For some time now, I have been skeptical of the narrative that has emerged regarding income inequality in the West in general and in the US in particular. That narrative, which I label UCN for U-Curve Narrative, simply asserts that inequality fell from a high level in the 1910s down to a trough in the 1970s and then back up to levels comparable to those in the 1910s.

To be sure, I do believe that inequality fell and rose over the 20th century. Very few people will disagree with this contention. Like many others I question how “big” is the increase since the 1970s (the low point of the U-Curve). However, unlike many others, I also question how big the fall actually was. Basically, I do think that there is a sound case for saying that inequality rose modestly since the 1970s for reasons that are a mixed bag of good and bad (see here and here), but I also think that the case that inequality did not fall as much as believed up to the 1970s is a strong one.

The reasons for this position of mine relates to my passion for cliometrics. The quantitative illustration of the past is a crucial task. However, data is only as good as the questions it seek to answer. If I wonder whether or not feudal institutions (like seigneurial tenure in Canada) hindered economic development and I only look at farm incomes, then I might be capturing a good part of the story but since farm income is not total income, I am missing a part of it. Had I asked whether or not feudal institutions hindered farm productivity, then the data would have been more relevant.

Same thing for income inequality I argue in this new working paper (with Phil Magness, John Moore and Phil Schlosser) which is a basically a list of criticisms of the the Piketty-Saez income inequality series.

For the United States, income inequality measures pre-1960s generally rely on tax-reporting data. From the get-go, one has to recognize that this sort of system (since it is taxes) does not promote “honest” reporting. What is less well known is that tax compliance enforcement was very lax pre-1943 and highly sensitive to the wide variations in tax rates and personal exemption during the period. Basically, the chances that you will report honestly your income at a top marginal rate of 79% is lower than had that rate been at 25%. Since the rates did vary from the high-70s at the end of the Great War to the mid-20s in the 1920s and back up during the Depression, that implies a lot of volatility in the quality of reporting. As such, the evolution measured by tax data will capture tax-rate-induced variations in reported income (especially in the pre-withholding era when there existed numerous large loopholes and tax-sheltered income vehicles). The shift from high to low taxes in the 1910s and 1920s would have implied a larger than actual change in inequality while the the shift from low to high taxes in the 1930s would have implied the reverse. Correcting for the artificial changes caused by tax rate changes would, by definition, flatten the evolution of inequality – which is what we find in our paper.

However, we go farther than that. Using the state of Wisconsin which had a tax system with more stringent compliance rules for the state income tax while also having lower and much more stable tax rates, we find different levels and trends of income inequality than with the IRS data (a point which me and Phil Magness expanded on here). This alone should fuel skepticism.

Nonetheless, this is not the sum of our criticisms. We also find that the denominator frequently used to arrive at the share of income going to top earners is too low and that the justification used for that denominator is the result of a mathematical error (see pages 10-12 in our paper).

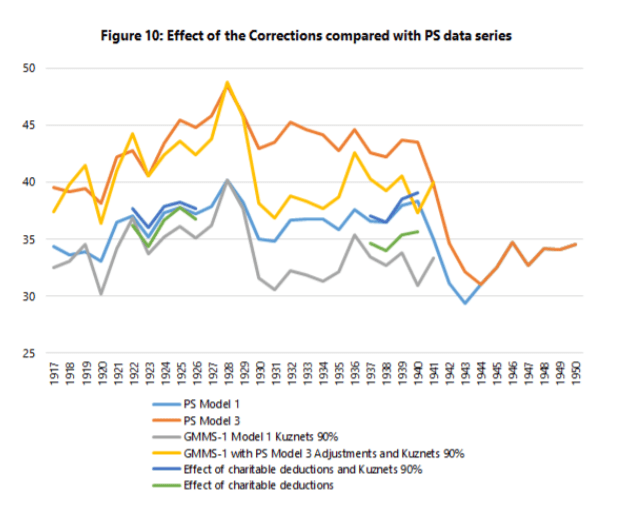

Finally, we point out that there is a large accounting problem. Before 1943, the IRS provided the Statistics of Income based on net income. After 1943, there shift between definitions of adjusted gross income. As such, the two series are not comparable and need to be adjusted to be linked. Piketty and Saez, when they calculated their own adjustment methods, made seemingly reasonable assumptions (mostly that the rich took the lion’s share of deductions). However, when we searched and found evidence of how deductions were distributed, they did not match the assumptions of Piketty and Saez. The actual evidence regarding deductions suggest that lower income brackets had large deductions and this diminishes the adjustment needed to harmonize the two series.

Taken together, our corrections yield systematically lower and flatter estimates of inequality which do not contradict the idea that inequality fell during the first half of the 20th century (see image below). However, our corrections suggest that the UCN is incorrect and that there might be more of small bowl (I call it the Paella-bowl curve of inequality, but my co-authors prefer the J-curve idea).