often complained about. I keep pointing out that I am trained as an economic historian. Thus, my training as an economist is geared towards data quality, recreation of data and the mind-boggling details of national accounting and other statistical series.

Simultaneously, as an economic historian, you are forced to have a strong understanding of theory across a wide set of fields. The poor data yielded by old data sources could often lead to “statistically significant” relations that are not significant economically (or even wrong by sheer virtue that the data is of low quality).

Hence, the goal of an economic historian is to find a better data set. The quest is not to conform to match the theory to fit the data but to find the data that properly allows one to falsify (as a true Popperian) the theory! I always feel that a vast majority of the econ field does not care as much about the details of datasets and will often select to adapt the theory to the data rather than have data that is meant to properly test the theory.

Here, I think we have the same case. We adapted output instead of transactions because it was easier than simply figuring out a way to measure transactions. This may have been a good proxy in the 1950s when computing power was low. However, it became embedded in the literature and later, when computing power increased, we forgot why we did that and the “imperfect solution” has become the norm (and the source of some confusion). ****

****Note: That is why I suggest that economists read their classics every 5-10 years so they remember the core of the field. Like a “Jouvence” quest to allow the field not to age badly…

Thanks for linking to The Fluttering Veil, Vincent. It’s nice to see evidence of Yeager’s continuing influence!

I had a discussion a few months ago at the department where I am a course lecturer where we asked each other which were our favorite monetary theory books.

I answered: Yeager, Timberlake, Lucas, Kydland-Prescott and The Mon.Hist.of.USA

At that point, I really felt alone in the room…

[…] In his comeback, Vincent writes: […]

[…] proxy as it captures more goods and services traded at the intermediate level (see blog posts here, here and here). The core of my argument is that NGO will capture many “time to […]