Before I start blogging at Notes on Liberty, I just want to say how happy I am to join this collaborative venture. I generally blog in French at the Journal de Montréal and my English writings are confined to my academic papers. Hence, I am very happy to communicate with English audiences.

Actually, this is an opportunity to write about NGDP targeting. In the anglosphere, this rule-based approach to monetary policy has been very popular. In the french world where I evolve, it is close to a fringe point of view (given a strong Old Keynesian/New Keynesian viewpoint). As a result, any effort to expand on the issue requires that the issue first be raised. Hence, I have avoided discussing monetary policy in my French writings. But there is a point that needs to be made about NGDP targeting as advanced by people like Scott Sumner, George Selgin, the late Bill Niskanen, Marcus Nunes, Benjamin Cole, David Beckworth, Lars Christensen and David Glasner : the idea of targeting nominal spending (me switching from the term NGDP to “nominal spending” is important) does not mean that we ought to target nominal gross domestic product.

The intuition behind NGDP target is that monetary policy should be aimed at reacting to changes in demand for money. Thinking of the equation of exchange (MV=PY), a change in V should be matched by an opposite change in M so that MV remains stable. Any increases in Y(output)should be met by reductions in P(rices) and no changes in MV. In practice, NGDP targeting is about avoiding deviations from long-term trends in NGDP. However, while the equation is often presented as MV=PY, the original papers by Irving Fisher and others present it as MV=PT where Y (output) is substituted by T (transactions).

But is PT the same as NGDP? At any point in time, total spending in the economy is much greater than the sum of final goods. There are intermediate goods which are being produced – intangible capital, capital inputs and producers goods. NGDP avoids calculating these because it would lead to double-counting. Work by Austrian-friendly scholars like Mark Skousen proposes that the double-counting is actually a strength in certain cases. This is because the double-counting gives greater weight to production. Skousen calls it “Gross Output”(GO) and he finds that GDP is generally a fraction of GO (at 53% in 1982).

Now, GDP is best for measuring welfare in the long-run. However, for short-run discussion, nominal GDP is not (at all) the sum of nominal spending. Imagine an easy monetary policy which incites firms to produce more, there might be a lag between the increased production and “arrival on shelves” for consumers to buy. This occurs as firms acquire new producer goods and/or gear themselves to producing goods for other producers. This means that in the short-run, the ratio of NGO to NGDP (nominal Gross Output) could vary. Easy monetary policy could make NGO grow faster than NGDP.

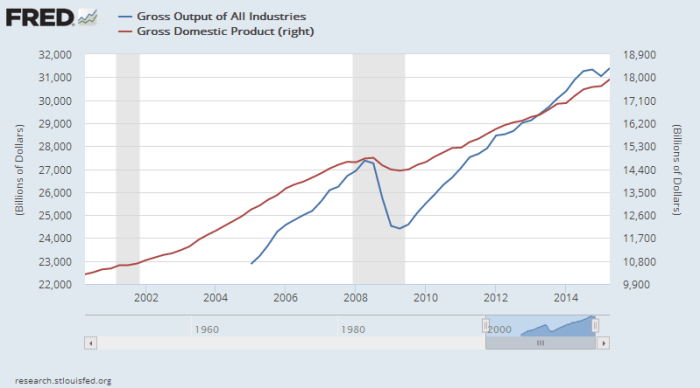

In a way, I am saying that NGDP is Y while the equation of exchange should be about all transactions (T in the original Irving Fisher papers) and transactions is best represented by NGO. As a result, NGO is a better proxy for trends of nominal spending. Let’s make a first test of this (and I hope this gets the ball rolling) by looking at the data.

The NGDP crowd claims that prior to 2008, monetary policy was easy, allowing NGDP to grow above trend. Tight monetary policy during 2008-2009 led to a significant drop below trend which was the cause of the recession. With NGO (gross domestic output for all industries as presented by St-Louis Fed), we see the same story but much more clearly!

From 2005 (when the data start for NGO) to 2008, NGO grows much more rapidly that NGDP (the ratio actually increases to 2008) and then it falls dramatically in 2008-2009 and barely recovers to remain stable thereafter. However, the drop from 2008-2009 is much more pronounced than that for NGDP. This suggests that “overall” nominal spending did fall more than NGDP suggests.

If monetary policy should shift to targeting nominal spending, NGDP is not the best indicator – NGO is.

It’s certainly true that people hold money in anticipation of all transactions, not just GDP transactions, so your argument has merit. However, if NGO is more volatile than NGDP as the chart suggests, then the monetary authoritiy’s lagging errors would be worsened by switching to NGO targeting.

I suggest that fiat money cannot be salvaged no matter how its rules are tweaked and that questions of targeting hardly matter. We need to return to competitive note issue (free banking). Fractional-reserve note-issuing banks could respond quickly to local demands for money in a way that no central bank, politically motivated as they always are, could ever do. See the writings of Selgin and White for details.

Warren: I would tend to disagree with the first half of your comment and partly agree with the second half. NGO as it currently stands may not be the best variable, but it remains closer to “total transactions” than NGDP is. Now, when central banks make decisions, NGO could be expanded as a statistic and refined so that it may eliminate some “noise” in its construction. However, NGO is simply an annualized version of an input-output table which is a good tool in identifying transmission mechanisms of monetary policy. If an IO table was made every year, that should be the “gauge” of monetary policy.

However, let’s assume that you are right on the first half and that the volatility of NGO prevents Central Banks from using it without making things worse. NGO maintains the benefit of hindsight when evaluating central banks and the stance of monetary policy in the long run..

Secondly, fiat money is not a problem per se. Government fiat money is. There we agree. Free banking offers numerous cases of individuals accepting lower reserve ratios of species to paper cash as banks produce reliable notes to “grease the wheel of trade”. My research with Mathieu Bédard on Canadian Free Banking from 1817 to 1851 (submitted to Enterprise and Society and presented at the Free Banking Conference in Lund, 2014) makes such a case.

Now, we live in an imperfect world where rent-seeking may have moved us away for a long-time from free banking, what do we do? Well, removing discretion on the part of central banks is a good first step. Rules on central banks may be somewhat inefficient relative to alternative arrangements like free banking. But as long as it is invariably inefficient, it will become a more “predictable” problem which actors can account for (see Lucas 1972; Kydland and Prescott 1977). In that regard, it’s better to accept a minor improvement that may have massive repercussions than a major improvement which will yield little marginal improvements (relative to the “political” cost).

It is an interesting question – if the policy makers are using a blend of a Taylor and Woodford rules to set the interest rates, one could integrate the NGO output gap in the model. I believe most of the authorities nowadays heavily rely on the nowcasting models which allow to forecast daily or weekly GDP (or NGO if needed) with the help of relevant high frequency variables.

NGO seems to be more volatile therefore the prediction error of such forecasts may be larger – so the bands of targeting will be wider. This is something the authorities try to avoid considering the Woodford rule – not all economic agents would enjoy volatility. It may be the case that bringing a more volatile indicator (even if its more precise) into the targeting rule will produce more volatile and broader distributed targets.

Vadim: I think that’s a good policy course. The federal reserve currently has numerous policy models through which it runs simulations. They never divulge the result to the public. However, they should and simultaneously include a NGO-rule.

With regards to the volatility of NGO, that’s where two policy proposals could be helpful. The first is the creation of a futures market for “nominal spending” which would allow markets to send signals for policy decisions (and basically trim down central banks to the bare minimum). The second, which is complementary to the first, is to expand the NGO statistics through a more frequent construction of input-output table. A rich and frequent IO table would have the side benefit of improving the quality of GDP constructs. More importantly, NGO and IO tables have a distinct advantage over all other constructs: it shows the complexity of the economy which means that we can see how “monetary transmission” occurs. You can see which sector is first affected by a “shock” and how it spreads.

Yes, indeed, I strongly agree that a frequent “Leontief” look at the economy is needed; however, it would be complicated to have frequencies higher, than the annual ones. It would be a great tool, if it is feasible – one could also see the structural change dynamics and have a better view on the transmission of monetary policy impulses. Are there any existing input-output tables for the US which are relevant nowadays? I know that in the 1950s and 1960s there was huge work done in this direction … OECD have IO tables for around 400 industries, but they are updated slowly.

The best solution is for the Fed to target commodity prices. Stabilizing the CRB Index (my preferred level is 300.00) would automatically stabilize everything else.

From June 2008 to March 2009, the real value of the dollar in terms of the CRB Index more than doubled. The result was a deflationary economic crash. The plunge in NGDP/NGO/Whatever was preceded by a huge rise in the value of the dollar. If the Fed had prevented this (and, to do so they would have had to never started paying interest on bank reserves) we would have had, at most, a garden variety recession.

Another huge advantage of targeting (and stabilizing) the CRB Index is that it is available in real time, and it is never revised. The Fed cannot actually target NGDP or NGO. It can only target (or pretend to target) its forecast of NGDP or NGO. There is far more accountability and less room for excuses if they target the CRB Index.

[…] the closing of 2015, Vincent Geloso proposed that the Fed target Nominal Gross Output (NGO), […]

[…] as it captures more goods and services traded at the intermediate level (see blog posts here, here and here). The core of my argument is that NGO will capture many “time to build” […]